By Karan Sharma

As India looks to scale solar beyond the limits of land availability and siting constraints, its reservoirs, canals and industrial water bodies are emerging as a valuable, though largely untapped, resource. Floating solar projects address some of the legacy challenges faced by ground-mounted solar in India, particularly delays in land acquisition and competing land uses. They are, therefore, being increasingly deployed on balancing reservoirs, backwaters and man-made ponds.

As India looks to scale solar beyond the limits of land availability and siting constraints, its reservoirs, canals and industrial water bodies are emerging as a valuable, though largely untapped, resource. Floating solar projects address some of the legacy challenges faced by ground-mounted solar in India, particularly delays in land acquisition and competing land uses. They are, therefore, being increasingly deployed on balancing reservoirs, backwaters and man-made ponds.

While floating PVs (FPVs) come with a cost premium in tariffs and installation costs compared to ground-mounted solar, these projects enable enhanced generation. In Indian operating conditions, generation from FPVs is typically around 5 per cent higher than that from ground-mounted systems, as per a presentation by R.R. Maurya, general manager, engineering and quality, NTPC Green Energy Limited, at Renewable Watch’s conference on “Hydro Power in India”. Overall, observed gains range from 2.5 per cent to 8.8 per cent in favourable conditions, as per the International Energy Agency.

A key benefit of FPVs is the availability of existing substations and transmission infrastructure at hydropower and thermal reservoirs, thus reducing project investments. Another key advantage is lower evaporation losses, allowing a larger share of stored water to remain available for power stations, irrigation and urban supply.

Against this backdrop, Renewable Watch examines the current status of the floating solar segment in India, the cost economics, project case studies, the key challenges and the future outlook…

Potential and current deployment: Around 100 GW is technically feasible, but less than 1 GW is operational

