By Nidhi Dua

Karnataka’s power sector has undergone a sea change. After experiencing a severe energy deficit of almost 14 per cent in 2011-12, the state has steadily improved its generation capacity over the past decade, and brought energy shortages to a negligible point. Remarkably, in the same period, the state also witnessed an impressive uptake of renewables, with installed capacity increasing from a mere 440.65 MW in 2011-12 to about 26,421.47 MW as of February 2026.

Karnataka’s power sector has undergone a sea change. After experiencing a severe energy deficit of almost 14 per cent in 2011-12, the state has steadily improved its generation capacity over the past decade, and brought energy shortages to a negligible point. Remarkably, in the same period, the state also witnessed an impressive uptake of renewables, with installed capacity increasing from a mere 440.65 MW in 2011-12 to about 26,421.47 MW as of February 2026.

The demand for electricity in the state has seen an upward trend in recent years, driven by expanding industrial activity, rapid urbanisation and growing energy consumption across sectors. To cater to this increasing demand, Karnataka has made substantial investments in its energy sector.

As per the Karnataka Economic Survey 2025-26, the state allocated a total of Rs 268.96 billion to the energy department, of which 99.84 per cent (Rs 268.53 billion) was directed towards developmental expenditure.

The state’s total installed power capacity has increased rapidly over the years, reaching 37,876.82 MW as of February 2026, according to the Central Electricity Authority (CEA). Thermal power contributed 10,814.95 MW, nuclear 698 MW and renewables 26,421.47 MW. Renewables make up around 70 per cent of the state’s total installed capacity, consisting of solar (11,029.95 MW), wind (8,500.54 MW), large hydro (3,689.20 MW), biopower (1,917.05 MW) and small hydro (1,284.73 MW) capacity, as per the Ministry of New and Renewable Energy (MNRE).

Karnataka’s solar portfolio includes 9,786.09 MW of ground-mounted solar, 840.9 MW of rooftop solar installations (including those under the PM Surya Ghar: Muft Bijli Yojana), 358.85 MW of hybrid solar and 44.11 MW of off-grid/Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyaan (PM-KUSUM) Component B. The state’s biopower capacity comprises 1,868.91 MW of biomass power/bagasse cogeneration, 20.2 MW of non-bagasse biomass cogeneration, 1 MW of waste-to-energy (WtE) and 26.94 MW of off-grid WtE capacity.

A look at the key trends and recent developments across renewable energy segments in Karnataka, and the future outlook…

Solar segment

The state has seen relatively slow uptake under the PM Surya Ghar scheme, with 159,947 applications received as of March 2026. Of these, 17,481 installations have been completed, covering 27,159 households. This reflects a conversion rate of 10.93 per cent, with a cumulative installed capacity of 69.81 MW.

Furthermore, under the PM-KUSUM scheme, performance has been mixed. For Component B, 41,365 standalone solar pumps were sanctioned, of which 5,533 have been installed. Under Component C, focused on feeder-level solarisation (FLS), 763,588 pumps were sanctioned, with 86,827 solarised so far. To accelerate FLS, the 2026-27 state budget introduced the Mukhyamantri Saura Krishi Yojana under Component C. The programme targets the development of 3 GW of solar capacity at substations of the Karnataka Power Transmission Corporation under the renewable energy service company model, with an outlay of Rs 105 billion.

Further, the state budget announced plans to develop 2,777 MW of solar projects under the PM-KUSUM Component C this year and 4 GW of solar capacity through microgrids under the Anantha programme, to be deployed across all gram panchayats under a public-private partnership model.

Meanwhile, the state’s progress in the development of large-scale solar parks has been slow, with only one solar park (2,000 MW Pavagada solar park) commissioned.

Storage segment

Storage segment

Karnataka has been actively investing in both battery energy storage systems (BESSs) and pumped storage projects (PSPs). According to the CEA, the installed energy storage capacity in the state is estimated to reach 15,752 MW by 2034-35. It has an estimated pumped storage potential of 7,600 MW. Of this, 3,600 MW is under construction and 300 MW is under survey and investigation. In a related development, a tender was issued by REC Power Development and Consultancy in March 2026 to develop an intra-state transmission system for evacuating power from the proposed 2,000 MW PSP at the Sharavathi complex.

