The year 2016 was marked by significant progress in the transition from conventional means to alternative sources of energy with record new additions, declining costs and tariffs, as well as long strides in technological advancement. Energy efficiency, climate change and renewable energy deployment continued to be the centrepiece of attention globally. The Paris Agreement was adopted during the 22nd United Nations Framework Convention on Climate Change Conference [UNFCCC] of Parties in November 2016. Even though the expansion of renewable energy is yet to reach the level required to restrict the global rise in temperature to below 2 °C above pre-industrial levels as established in the Paris Agreement, the foundation to achieve this goal has been greatly strengthened in the past year.

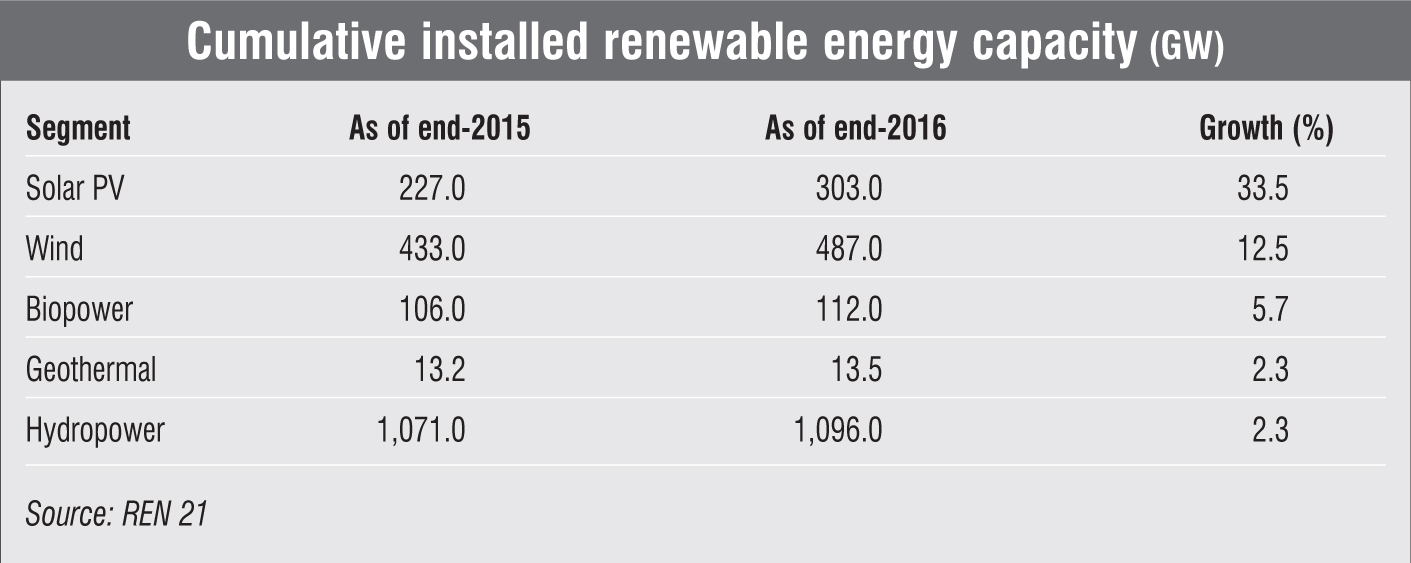

About 161 GW of renewable energy capacity was added in 2016, growing by nearly 9 per cent over 2015 and setting a new global record. Of this, 47 per cent of capacity was added in the solar photovoltaic (PV) segment alone, followed by 34 per cent of wind and 15.5 per cent of hydropower. This capacity addition entailed an investment of about $249.8 billion, roughly double the investments in the fossil fuel sector. The addition was greater than the combined capacity added for all fossil fuels in 2016. However, investments fell by about 23 per cent as compared to those in 2015, largely due to the slowdown in the Chinese and Japanese markets.

Given the increased deployment of renewable energy and the decreased coal consumption, carbon emissions from fossil fuels and industries remained stable for the third consecutive year even as the global economy grew at about 3 per cent, indicating the decoupling of economic growth and carbon emissions. In the developing world especially, higher renewable energy targets at the state, city and local levels have brought about a paradigm shift in deployment towards off-grid areas through minigrids.

