By Mohammed Ali Siddiqui

Two thousand years ago, Aristotle coined the term “energeia” to describe the moment when potential transforms into actual action. One could argue that the modern energy system is now experiencing its moment of energeia. Every year, global energy demand increases due to the rising energy needs of developing economies and the emergence of new demand centres, such as data centres. However, this growing trend is accompanied by challenges, such as a slowdown in renewable energy adoption, geopolitical tensions that affect supply chains, and sluggish progress on climate finance commitments made at international climate conferences.

As per McKinsey’s Global Energy Perspective 2025, clean energy deployment is likely to stall in the US as tensions emerge in energy trade with the imposition of tariffs across renewable energy components. However, 2025 may also be remembered as a pivotal year for the global energy transition due to the emergence of battery energy storage systems (BESS). The segment recorded the fastest year-on-year growth vis-a-vis other segments, driven by a significant decline of more than 50 per cent in battery costs in the past two years. Currently, China leads not just in terms of installed capacity every year but also dominates technology segments in the renewable energy supply chain. Renewable Watch presents a comprehensive overview of the emerging global trends that have been shaping renewable energy in 2025.

Regional developments

Americas

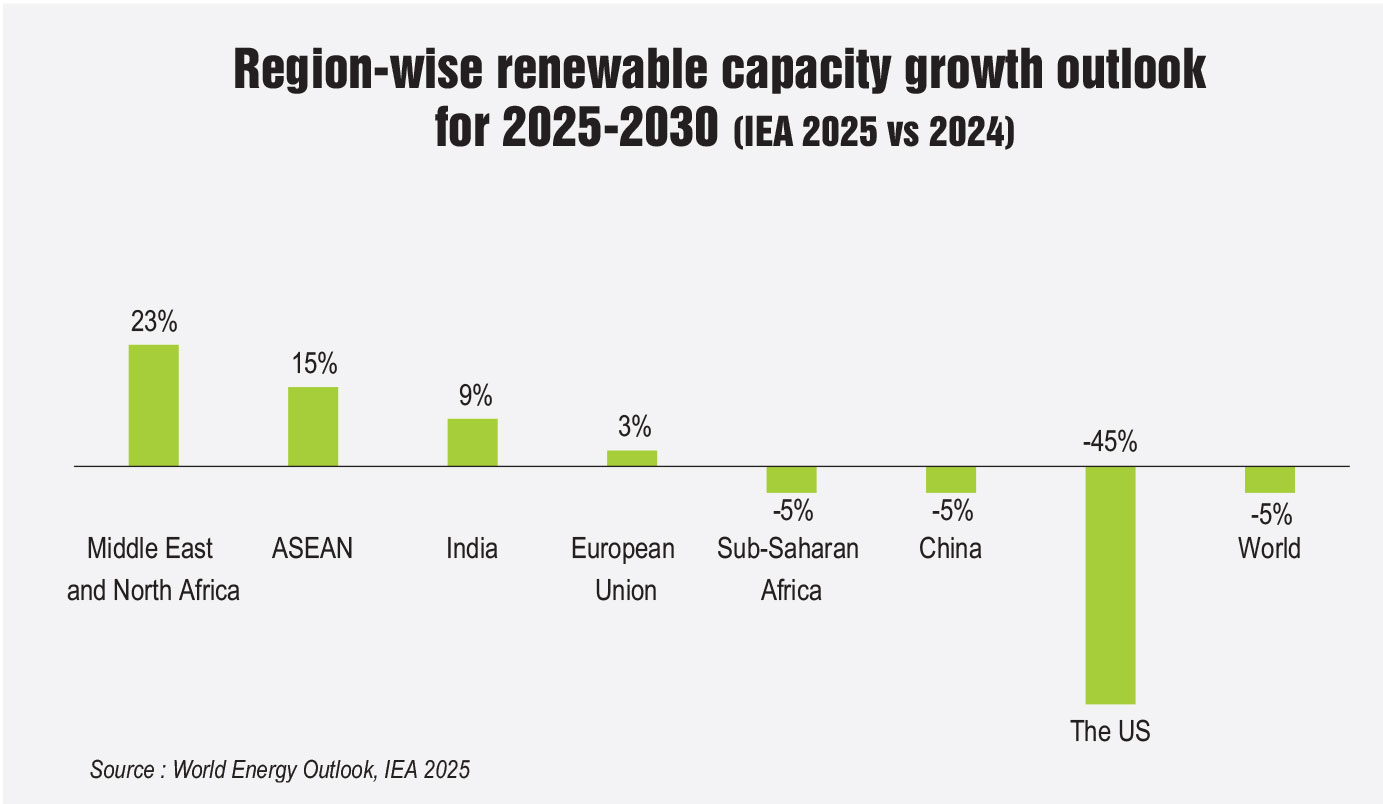

In 2025, only three years after initiating the Inflation Reduction Act (IRA), the US significantly altered the course of its energy transition. The One Big Beautiful Bill Act, passed in July 2025, was a reversal of the progress on energy transition made during the IRA era. For starters, the bill prohibits projects sourcing components from “prohibited foreign entities” (mostly Chinese companies) with the risk of disqualification. It also imposes new barriers for developers by accelerating the phase-out timelines. As a result, the IEA’s Renewables 2025 forecast has marked a 50 per cent “downward” revision in US renewable energy capacity additions across nearly all technologies, with solar expected to decline by about 40 per cent and wind by 60 per cent. According to official press releases from the White House, the new administration has signalled its formal exit from the Paris Agreement. Despite this setback, there is a positive trend in demand for round-the-clock renewables from technology companies. According to McKinsey’s Global Energy Perspective 2025, with power demand likely to triple in the next three years, tech majors such as Google, Amazon, Microsoft, and Meta have firmed up plans to invest in solar plus storage solutions to scale up facilities. Overall, the US renewable energy landscape in 2025 presents a paradox: it is experiencing one of the largest surges in demand for AI-powered renewable energy while simultaneously witnessing cuts in federal commitments to the clean energy transition.

Meanwhile, South America is moving towards a clean energy future. Over the next decade, electricity demand is likely to quadruple, which will necessitate a significant expansion in installed renewable energy capacity and increased regional cooperation. According to IRENA’s Regional Energy Outlook on South America, the region could face average efficiency losses amounting to USD 1 billion per year. In response to this challenge, regional initiatives such as the Energy Integration System of the Southern Cone Countries (Sistema de Integración Energética de los Países del Cono Sur – SIESUR) and the Andean Electrical Integration