The state has also been expanding its footprint in the BESS segment across project deployment, manufacturing and grid-level implementation.

In July 2025, Pace Digitek commissioned a BESS manufacturing facility through its subsidiary, Lineage Power Private Limited, in the Bidadi industrial area in Bengaluru, which has an annual production capacity of 2.5 GWh, extendable to 5 GWh. Solar-plus-BESS projects are being set up in the state.

In January 2026, Hartek Power was awarded the engineering, procurement and construction contract for a 280 MW solar PV project, along with an 80 MW/320 MWh BESS at Challakere.

Furthermore, Karnataka implemented 1,000 MWh BESS capacity across seven substations during 2025-26, as per the state budget 2026-27. Building on this, the state proposed an additional 2,000 MWh of BESS capacity at the Huliyur, Pavagada and Kushtagi substations, at an estimated investment of Rs 34 billion.

Green hydrogen segment

Karnataka has been making noteworthy progress in the green hydrogen segment through a series of industry developments in the sector…

In September 2025, SCC Infrastructure Private Limited and InSolare Energy Limited emerged as winning bidders under Solar Energy Corporation of India Limited’s (SECI) twelfth auction for green ammonia under the Strategic Interventions for Green Hydrogen Transition Programme (Mode 2A, Tranche I). The companies secured a contract to supply 15,000 tonnes per annum (tpa) of green ammonia to Mangalore Chemicals and Fertilisers in Karnataka at a tariff of Rs 57.65 per kg.

In November 2025, JSW Energy Limited commissioned a green hydrogen manufacturing plant adjacent to the JSW Steel facility in Karnataka. The plant will supply green hydrogen to the direct reduced iron unit of the steel plant for low-carbon steel production.

Bioenergy segment

The compressed biogas (CBG) sector in Karnataka is witnessing gradual progress, supported by policy push. As per the GOBARdhan portal, 124 CBG/bio-CNG plants have been registered in the state so far. Of these, 26 are currently under construction and only 20 plants have been commissioned to date.

Recent developments highlight growing momentum in the sector. In October 2025, GAIL (India) Limited signed a tripartite concession agreement with the Greater Bengaluru Authority (GBA) and Bengaluru Solid Waste Management Limited (BSWML) to set up a CBG plant in the KCDC area of Haralakunte village, Bengaluru South taluk. The project is expected to produce around 12.6 tonnes of CBG daily.

Furthermore, biofuel utilisation has seen modest progress. As per the Economic Survey of Karnataka 2025-26, around 14,694 litres of biodiesel was produced and utilised, promoting renewable energy adoption.