Renewable Watch takes a look at the global trends in the renewable energy sector during the past year…

Solar

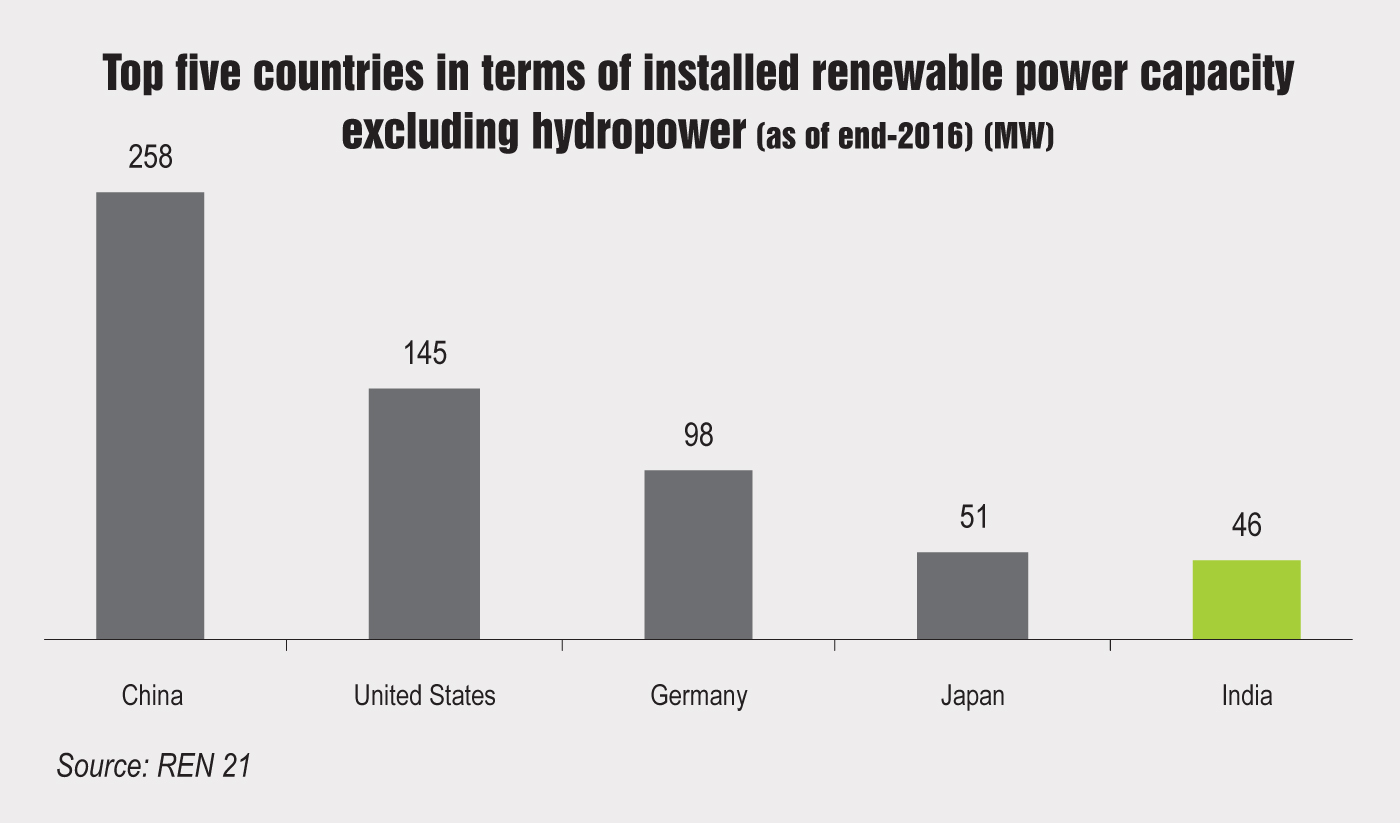

In 2016, over 75 GW of solar power capacity was added globally, taking the cumulative installed solar capacity to 303 GW. Capacity addition in this segment grew by about 48 per cent over 2015 and was more than the combined capacity addition in the previous five years. China, the US and Japan continued to be the top three countries, together accounting for about 77.5 per cent of the installations (China 46 per cent, the US 20 per cent and Japan 11.5 per cent). India ranked fourth, accounting for 5.5 per cent of the total solar PV capacity addition, followed by the UK and Germany with 2.7 per cent and 2 per cent respectively.