System (Sistema de Interconexión Eléctrica Andina – SINEA) have emerged to promote market integration. Brazil and Chile are two of the key clean energy proponents in the region. Brazil has been ramping up its renewable energy capacity by focusing on hydropower and biofuels, as it consumes nearly 50 per cent of its energy demand from clean energy. The Republic of Chile generates 35 per cent of its energy from clean energy sources. Endowed with abundant renewable energy sources, the country has been at the forefront of achieving its net-zero goals by 2050, with a focus on green hydrogen. Chile released its National Hydrogen Strategy in 2020 and introduced its Electromobility Strategy in 2022, which outlines goals for 5 GW of electrolysis capacity by 2025 and 100 per cent electric vehicle sales by 2035..

Europe

In Europe, wind power will remain the dominant energy source, driving the continent’s energy transition. According to WindEurope, it added 6.8 GW of new wind capacity in the first half of 2025, with Germany in the lead. As of mid-2025, Europe’s total wind power installed capacity stood at 291 GW. Almost 89 per cent of the new additions are dominated by onshore wind projects. However, a significant challenge for Europe is its limited domestic manufacturing base. While wind and solar capacities have increased, the industry still relies on imports of renewable energy technologies from China, Southeast Asia, and India. Due to these interdependencies, the continent is exposed to significant risks, especially amidst emerging geopolitical uncertainties. In response, the European Union (EU) has constituted the REPowerEU strategy, which aims to install over 420 GW of wind energy capacity by 2030, implying at least 30 GW of new generation capacity addition each year. This strategy has positive implications for European wind turbine manufacturers, as the increased demand for wind turbines will encourage them to invest in domestic manufacturing. Another important policy notification announced in early 2025 is the Clean Industrial Deal, which aims to support energy-intensive sectors while also building a domestic clean tech value chain. The deal plans to raise over 100 billion euros through various policy mechanisms, such as the Innovation Fund and an industrial decarbonisation bank. To support the existing 14.7 GW of offshore wind installed capacity in the UK, the Offshore Wind Growth Partnership launched a £2 million funding pool in August 2025. In addition to its already strong position in the offshore wind energy supply chain, the UK is expected to witness significant growth in this segment.

Asia

Asia

For most of the post-war industrialisation period, the idea of pursuing economic development alongside decarbonisation was viewed as an impossible task. From 1978 to the early 2010s, China’s gross domestic product grew by more than 10 per cent every year, establishing the country as the manufacturing capital of the world. This was largely due to the increasing consumption of coal and oil. The country’s developmental strategy has transitioned from the conception of coal as a pre-requisite for energy security to the vision of an “ecological civilisation”. This concept, first proposed by then President Hu Jintao at the 17th Party Congress in 2007, aims to balance domestic energy security with the development of clean energy. For instance, the Atlas Institute reported that as of 2023, China’s clean energy sector contributed around 40 per cent to its GDP in 2023. According to Ember, by 2024, China was producing every four out of five solar modules and battery cells globally, more than two-thirds of electric vehicles, and over half of all heat pumps.

