By Nidhi Dua

By Nidhi Dua

Green hydrogen is emerging as a key pillar of India’s transition towards a low-carbon economy, with the country increasingly focusing on building a domestic production and manufacturing ecosystem. Backed by India’s rapidly expanding renewable energy capacity, the sector is witnessing growing momentum with developments across the entire value chain. Falling renewable energy costs, technological advancements in electrolysers and rising global demand for low-carbon fuels and derivatives are further strengthening the business case for green hydrogen in India.

The sector is moving beyond policy announcements and early-stage ambitions to tangible on-ground progress. Against this backdrop, this article examines the status of India’s green hydrogen projects, upcoming project pipelines, electrolyser manufacturing and emerging demand segments for the next phase of growth, based on insights shared at Renewable Watch’s 11th edition of the “Green Hydrogen in India” conference…

Recent policy and project developments

The Government of India recently undertook several important policy initiatives in the green hydrogen and derivatives segment. In February 2026, the Ministry of New and Renewable Energy (MNRE) notified separate standards for green ammonia and green methanol, building on the green hydrogen standards notified earlier. These standards are expected to bring greater clarity and uniformity to the emerging market. Another major milestone has been the launch of the Green Hydrogen Certification Scheme of India. This scheme establishes a national framework for measuring and verifying the greenhouse gas intensity of domestically produced hydrogen. It is expected to strengthen traceability for exports, while also linking green hydrogen production with India’s carbon credit market.

Commissioned projects

India has commissioned six green hydrogen projects across the steel, refinery and industrial manufacturing sectors (Table 1). Key commissioned projects include the GAIL Vijaipur green hydrogen project, Bharat Petroleum Corporation Limited’s (BPCL) Bina refinery green hydrogen project, JSPL-Jindal Renewables’ Angul green hydrogen and green steel project, JSW Vijayanagar green hydrogen and green steel project, Hero Future Energies’ Tirupati green hydrogen project for Rockman Industries, and INOXAP’s Chittorgarh green hydrogen project for Asahi Glass. These projects together account for around 70 MW of installed electrolyser capacity and are expected to produce around 10,000 tonnes per annum (tpa) of green hydrogen.