For the fourth year, Asia remained the largest solar market, adding about two-thirds of the total global solar capacity in 2016, with China, Japan and India leading the capacity additions. China continued to dominate in solar PV installations and manufacturing, gaining significant ground in the emerging markets of the Middle East and Africa. It added 34.5 GW of solar capacity, growing by about 126 per cent over 2015 and taking the country’s total capacity to 77.4 GW. Despite the downward adjustment in China’s 2020 targets due to slow growth in electricity demand, the installed capacity increased on the back of a rush to commission approved projects to avail of the 2015 feed-in tariff (FiT) rate. The second largest in Asia and the third largest overall, Japan added 8.6 GW in 2016, taking the country’s cumulative solar capacity to 42.8 GW. This growth was driven mainly by large-scale projects and to some extent by a surge in residential solar systems. About 50,000 residential systems in Japan included storage as of end-2016. India was the third largest market in Asia and the fourth globally, while being the seventh largest in terms of total cumulative capacity. The country added about 4.1 GW taking the total to 9.1 GW as of end-2016. The rooftop market accounted for about 10 per cent of India’s total solar capacity.

The US became the second largest global market. Its solar capacity addition in 2016 stood at 14.8 GW, nearly double that in 2015, taking the country’s cumulative solar capacity to 40.9 GW as of end-2016. In Europe, the UK remained the top market in 2016, adding about 2 GW and increasing the country’s total to 11.5 GW. Germany fell short of its annual target of 2.5 GW and added only 1.5 GW. The country’s total stood at 41.3 GW as of end-2016. Despite the slowdown, Germany’s solar-plus-storage market has grown significantly, by more than 50 per cent over 2015. Also, in 2016, Germany and Denmark held the world’s first cross-border auctions for solar PV, for which all successful bids were for projects sited in Denmark.

Meanwhile, 2016 saw a steep fall in the prices of modules, inverters and structural balance of systems due to high demand and high supply, especially from China. This has led to reduced margins for manufacturers as the costs have not fallen as swiftly. On the other hand, 2016 was a good year for developers as the decreased costs resulted in improved margins. However, the trend may not continue in 2017 owing to a sharp fall in tariffs across the world, especially in China, India, Chile, Jordan, South Africa and the UAE. In the US, power purchase agreement (PPA) prices have dropped sharply, making solar more profitable than new natural gas capacity.

China dominated global shipments for the eighth consecutive year. In 2016, Asia accounted for 90 per cent of the global module production (of which China’s share stood at 65 per cent), while Europe accounted for 5 per cent and the US for 2 per cent. The top 10 module manufacturers were responsible for about 50 per cent of the global shipments, indicating a strong market consolidation trend. The top company among these was China-based Jinko Solar, followed by Trina Solar and JA Solar (both China), Canadian Solar (Canada), Hanhwa Q Cells (Republic of Korea), GCL (China) and First Solar (USA).

Consolidation was a dominant trend in the solar market in 2016 as new partnerships were formed to capture value in project development and enter new markets. Spanish solar inverter major Ingeteam purchased Italy-based Bonfiglioli’s solar PV business, while Foxconn purchased financially stressed Japanese solar module maker Sharp. GE, Gamesa, Goldwind and Mingyang, four of the world’s top wind power companies, too entered the solar segment by end-2016. In addition, Tesla partnered with Panasonic to acquire SolarCity, with plans to create a solar PV storage electric vehicle product.

Owing to several challenges, the concentrating solar power (CSP) segment added a meagre 110 MW as of end-2016, taking the global capacity to 4.8 GW. Recording just 2 per cent growth over 2015, this has been the lowest increase in the total global capacity in 10 years. However, about 900 MW of CSP capacity is expected to come online by end-2017. The market was led by South Africa followed by China. The segment grew outside of the traditional markets of Spain and the US. In Asia, besides China, India was the only country with CSP facilities. A 25 MW CSP plant is currently under construction in Gujarat. Although Morocco, the world leader in CSP technology in 2015, did not add any new projects in 2016, its 200 MW Noor II parabolic trough and 150 MW Noor III tower are expected to be commissioned in 2017.