State of the sector and the way forward

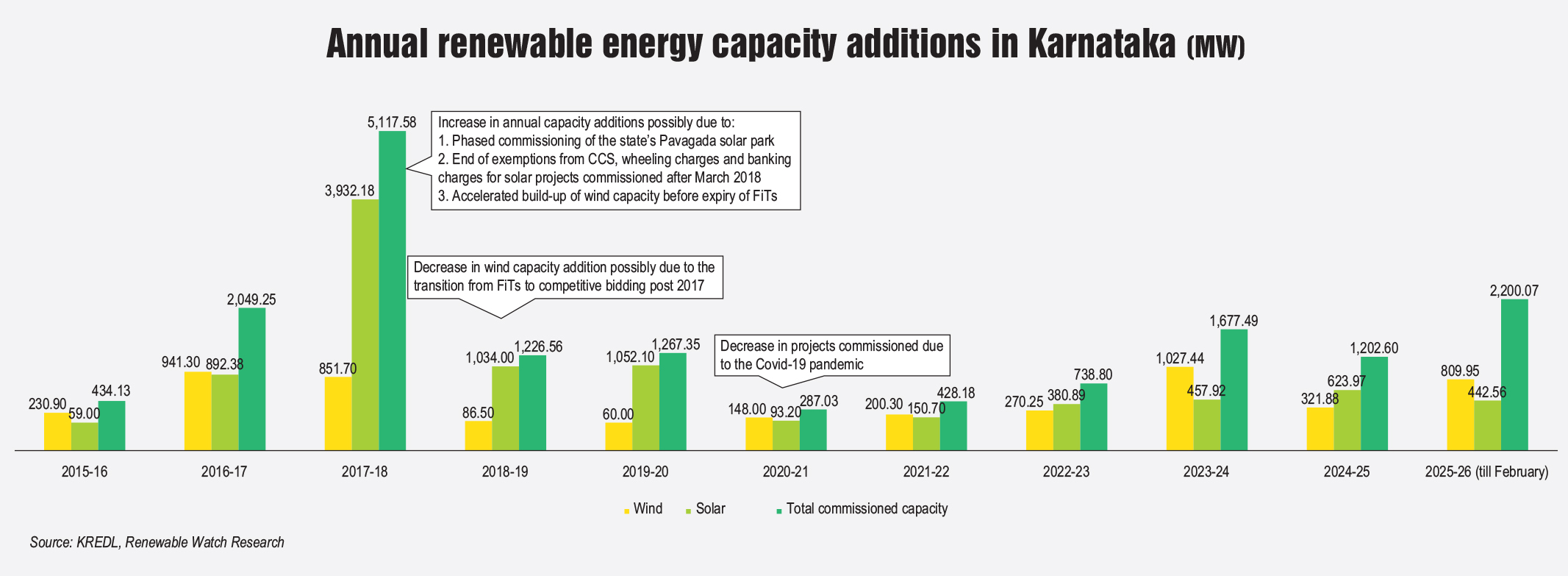

Several interesting trends have emerged in Karnataka over the years across the power sector value chain. Renewable energy commissioning has followed a highly uneven pattern (refer to the graph). Until 2015-16, annual capacity additions remained below 500 MW. Post that, commissioned capacity increased, with an exceptional peak in 2017-18, when more than 5,100 MW was added in a single year. This peak can be attributed to solar capacity additions of 3,932.18 MW. One reason for this was the phased commissioning of the state’s Pavagada solar park, which began around this period.

Following a regulatory update in 2014, the state introduced incentives for open access solar power, including exemptions from wheeling charges, banking charges, and cross-subsidy surcharges (CCS) for 10 years for projects achieving commercial operation before March 31, 2018. These incentives prompted developers to expedite project commissioning before the policy deadline.

Around the same time, the wind power sector witnessed a boom-and-bust cycle. While annual wind capacity additions remained less than 320 MW till 2015-16, they surged to 941.3 MW in 2016-17 and 851.7 MW in 2017-18. However, capacity addition declined sharply to 86.5 MW in 2018-19 and 60 MW in 2019-20, which is less than 10 per cent of the earlier levels. A major cause for this decline was the transition from feed-in tariffs (FiTs) to competitive bidding (reverse auctions) in 2017. Developers fast-tracked project execution to commission capacity under the earlier tariff regime before the shift. Post-transition, lower tariffs and initial auction-related challenges led to a slowdown in project execution. Notably, it was only in 2023-24 that wind capacity additions surpassed the previous high recorded in 2016-17.

Overall, following the 2017-18 peak, the momentum for renewable capacity addition did not return. Capacity additions declined to 1,200-1,300 MW in 2018-19 and 2019-20. A further sharp drop was observed in 2020-21, when commissioning fell to about 287 MW. This decline can be attributed, in part, to disruptions caused by the Covid-19 pandemic, which affected renewable energy project development globally.

Although there has been a gradual recovery since then, the trend overall remains inconsistent. In 2025-26 (up to February 2026), commissioning has shown renewed momentum, with over 2,200 MW of capacity added.

In terms of new capacity additions, the CEA’s quarterly report on under-construction renewable energy projects released in September 2025 indicates that Karnataka has over 18 GW of renewable energy projects under construction. This includes 3,223 MW of solar capacity, 9,706 MW of wind capacity and 5,344 MW of hybrid capacity. Karnataka’s project pipeline reflects its focus on developing a diversified renewable energy mix.