Besides manufacturing, China is also emerging as the world’s clean energy laboratory. As per IRENA’s patent database, between 2000 and 2022, the share of patent applications in clean energy technologies by China rose from just 5 per cent to around 75 per cent. Not surprisingly, in the first half of 2025, it installed more solar capacity than the rest of the world combined. According to the China Hydrogen Development Report, the country is now home to half of the world’s green hydrogen deployment. As China establishes a widespread presence in nearly every component of the clean energy supply chain, other countries are also increasing their manufacturing capabilities. Vietnam and Thailand have started offering incentives to attract battery and module assembly, whereas Singapore is trying to position itself as a regional research and development hub.

Meanwhile, India, despite its production-linked incentive (PLI) schemes and Make in India initiatives, continues to rely heavily on Chinese imports, even as its manufacturing capacities rise. As per the Ministry of New and Renewable Energy and media reports, imports of photovoltaic (PV) cells have only dipped by 2 per cent, regardless of the presence of the Approved List of Models and Manufacturers. Between FY 2024 and FY 2025, India’s solar cell imports surged by 88 per cent, with China’s share rising from 70 per cent to 90 per cent. Meanwhile, its module imports declined from 48.48 million panels to 40.99 million panels. Notably, India is on track to meet its target of 500 GW of installed non-fossil fuel capacity by 2030, having crossed 120 GW of installed solar capacity and 250 GW of cumulative renewable energy capacity. As India demonstrated at the recently concluded COP30 in Belém, it can fulfil half of its electricity demand through renewable energy sources, and is set to achieve its 2030 target five years ahead of schedule.

Africa

The energy resource-rich African continent continues to struggle to attract investment, both public and private. Currently, nearly 600 million people still lack access to electricity. According to the IEA’s World Energy Investment 2025, global renewable energy investments are expected to surpass the $3 trillion mark, of which Africa will receive only 2 per cent. This is ironic given that more than 85 per cent of the continent receives over 2,000 kWh per m^2 of solar irradiation every year, nearly double that of Europe. A commonly cited reason is the shortage of bankable projects. This is compounded by high capital costs, volatile currencies and underdeveloped regulatory frameworks.

In many African countries, borrowing costs are almost three times higher than in developed economies, making renewable energy projects expensive. Furthermore, transmission infrastructure delays pose significant hurdles. Recognising this issue, the World Bank, African Development Bank, and Sustainable Energy for All have launched “Mission 300”, with the objective to ensure energy access to over 300 million people by the end of this decade. Any serious discussion on the state of renewable energy in Africa warrants a close examination of China’s involvement in the region. China has pledged over CNY100 million in public funds to power 50,000 off-grid households using solar systems through the Africa Solar Belt Initiative. Before 2024, China had primarily played the role of a lender, having invested over $65 billion, which accounted for one-third of its total renewable energy lending. However, between 2020 and 2024, Chinese wind and solar technology exports to Africa increased by over 150 per cent. Chinese firms are focusing on executing their clean energy industry engagements through engineering, procurement and construction projects. In contrast, the US has decided to reduce its allocations to international clean energy initiatives, including the Power Africa initiative.

Middle East

Middle East

Earlier this year, the Masdar Group announced a $6 billion project to develop a 5 GW solar plant with over 19 GWh of battery storage. In terms of size, this is reported to be the largest project ever attempted in the region. Surprisingly, a decade ago, renewable energy was virtually absent from the Middle East’s energy landscape. For instance, in 2010, the region’s installed capacity was just 1 GW. However, over the next decade, the region’s installed renewable energy capacity has increased to over 30 GW. In addition to these capacity additions, the region has entrenched itself more deeply in global supply chain. With over 99 per cent of the UAE’s solar modules and almost 80 per cent of Oman’s PV panels imported from China, the region is now turning its attention towards local manufacturing. For instance, in October 2024, Saudi Arabia’s energy ministry iterated its commitment to localising 75 per cent of its energy sector. Meanwhile, the UAE is pursuing a market-led strategy that emphasises flexible regulations and open market incentives to promote module assembly, in a bid to attract Chinese firms. Following a similar route, Oman is targeting renewable energy manufacturers by promoting free zones and offering fiscal incentives. Meanwhile, Qatar, like Saudi Arabia, is interested in localising upstream technologies, with investments in polysilicon production through Qatar Solar Technologies.

To improve regional connectivity, the Gulf Cooperation Council Interconnection Authority is set to invest over $3.5 billion in the following decade to tap into export channels beyond the region, strengthen the transmission backbone, and eventually turn the Gulf into a regional electricity export hub.

Conclusion

According to Daniel Yergin, an eminent energy historian, energy transition is a multidimensional process that unfolds at varying speeds across regions depending on technology adoption. So far, developing countries have led the efforts to scale up renewables and expand energy access. Central to this push, China’s rapid production of virtually every renewable technology has helped reduce prices and enable technology adoption across the world. Looking ahead, it is clear that only coordinated action through regional cooperation and technological diffusion is essential for building a secure global energy system. As China has demonstrated, national development priorities need not be at odds with international engagement. The question now is: how can countries chart their own paths towards decarbonisation while advancing domestic priorities. The way we address this challenge will shape the future of the energy transition itself.