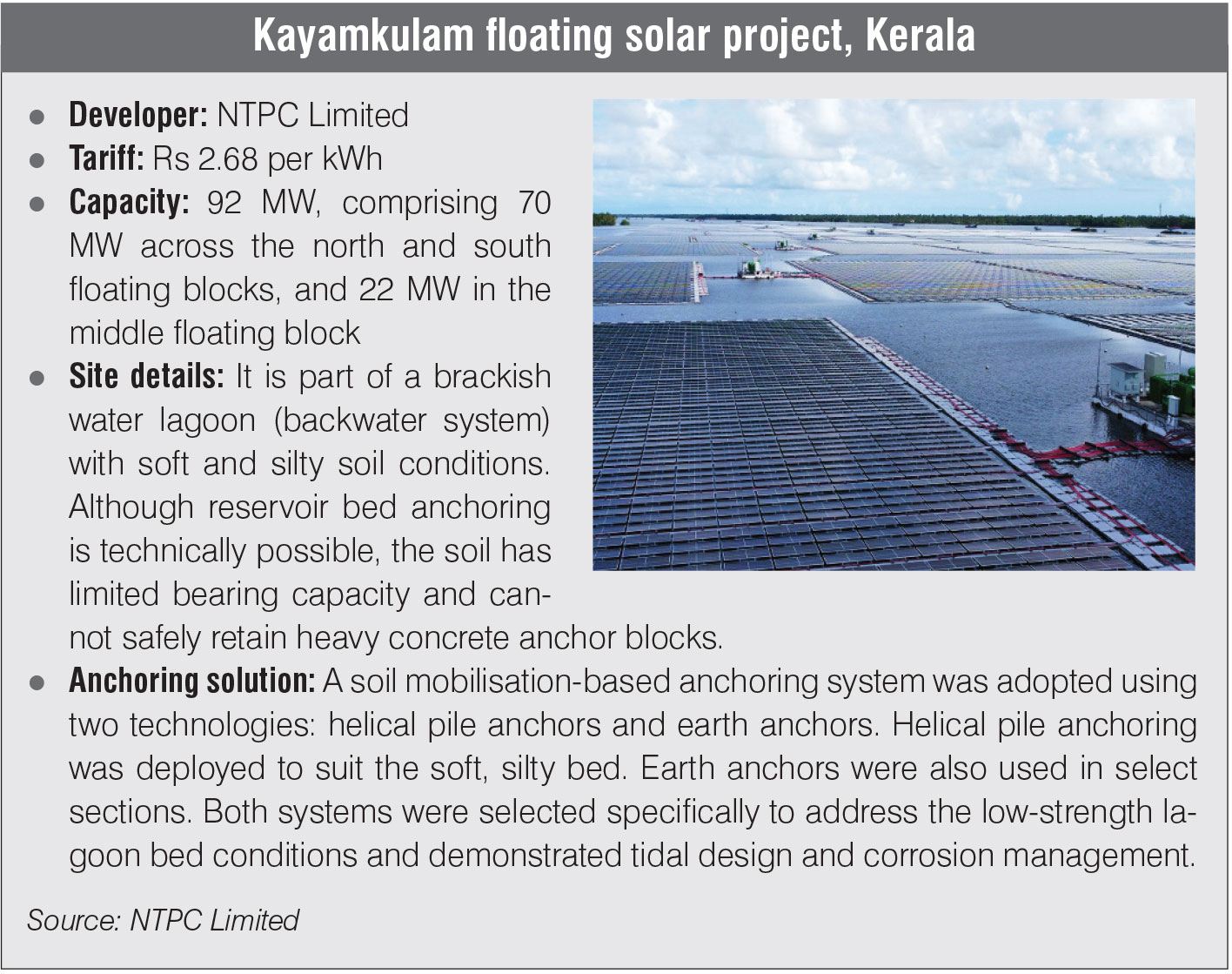

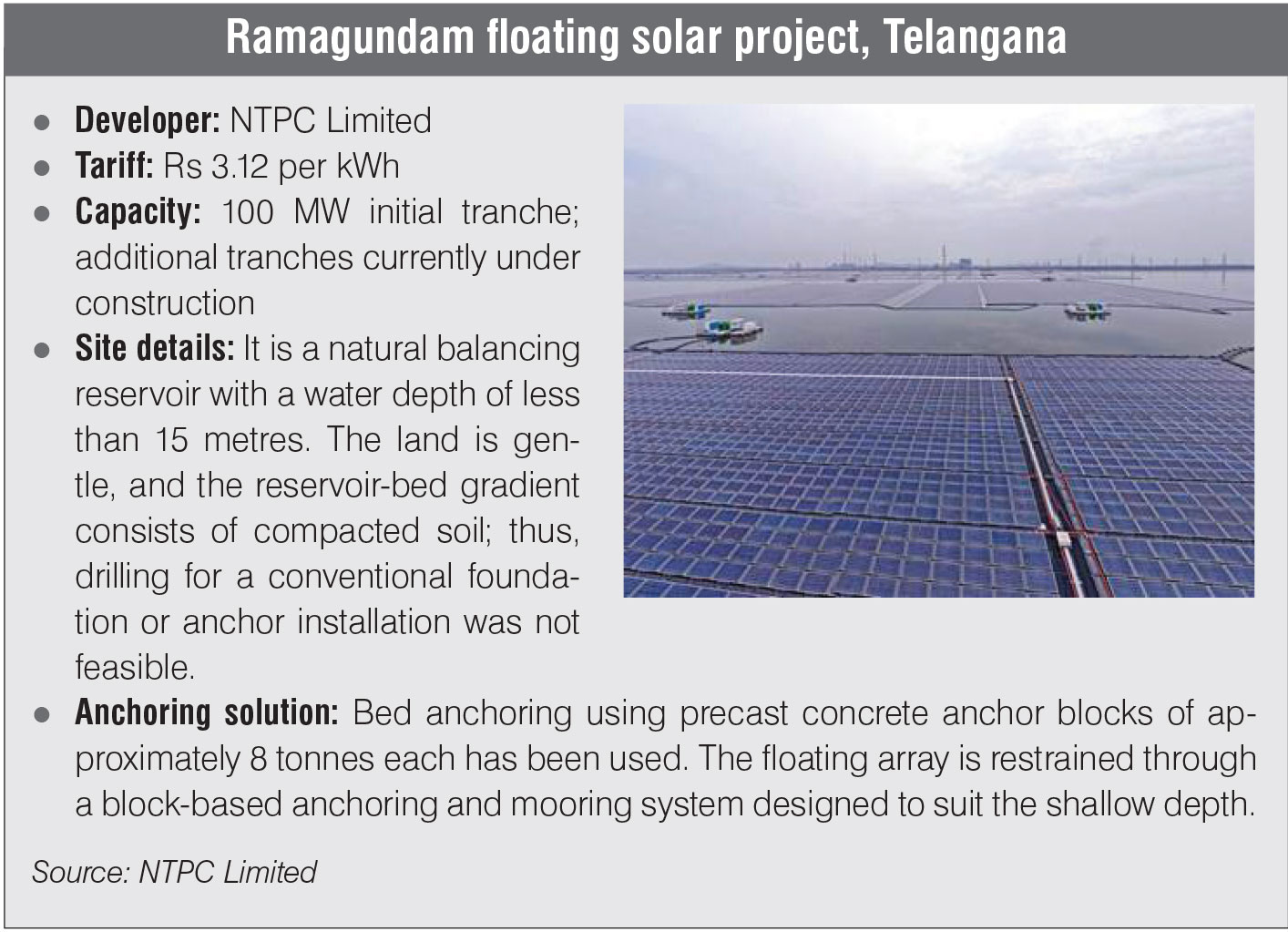

Despite a large potential, the actual FPV deployment is modest, with installed capacity at well below 1 per cent of what is technically feasible. As per The Energy and Resources Institute’s 2025 micro-level reassessment, the practical estimate for FPVs on man-made reservoirs is roughly 100 GW. This comprises 55 GW at reservoirs/barrages, 37 GW at tanks/ponds, 3 GW at inland aquacultures and 5 GW at coastal aquacultures. As of October 2025, about 600-700 MW of FPVs have been commissioned and about 1 GW is under construction, as per a guest article by Vaibhav Singh, executive director, PwC, in Renewable Watch’s November 2025 issue. A substantial part of the commissioned capacity is concentrated in a few large projects, including the Omkareshwar solar park in Madhya Pradesh with a commissioned capacity of 278 MW, the 100 MW Ramagundam plant (on the Singur reservoir in Telangana), and the 92 MW Kayamkulam plant (on the Vembanad backwaters in Kerala).

Cost economics: Installation cost for FPVs is around Rs 60 million per MW, while their tariffs average Rs 3.63 per kWh

Recent project tariffs for FPVs highlight a wide variation, driven by site conditions and project scale. NTPC’s 100 MW Rihand floating solar project was awarded at Rs 3.36 per kWh in August 2019, while the 2 MW Darbhanga project in November 2019 was awarded at Rs 4.15 per kWh. The 15 MW Nangal project, awarded in February 2022, recorded a tariff of Rs 