Wind

The wind power segment saw a 14 per cent decline in capacity additions over the record year of 2015, with 433 GW. A total of 55 GW was added across the world, the second highest wind capacity addition till date, to take the global installed capacity to 487 GW. By end-2016, 29 countries had installed wind power capacity of more than 1 GW, while over 90 countries had begun commercial wind power activity. The market decline can be attributed to the sharp contraction in the Chinese wind power segment, despite which it maintained its global lead. China was followed by the US, Germany and India, which surpassed Brazil. Bolivia and Georgia installed their first large-scale wind farms in the past year.

Asia remained the dominant region in wind power capacity additions in 2016 for the eighth consecutive year, contributing about half of the global capacity addition. China added 23.4 GW in 2016, down by 24 per cent over 2015, to take the country’s overall wind power capacity to 169 GW. The reduction in capacity addition was due to weak power demand and grid integration issues. India installed 3.6 GW to end the year with 28.7 GW, largely due to the rush to avail of the accelerated depreciation benefits that were phased out from April 2017. Turkey added 1.4 GW in 2016 to increase the country’s total to 6.1 GW. Other notable Asian countries that added substantial wind power capacity in 2016 were Pakistan (0.3 GW), the Republic of Korea (0.2 GW) and Japan (0.2 GW), taking the region’s total to 203 GW.

The US became the second largest country for wind capacity additions in 2016, adding 8.2 GW of capacity and taking its total to 82.1 GW. The trend of investments by utilities in the segment continued. The share of non-utilities decreased to 39 per cent from 52 per cent in 2015, but grew over 2014 (23 per cent) and 2013 (5 per cent). As of end-2016, 10.4 GW of wind power was under construction in the US.

Canada added 0.7 GW, half of the capacity added in 2015, taking its total wind capacity to 11.9 GW. The European Union (EU) installed about 12.5 GW of wind power capacity, down by 3 per cent over 2015. The onshore wind capacity addition increased by about 3 per cent, while that of offshore decreased by about 50 per cent. The total EU capacity by end-2016 stood at 153.7 GW. Germany emerged as the largest European market, adding about 5 GW, pegging the total wind capacity at 49.5 GW. This growth was largely driven by the transition from FiT to the competitive bidding mechanism for project allocation. The other major European countries in this segment were France (1.6 GW), the Netherlands (0.9 GW), Finland (0.6 GW), Ireland (0.4 GW) and Lithuania (0.2 GW). In the offshore wind power segment, 2.2 GW was connected to the grid and 9 MW decommissioned in 2016 to increase the global offshore wind power capacity to 14.4 GW.

The levellised cost of energy for wind power continued to decline in 2016 as technological advancements resulted in decreased capital costs across the globe. Record low bids were witnessed in Chile, India, Mexico and Morocco; prices also fell sharply for offshore tenders in Europe. Most of the wind turbine manufacturing remained restricted to China, India, the EU and the US. The market witnessed further consolidation and the largest market shares remained in the hands of the top companies. The top 10 players, which accounted for about 75 per cent of the market, were Denmark-based Vestas, which surpassed Goldwind (China) to regain its lead position owing to a strong year in the US, followed by GE (USA), Goldwind, Gamesa (Spain), Enercon (Germany), Siemens (Germany), Nordex Acciona (Germany), and United Power, Envision and Mingyang (China).

Capacity ratings also increased in 2016 with the average size of turbines rising by 6.4 per cent over 2015 to 2.16 MW. Average turbine sizes were the highest in the Middle East and the Commonwealth of Independent States (2.8 MW) due to the installation of several 3.3 MW machines, followed by Europe (2.7 MW), Latin America (2.3 MW), North America (2.2 MW), and Africa and Oceania (both below 2 MW).