Project pipeline

Project pipeline

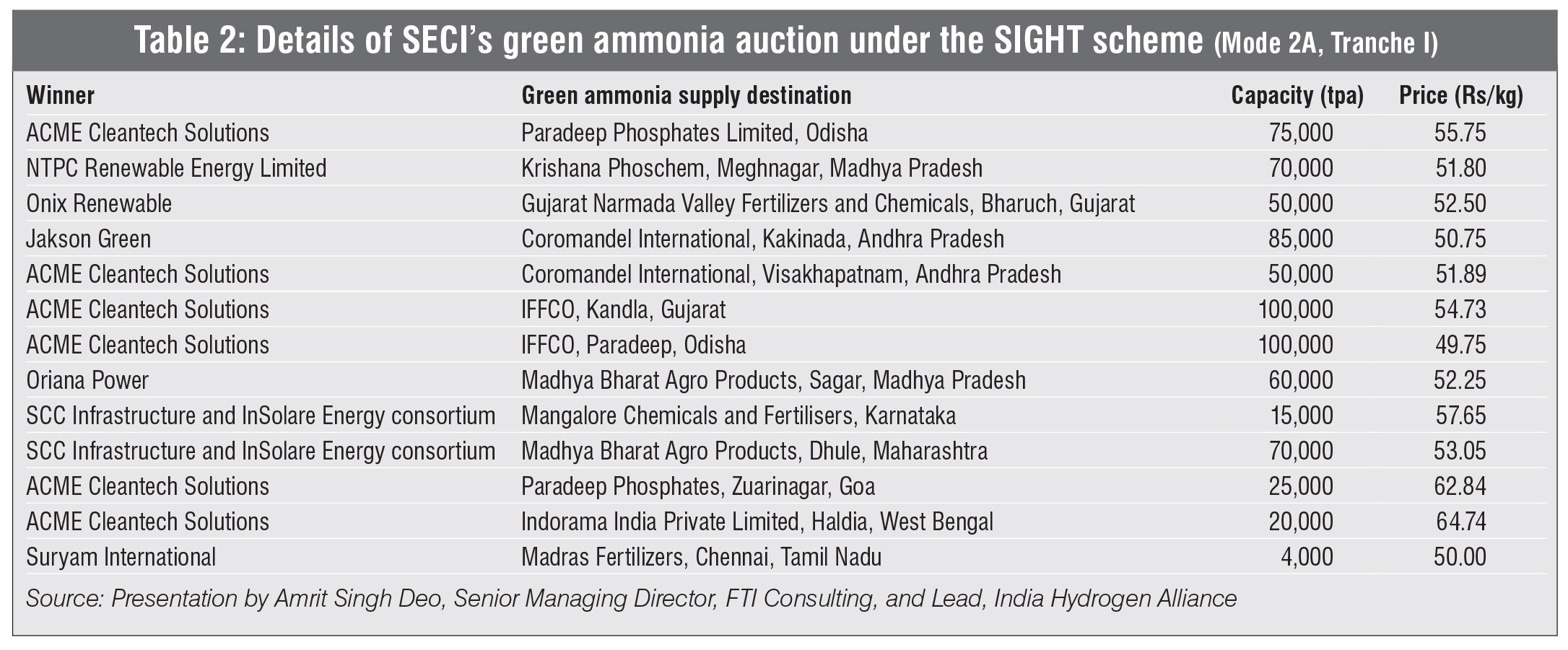

One of the sector’s most significant developments has been the conclusion of the green ammonia tender in 2025 (Table 2). Due to this, India’s green ammonia sector is expected to see significant capacity additions over the next 36 months under the Strategic Interventions for Green Hydrogen Transition (SIGHT) scheme (Mode 1, Tranche 2A). Following the completion of the bidding process, the sector has now begun transitioning from capacity allocation to long-term offtake execution. In March 2026, SECI signed six agreements with manufacturers to supply green ammonia to fertiliser companies. Of the total allocated green ammonia supply capacity of 724,000 tpa under SECI’s SIGHT scheme (Mode 2A), agreements covering 670,000 tpa have been signed so far. Agreements have been signed by ACME Cleantech, Jakson Green, NTPC Green Energy Limited, Oriana Power and a consortium of SCC Infrastructure and InSolare Energy. Furthermore, through these projects, 1,485 MW of electrolyser capacity is to be installed within the next 36 months and 637,400 tonnes of green hydrogen is expected to be delivered. This covers only 2.5 per cent of the National Green Hydrogen Mission’s (NGHM) 5 million metric tonne (mmt) target.

Applications

Apart from green ammonia, the adoption of green hydrogen is expected to expand across several hard-to-abate sectors, particularly refining, steel and other energy-intensive industries. Green hydrogen is emerging as a key pathway for industrial decarbonisation, particularly through the replacement of grey hydrogen in existing industrial processes. The companies are currently adopting a phased approach towards green hydrogen deployment, with the focus initially on pilot-scale projects to gain operational experience in production, storage, transportation and safety management. Despite current commercial challenges, investments in the sector continue to gain traction, largely driven by long-term decarbonisation commitments and the expectation that green hydrogen will become cost-competitive over time.

Refinery segment as a key demand centre

The refinery sector is expected to become one of the most significant application areas for green hydrogen in India over the next decade. Although progress in refinery-based green hydrogen adoption has remained slow so far, the segment holds substantial long-term demand potential due to its large existing grey hydrogen consumption base.