3.26 per kWh. Omkareshwar Phase I, awarded in May 2022, had a tariff of Rs 3.21 per kWh, while Omkareshwar Phase II, awarded in November 2022, recorded a higher tariff of Rs 3.79 per kWh. The 105 MW Erai floating solar project awarded in October 2022 saw a tariff of Rs 3.93 per kWh. The 10 MW Phulwaria project in Bihar, awarded in December 2023, was won at Rs 3.87 per kWh, while the 100 MW Getalsud floating solar project in Jharkhand, awarded in March 2024, was discovered at a tariff of Rs 3.50 per kWh.

Overall, across all eight projects mentioned, the average tariff is about Rs 3.63 per kWh, with tariffs ranging from a low of Rs 3.21 per kWh (Omkareshwar Phase I) to a high of Rs 4.15 per kWh (2 MW Darbhanga), as per Renewable Watch Research. Larger projects of around 100 MW and above, such as Rihand, Omkareshwar Phase I, Omkareshwar Phase II, Erai and Getalsud have an average tariff of about Rs 3.54 per kWh. In contrast, smaller projects below 20 MW (Darbhanga, Nangal and Phulwaria) show a higher average tariff of around Rs 3.76 per kWh. This indicates that smaller and more site-constrained reservoirs tend to carry a tariff premium. A similar disparity is also visible at the state level. Projects located on large, utility-owned reservoirs in Madhya Pradesh and Uttar Pradesh have generally delivered lower tariffs compared to projects on smaller municipal and irrigation reservoirs in Bihar and Jharkhand, where anchoring complexity, site access and power evacuation arrangements are more constrained.

