The renewable energy sector has witnessed a number of innovative policy initiatives to promote uptake. A key initiative to resolve the issue of intermittency in renewable energy and promote grid stability has been to shift from vanilla solar or wind projects to hybrid, assured peak power and eventually round-the-clock (RTC) tenders. An overview of different RTC tenders (1 to 3), key policy initiatives, and the future outlook…

Policy background

In a bid to promote the grid-connected solar power segment, a provision for bundling was introduced in the first phase of the National Solar Mission. Under this scheme, expensive solar power was bundled with cheaper power from non-renewable energy sources, including thermal power generated at NTPC’s coal-based stations. There were other policy interventions that assisted in the reduction of risks associated with solar and wind power projects. These included advanced arrangement of land, and evacuation through solar parks, green energy corridors, and 25-year power purchase agreements with an elaborate mechanism for risk apportionment and compensation, payment security. The tariffs for solar and wind power projects subsequently fell; in fact, they went even lower than the tariffs for non-renewable energy/thermal power projects owing to such de-risking policy initiatives. Economies of scale, technology advances and the availability of abundant and cheap finance also helped bring down renewable energy tariffs. These factors resulted in the rapid expansion of renewable energy capacity, especially solar and wind, in both the public and private sectors.

While the increasing uptake of renewables was indeed a positive development, certain fundamental issues needed to be tackled, especially with regard to the intermittent and unpredictable nature of renewable energy and low capacity utilisation of the transmission system. These issues became more pronounced when the grid had to absorb large-scale renewable projects. To resolve these issues, distribution companies had to arrange for balancing power to ensure grid stability during the non-availability of renewable energy. Given that the utilities’ were already facing acute financial stress, having to ensure grid stability as well made the case for reverse bundling even stronger. In this scenario, it was envisaged that cheaper renewable energy would be bundled with relatively expensive non-renewable energy, including coal-based thermal power, and sold to discoms round the clock, thus alleviating their woes to some extent.

Accordingly, the Ministry of Power issued the “Guidelines for tariff-based competitive bidding process for procurement of round-the-clock power from grid-connected renewable energy power projects, complemented with power from any other source or storage” on July 22, 2020. According to the ministry, the guidelines were issued with the objective of providing RTC power to discoms to facilitate the scale-up of renewables, economies of scale and renewable purchase obligations compliance.

RTC 1, 2 and 3 tenders

Before the RTC tenders were floated, the government, through the Solar Energy Corporation of India (SECI), had started a transition to renewable-plus-storage tenders in 2016. Later, in August 2019, SECI issued a 1.2 GW tender for renewable-plus-storage projects with an assured peak power supply. In January 2020, the auction took place and Greenko and ReNew Power won 900 MW and 300 MW at a peak tariff of Rs 6.12 per kWh and Rs 6.85 kWh respectively and off-peak tariff of Rs 2.88 per kWh. Then, in October 2019, SECI issued the RTC tender for the first time, called RTC-1, with a capacity of 400 MW. ReNew Power won the entire capacity of this auction at a tariff of Rs 2.90 per kWh for the first year.

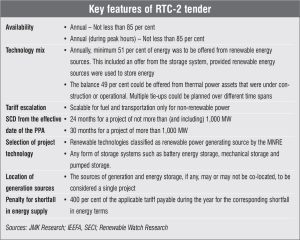

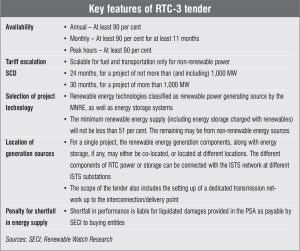

Keeping the momentum going, SECI issued the ambitious RTC-2 tender for 5,000 MW of capacity in March 2020, with bundled renewable and thermal energy. However, in December 2020, the tender’s capacity was halved. The lowest tariff of the RTC-2 auction was Rs 3.01 per kWh, quoted by Hindustan Thermal Projects for 250 MW capacity. The auction was concluded but SECI had asked other developers to match the L1 tariff, and just 250 MW was awarded finally. After a gap of around two and a half years, SECI released its RTC-3 tender in September 2022 with an aggregate capacity of 2,250 MW. The power procured by SECI from the projects will be sold to MPSEZ Utilities Limited. The tender provides for incentives such as accelerated depreciation, concessional customs and excise duties, and tax holidays.

Future outlook

While the policy push to promote RTC power is impressive, some issues and concerns have been highlighted by several sector stakeholders. One, the high cost of energy storage implies that its use will be minimal and focus will primarily be on renewables and thermal power. Two, supply chain disruptions, duties and taxes applicable on solar components, and increase in input costs may hike the cost of solar and renewable energy projects. This puts a question mark on whether the discoms will be willing to buy it. Three, there are concerns regarding the complicated nature of rules and provisions for RTC tenders, making the task of the developer tedious and prone to stringent penalties.

Issues notwithstanding, RTC tenders are the future of India’s clean energy landscape and more such tenders are awaited by the industry. In fact, corporates are also demanding RTC power from developers, making the segment all the more interesting.

By Sarthak Takyar