To accelerate its adoption, a SECI-led aggregated green hydrogen supply tender targeting 350,000 mtpa of green hydrogen offtake for refineries is required, as per the India Hydrogen Alliance. The proposal is based on replacing 10 per cent of the grey hydrogen consumption with green hydrogen, across existing and upcoming refinery projects by 2030. The assessment covers 17 existing refineries as well as planned expansion projects by companies including Reliance Industries Limited, Indian Oil Corporation Limited, BPCL and Hindustan Petroleum Corporation Limited. Existing refineries alone currently consume nearly 3 million tonnes of grey hydrogen annually, creating a potential demand of about 300,000 tonnes of green hydrogen under a 10 per cent replacement scenario. Planned refinery expansions could contribute an additional demand of nearly 51,766 tonnes, taking the total estimated demand potential to around 351,766 tpa.

The proposed SECI-led tender could contribute nearly 7 per cent of the NGHM target. Beyond supporting emission reduction efforts in the refining sector, the initiative is also expected to create early-stage demand visibility, improve project bankability and catalyse large-scale investments in domestic green hydrogen production infrastructure.

Electrolyser technologies and the manufacturing ecosystem

Electrolyser technologies and the manufacturing ecosystem

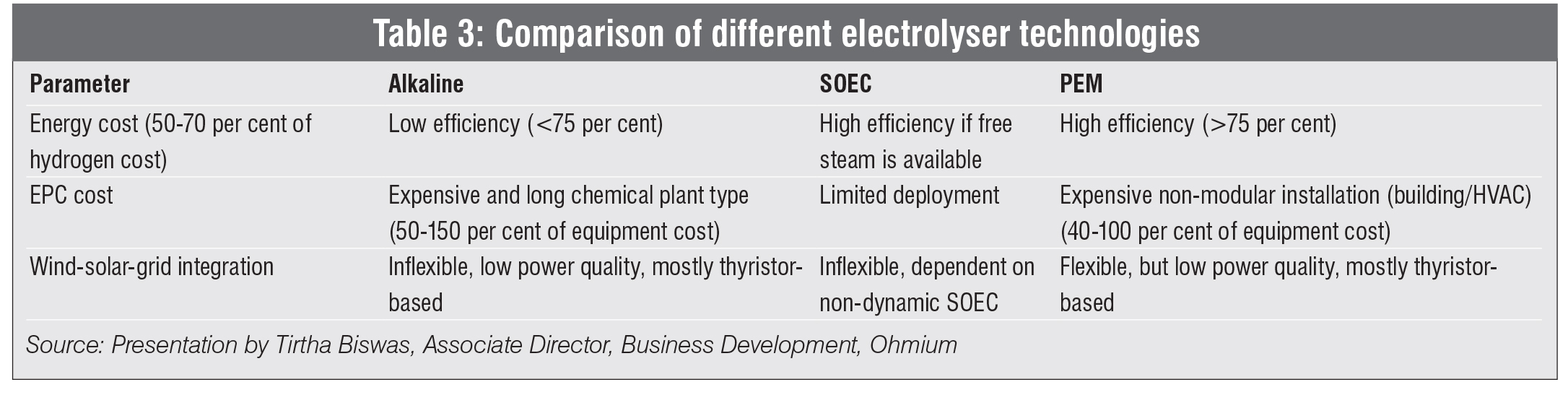

Some of the electrolyser technologies currently available in India’s green hydrogen market are alkaline water electrolysis (AWE), proton exchange membrane (PEM) and solid oxide electrolysis cell (SOEC). Among these, AWE remains the most widely deployed technology globally, accounting for nearly 61 per cent of the market share. The technology is highly mature and commercially established, with relatively lower upfront capital costs compared to other electrolyser technologies. However, alkaline systems have comparatively lower dynamic response capabilities, making them less suitable for handling highly variable renewable energy sources such as solar and wind power.

Meanwhile, PEM electrolysers currently account for around 31 per cent of the global electrolyser market and are witnessing rapid technological advancements and declining costs. PEM electrolysers are more compact and can efficiently operate under fluctuating renewable power conditions, making them increasingly attractive for green hydrogen projects linked to intermittent renewable energy sources. SOEC technology, although still emerging, is also attracting interest because of its high efficiency potential. However, the technology requires very high operating temperatures. A detailed comparison of these technologies is provided in Table 3.