As per Renewable Watch Research, since 2022-23, floating solar tariffs have been around 6.8 per cent higher than solar-wind hybrid tariffs, with hybrid projects averaging about Rs 3.40 per kWh over the same period. Floating solar tariffs have also been around 33.3 per cent higher than utility-scale ground-mounted solar tariffs, which have averaged about Rs 2.723 per kWh, and about 6.3 per cent higher than onshore wind tariffs, which have averaged about Rs 3.415 per kWh. In contrast, floating solar tariffs have been around 25.7 per cent lower than round-the-clock/firm and despatchable renewable energy tariffs, which have averaged around Rs 4.884 per kWh.

As per Renewable Watch Research, since 2022-23, floating solar tariffs have been around 6.8 per cent higher than solar-wind hybrid tariffs, with hybrid projects averaging about Rs 3.40 per kWh over the same period. Floating solar tariffs have also been around 33.3 per cent higher than utility-scale ground-mounted solar tariffs, which have averaged about Rs 2.723 per kWh, and about 6.3 per cent higher than onshore wind tariffs, which have averaged about Rs 3.415 per kWh. In contrast, floating solar tariffs have been around 25.7 per cent lower than round-the-clock/firm and despatchable renewable energy tariffs, which have averaged around Rs 4.884 per kWh.

In current market conditions, the total project cost for floating solar typically ranges between Rs 55 million per MW and Rs 65 million per MW, as per R.R. Maurya. Of this, modules account for about 55 per cent, while floaters and anchoring systems account for around 23 per cent, and the remaining 22 per cent consists of balance-of-system (BoS) components. GIZ points to a similar cost structure for floating solar projects. Its report, “Floating PV in India”, released in January 2024, assesses the total capital cost of FPV projects at about Rs 57.08 million per MW. Modules account for the largest share at 52.57 per cent, while floating structures, and installation and erection together contribute close to 23.78 per cent. BoS components form the remaining 23.65 per cent of the total cost.

This cost structure also indicates that FPVs carry a clear capital premium over solar, wind and wind-solar hybrid projects. Project capex for FPVs is typically around 20 per cent higher for closed and relatively calm reservoirs, and 25 per cent or more for large dam reservoirs, as per Maurya’s presentation.

State-led policy support for floating solar: Dedicated guidelines in a few states, but no national framework yet

Floating solar has received dedicated support at the state level in some states. Odisha issued the “Guidelines for Establishing Floating Solar PV Power Projects on Water Bodies” in January 2025, with the aim of developing 1 GW of capacity by 2030 and providing a structured framework for FPV projects. Kerala issued the “Guidelines for the Development of Floating Solar Power Plants” in March 2025, introducing a structured approval and single-window clearance process for projects on reservoirs and urban water bodies.

Floating solar has received dedicated support at the state level in some states. Odisha issued the “Guidelines for Establishing Floating Solar PV Power Projects on Water Bodies” in January 2025, with the aim of developing 1 GW of capacity by 2030 and providing a structured framework for FPV projects. Kerala issued the “Guidelines for the Development of Floating Solar Power Plants” in March 2025, introducing a structured approval and single-window clearance process for projects on reservoirs and urban water bodies.

Other states have integrated FPVs into their broader solar or renewable energy policies. Madhya Pradesh’s “Renewable Energy Policy, 2022” promotes FPV on its dams and reservoirs. Uttar Pradesh recognises floating and reservoir-based solar under its Solar Energy Policy, 2022, having identified 35 reservoirs for floating solar in 2024. In 2025, it further shortlisted six sites with a total potential of 440 MW, and approved a 49 MW FPV at the Maudaha dam in Lalitpur district with GAIL as a developer in December 2025. Telangana’s “Clean & Green Energy Policy, 2025”, issued in January 2025 along with associated reservoir-allocation mechanisms, has established institutional procedures for allocating water bodies for renewable projects. In June 2025, Assam incorporated floating and canal-top solar within the scope of its “Assam Solar Power Generation Promotion Policy, 2025”.