The state has also increased its procurement from power exchanges over the years. Power procurement from other states through energy exchanges rose sharply in the state from 589 MUs (2022-23) to over 3,800 MUs (2025-26). The average power purchase cost from the exchange market has declined steadily from Rs 8.09 per kWh to Rs 5.26 per kWh. The average sale price of surplus power through energy exchanges has fluctuated, with the highest price being Rs 6.38 per kWh in 2025-26 (up to December 25) and lowest being Rs 4.07 per kWh in 2023-24.

The state has also laid equal emphasis on the expansion of its transmission infrastructure. According to a Rajya Sabha response dated February 11, 2026, over the past five years under the Intra-State Transmission System GEC Phase I, Karnataka’s transmission line length increased from 531 ckt km in 2020-21 to 596 ckt km in 2021-22 and 618 ckm in 2022-23, after which it remained constant at 618 ckt km in 2023-24 and 2024-25. Substation capacity stood at 2,490 MVA in 2020-21 and 2021-22, and then increased to 2,702 MVA in 2022-23, remaining unchanged at 2,702 MVA through 2023-24 and 2024-25. Overall, Karnataka has achieved its target of 2,702 MVA substation capacity under GEC Phase I. The target for GEC Phase II is 1,225 MVA.

As per the CEA’s transmission plan for integration of over 900 GW non-fossil fuel capacity by 2035-36, Karnataka is placed as an important renewable energy hub. For utilising 31.24 GW solar and wind potential in the state, the ISTS network for 30.74 GW is already under implementation, with commissioning scheduled between 2026-27 and 2029-30, and the remaining 0.5 GW ISTS network is planned for 2028-29. Furthermore, the state has envisaged a renewable energy capacity addition of 2,639 MW under GEC-II, with 938 ckt km of transmission lines and a transformation capacity of 1,225 MVA. Additionally, under GEC-III, the state plans to add 19,010 MW of renewable energy capacity with 8,306 ckt km of transmission lines and 35,305 MVA of transformation capacity.

In the distribution space, both aggregate technical and commercial (AT&C) losses and transmission and distribution (T&D) losses have declined in Karnataka over the years, according to the state economic survey for the year 2025-26. T&D losses decreased from 15.73 per cent in 2019-20 to 12.57 per cent in 2024-25, while AT&C losses fell from 15.32 per cent to 10.89 per cent during the same period.

Karnataka’s power sector continues to face financial stress, with all ESCOMs selling power below cost during 2024-25. The average tariff of Rs 8.90 per unit was lower than the average cost of power of Rs 10.03 per unit, creating a gap of Rs 1.13 per unit for ESCOMs. Overall, in 2024-25, all ESCOMs were in loss, with total losses being Rs 88.69 billion. This financial weakness affected the utilities’ capacity to invest in grid infrastructure and renewable energy integration.

On the contrary, the state has surpassed its renewable energy targets ahead of schedule. While the Karnataka Renewable Energy Policy 2022-27 aimed to add 10 GW during the policy period, installed capacity rose from 15,904.59 MW in 2022 to 26,421.47 MW by February 2026. Despite achieving its renewable capacity targets ahead of schedule, utilisation of resource potential remains low. According to a research report titled “Indian States’ Electricity Transition (SET) 2026” by the Institute for Energy Economics and Financial Analysis and EMBER, as of March 2025, only 4 per cent of wind and 39 per cent of solar potential had been utilised by Karnataka, leaving a significant share untapped.

Moving forward, bridging the tariff-cost gap through tariff rationalisation and efficiency improvements is necessary to improve the financial health of ESCOMs. Strengthening transmission infrastructure and improving grid management will be critical to support higher renewable energy penetration and address variability-related challenges.

Meanwhile, efforts are under way to expand renewable energy use in emerging sectors such as data centres, supported by policies such as the Data Centre Policy 2022-27. Additionally, maintaining a consistent project pipeline, ensuring faster approvals, and improving land acquisition and evacuation planning will be essential for Karnataka to fully realise its renewable energy potential.