Other markets

Biopower

The global biopower capacity increased by about 6 per cent in 2016 to reach 112 GW by end-2016. The world leaders in biomass-based electricity generation in 2016 were the US (68 TWh), China (54 TWh), Germany (52 TWh), Brazil (51 TWh), Japan (38 TWh), and India and the UK (both 30 TWh). Although the US remained the largest producer of electricity from biomass sources, generation fell by around 2 per cent in 2016 to 68 TWh, down from the 2015 level of 69 TWh, as the segment faced increasing price competition from alternative renewable generation sources in a number of states under the Renewable Portfolio Standards. In Europe, the growth in electricity generation from both solid biomass and biogas continued in 2016, driven by the Renewable Energy Directive. In Germany, Europe’s largest producer of electricity from biomass, the total biopower capacity increased by 2 per cent, to reach 7.6 GW. The UK’s biopower capacity increased by 6 per cent to reach 5.6 GW, mainly due to the large-scale generation.

Hydropower

The global hydropower capacity addition in 2016 stood at around 25 GW, with the total capacity reaching approximately 1,096 GW. The top countries for hydropower capacity are China, Brazil, the US, Canada, the Russian Federation, India and Norway, which together accounted for about 62 per cent of the installed capacity by end-2016. More than one-third of the new hydropower capacity was commissioned in China, which added 8.9 GW of capacity in 2016, increasing its total to 305 GW. The countries adding the most capacity in 2016 were Brazil, Ecuador, Ethiopia, Vietnam, Peru, Turkey, Lao PDR, Malaysia and India. Brazil’s hydropower output increased by around 7.4 per cent over 2015 to 410 TWh owing to improved hydrological conditions in 2016.

The global pumped storage capacity was estimated at 150 GW at the year’s end, with about 6.4 GW added in 2016. China was the leading installer of pumped storage capacity during the year, adding 3.7 GW of capacity and increasing its total to 27 GW. South Africa, Switzerland, Portugal and the Russian Federation followed.