Most other states have not issued any FPV-specific guidelines or policy instruments so far, with the concerns addressed through isolated project-level approvals rather than a formal policy structure. At the national level as well, no dedicated floating solar policy or programme has been issued yet. The central government still covers FPV indirectly under the broader solar power and renewable energy development framework, without separate targets, standardised reservoir-allocation rules, or nationally defined technical and environmental guidelines.

so far, with the concerns addressed through isolated project-level approvals rather than a formal policy structure. At the national level as well, no dedicated floating solar policy or programme has been issued yet. The central government still covers FPV indirectly under the broader solar power and renewable energy development framework, without separate targets, standardised reservoir-allocation rules, or nationally defined technical and environmental guidelines.

Sector concerns and outlook

While cost premiums exist, economies of scale, existing evacuation infrastructure, simple site conditions and growing competition are improving project viability

FPVs’ higher capital cost over ground-mounted projects is driven almost entirely by the need for floating platforms and site-specific anchoring and mooring systems, which are highly site-dependent. Anchoring costs rise sharply with increasing water depth and higher seasonal water level variation, as longer mooring lines, heavier anchors or pile-based solutions are required. Additionally, in large reservoirs with long wind fetch, wave barriers and protective structures are often needed to shield the floating arrays from waves and debris flow, further pushing up capital costs. This means that floating solar becomes financially attractive only where land constraints are severe, grid access is already available at the reservoir or power station, and anchoring conditions are relatively simple.

However, encouragingly, project costs are gradually improving. Higher volumes, growing competition among floater and anchoring suppliers, and more standardised plant layouts are steadily reducing non-module costs.

Engineering and design challenges persist, making it critical to build long-term capability

Unlike standardised land-based solar parks, FPVs require iterative and site-specific engineering. Water levels in many reservoirs change sharply during the monsoon, and this creates continuous movement in the floating structure and mooring lines. In large reservoirs, wind and wave forces become a major design challenge. In addition, projects must operate under harsh environmental conditions, including high humidity, accelerated corrosion and biological growth on submerged and semi-submerged components. Moreover, the most difficult element remains anchoring and mooring design. Deep reservoirs and rocky or uneven lakebeds require customised solutions, including rock-bolted anchors and hybrid mooring layouts.

Additionally, the domestic supply chain is not yet mature, with limited engineering design capabilities. India currently has few specialised suppliers for floaters, anchoring systems and marine-grade BoS components. Design knowledge is still concentrated among a small group of vendors, and testing data on long-term material behaviour in Indian reservoir conditions remains limited.

Building long-term capability is therefore critical. Dedicated infrastructure for the testing and certification of floating solar components, including float materials, anchoring and mooring systems, and interconnection hardware, is required. Facilities for material testing, hydrodynamic model testing and structural certification will reduce design uncertainty and improve lender confidence in large projects.

Environmental concerns remain, but careful planning can enable sustainable growth

Environmental and ecological concerns remain a significant challenge for reservoir-based FPVs. Large surface coverage can reduce light entering the water, which may affect oxygen levels, aquatic vegetation and local biodiversity if not carefully planned.

Environmental and ecological concerns remain a significant challenge for reservoir-based FPVs. Large surface coverage can reduce light entering the water, which may affect oxygen levels, aquatic vegetation and local biodiversity if not carefully planned.

To address this, the systematic identification of scientifically realisable sites is important. This will require structured reservoir screening, bathymetric surveys and environmental assessments, supported by public agencies. Prioritising water bodies with lower operational and environmental complexity, such as balancing reservoirs and industrial water ponds, can allow faster scale-up before moving into larger and more sensitive multi-use reservoirs.

Sharp increase in capacity addition needed to harness the FPV potential

India’s floating solar segment is at a transition point. Having demonstrated technical feasibility through a limited number of large projects, it must now shift decisively towards more scalable deployment. The pace of deployment needs to pick up too. Achieving even 10 per cent of the 100 GW potential by 2030 would require annual additions of roughly 2 GW, a sharp increase from the current levels.

Going forward, the real test for floating solar will not be how many projects are announced, but how quickly these can move from site identification to commissioning, under a standardised and reliable national framework. FPVs have certainly created ripples across India; it’s time now to ride the wave.