As India’s green hydrogen project pipeline expands, the development of domestic electrolyser manufacturing capacity is becoming increasingly important for reducing import dependence and supporting long-term cost competitiveness. In this context, under the NGHM, the government has awarded a cumulative electrolyser manufacturing capacity of 3,000 MW per annum to 15 companies. The largest allocations of 300 MW per annum each were awarded to Reliance Electrolyser Manufacturing Limited, John Cockerill, L&T Electrolysers Limited, Advait, Matrix Gas and Renewable, NewAge Green Electro Private Limited, Waaree Energies and Adani Enterprises. Most of these manufacturing facilities are planned in Gujarat, while Andhra Pradesh and Karnataka have also emerged as key locations for electrolyser manufacturing investments.

Meanwhile, Ohmium Operations secured 274 MW per annum of manufacturing capacity in Karnataka. Other beneficiaries include GH2 Solar with 105 MW, Homihydrogen with 102 MW in Maharashtra, Avaada with 50 MW, Eastern Electrolyser and Newtrace with 30 MW each, and Suryaashish KAI Solar Park with 10 MW per annum capacity. This initiative is aimed at building a domestic electrolyser manufacturing ecosystem capable of supporting India’s rapidly expanding green hydrogen project pipeline and long-term decarbonisation goals.

Outlook

Going forward, the development of a robust demand ecosystem and long-term policy visibility will be critical for scaling India’s green hydrogen sector and achieving the targets under the NGHM. Currently, despite growing policy momentum, large-scale adoption remains constrained by high production costs, limited demand visibility and infrastructure gaps across the value chain. One of the biggest challenges continues to be the availability of affordable, round-the-clock, renewable power. While solar-based electrolysis is increasingly cost-competitive during daytime hours, the lack of low-cost firm renewable energy keeps green hydrogen production costs elevated, affecting the commercial viability. In addition, significant gaps remain in storage facilities, transportation infrastructure, pipelines and port connectivity, underlining the need for coordinated ecosystem-wide planning and investment.

To address these challenges and stimulate market creation, stronger demand-side interventions and long-term procurement mechanisms are required. Introduction of a SECI-style tender for refinery units is expected to provide long-term demand certainty, improve project bankability and accelerate investments in the domestic production infrastructure. Policy measures such as hydrogen purchase obligations and demand-side mandates are also identified as important tools to accelerate green hydrogen adoption across industrial sectors.

Expanding the budget allocation under the NGHM can also support demand creation in hard-to-abate sectors. Support measures could include public procurement programmes, concessional public finance, fiscal incentives and contract-for-difference style schemes aimed at improving the commercial viability of industrial decarbonisation projects.

Another major recommendation is the inclusion of green hydrogen and green ammonia projects under priority sector lending, which could improve access to lower-cost financing and support long-term industrial investments. In parallel, greater coordination between the central and state governments is needed for the development of hydrogen infrastructure, industrial hubs and green hydrogen clusters, in partnership with anchor industrial offtakers. Coordinated infrastructure planning and policy support are expected to play a critical role in enabling large-scale investments across production, storage, transportation and export infrastructure over the coming decade.

This article is based on remarks by

Dr Prasad Arvind Chaphekar, Director, Hydrogen, MNRE; Abhishek Kumar Ambasta, DGM (Green Hydrogen), SECI; Harsh Nupur Joshi, Chief Operating Officer, ONGC Green; Ashish Goyal, Associate Vice President, Procurement and Renewable Energy Projects, Jindal Stainless; Amrit Singh Deo, Senior Managing Director, FTI Consulting, and Lead, India Hydrogen Alliance Secretariat; and Tirtha Biswas, Associate Director, Business Development, Ohmium; at Renewable Watch’s 11th edition of the “Green Hydrogen in India” conference, 2026