Investments

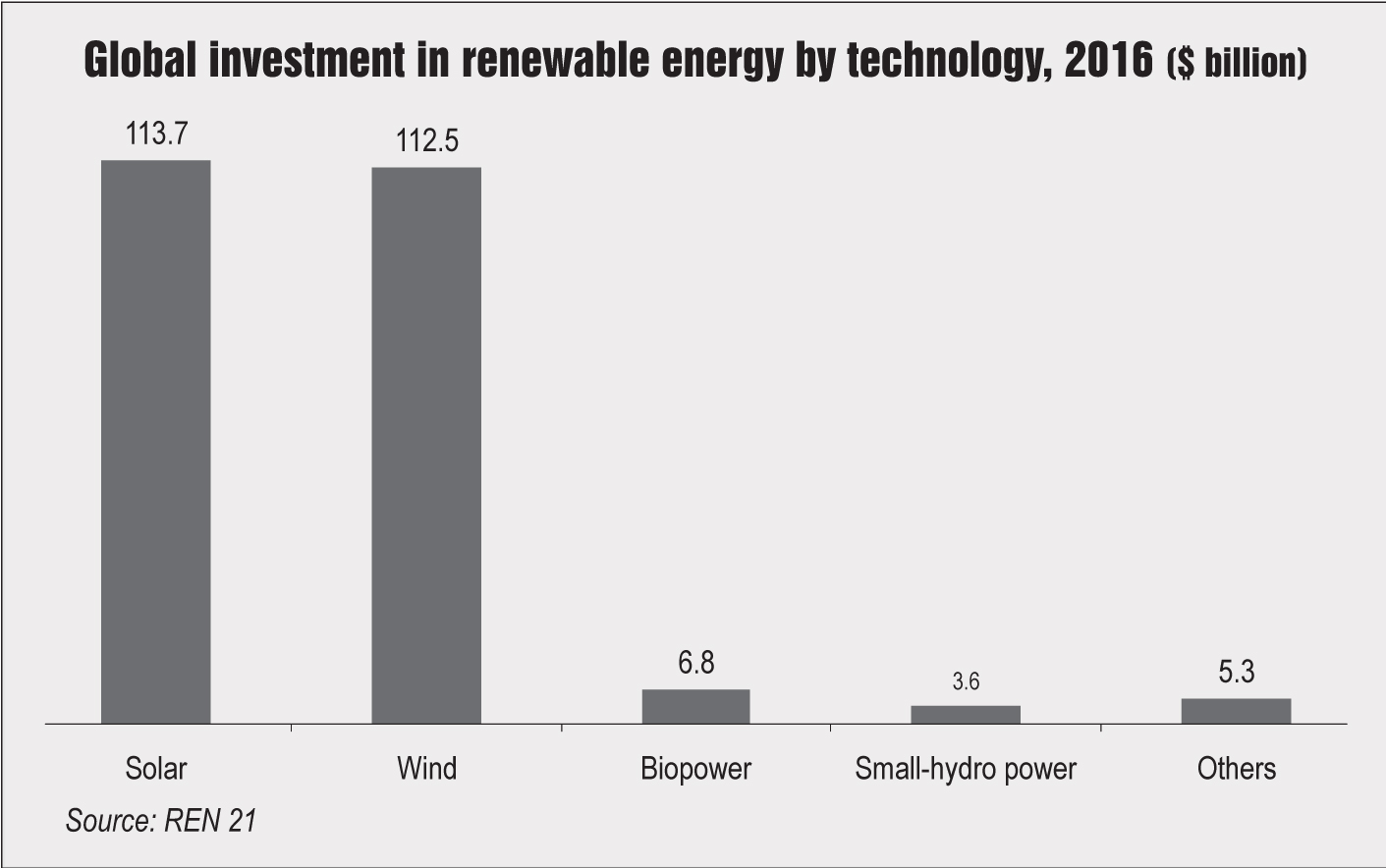

According to Bloomberg New Energy Finance, the global investment in renewable energy in 2016 is estimated at $241.6 billion, representing a 23 per cent decrease over 2015, due largely to the decrease in capital costs over the past year, leading to more renewable energy capacity per dollar. Asset finance of utility-scale projects such as wind farms and solar parks received the largest investments during the year at $187.1 billion, whereas small-scale solar PV installations (less than 1 MW) accounted for $39.8 billion worldwide, representing a decline of 28 per cent over 2015.

Renewable energy investment in developed countries fell by 14 per cent in 2016 to $125 billion. While investments in Japan and the US declined, Europe witnessed a slight increase. In developing countries, renewable energy investments fell by 30 per cent to $116.6 billion. China was instrumental in this turnaround, breaking an 11-year rising trend. Chile, Mexico, Morocco, Pakistan, the Philippines, South Africa, Turkey and Uruguay had all reached the billion-dollar market level in 2015, but there was a decline in 2016 due in part to delayed auctions or delays in securing equity for projects that won capacity in tenders. Argentina, Bolivia, Egypt, Indonesia, Jordan, Kenya, Mongolia, Peru, Thailand and Vietnam saw an increase in investments in 2016. Renewable energy investments across the globe declined primarily due to the slowdown in Japan, China and other emerging countries.

Outlook

The strong growth and investments in the renewable energy sector can be attributed to a solid policy and regulatory base, driven by targets at the global, regional and local levels that have compelled countries to promote renewable energy and create a favourable business ecosystem. The year 2016 not only saw large capacity additions in China, India and the US, but also witnessed the laying of a bold foundation in many African, Middle Eastern, South Asian and Latin American countries.

With reducing capital costs and decreasing tariffs, the global renewable energy market is expected to continue its upward journey. The trend of high investments in the sector is expected to continue on the back of the Paris Agreement targets and Intended Nationally Determined Contributions under the UNFCCC. High cost competitiveness and awareness have led to the technology becoming increasingly affordable. Coupled with innovative financing options such as PPAs, community-led programmes and off-site options, reduced costs will ensure renewable energy growth in even remote parts of the world. With dedicated targets for climate change and energy under the Sustainable Development Goal 7 of the United Nations in place, the future of renewable energy seems promising.

However, the sector is also riddled with challenges like land acquisition in developing countries and the lack of proper grid integration in countries like China and India. This has led to significant congestion in the grid networks of these countries, resulting in project delays and cost overruns. Planning, innovation, use of storage technology and technological advancements can help improve grid conditions and make way for larger renewable energy installations in the developing economies.

Based on the Global Status Report 2017