By Aastha Sharma

By Aastha Sharma

India’s transmission sector is scaling up at an unprecedented pace to keep up with rising electricity demand and the rapid expansion of generation capacity, particularly from renewable sources. Network growth is no longer limited to adding line length, but increasingly focuses on higher voltage levels and the adoption of advanced technologies to facilitate bulk power transfer over long distances. At the same time, transmission planning and operations are becoming more forward-looking to enhance system resilience and operational flexibility.

Segment size and growth

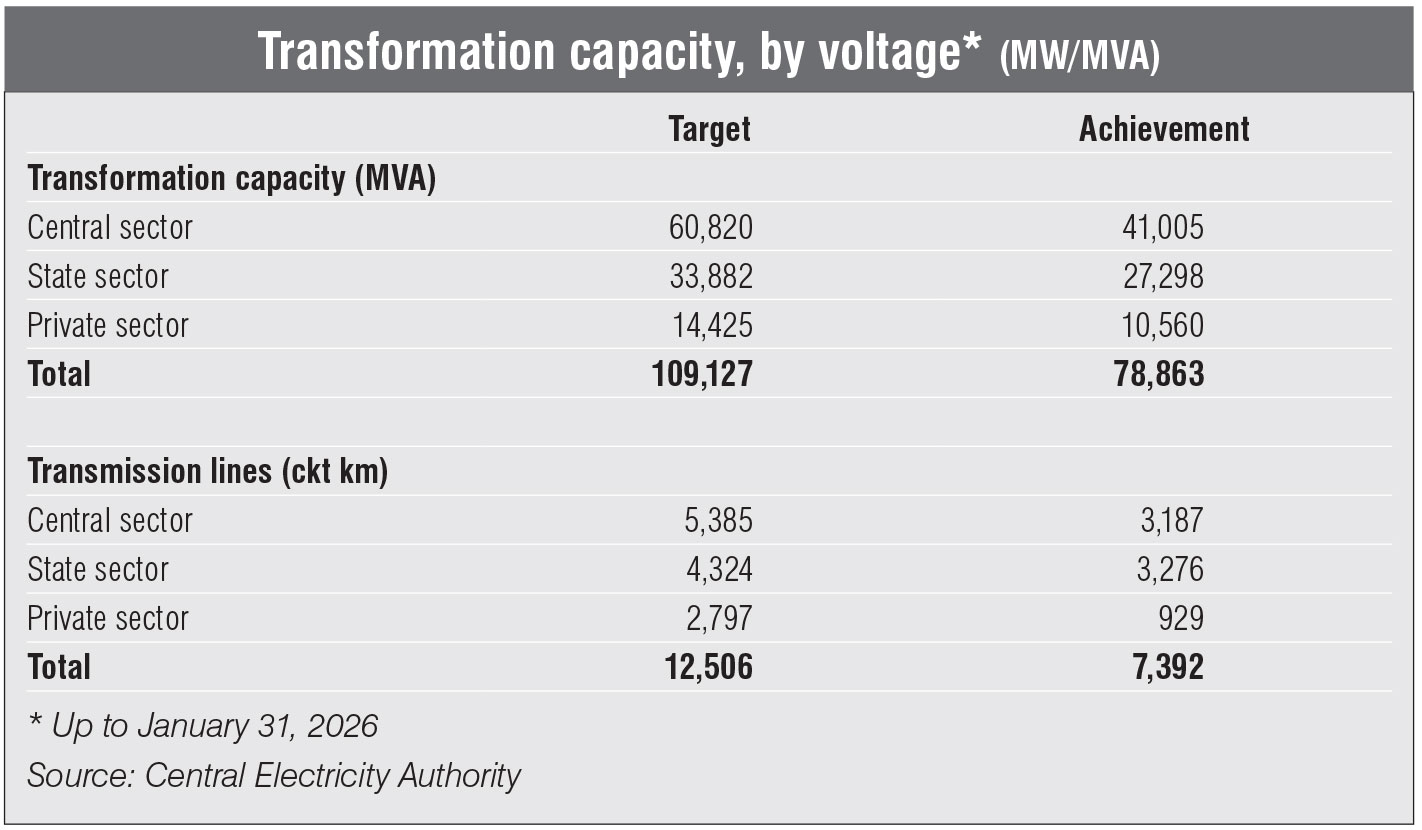

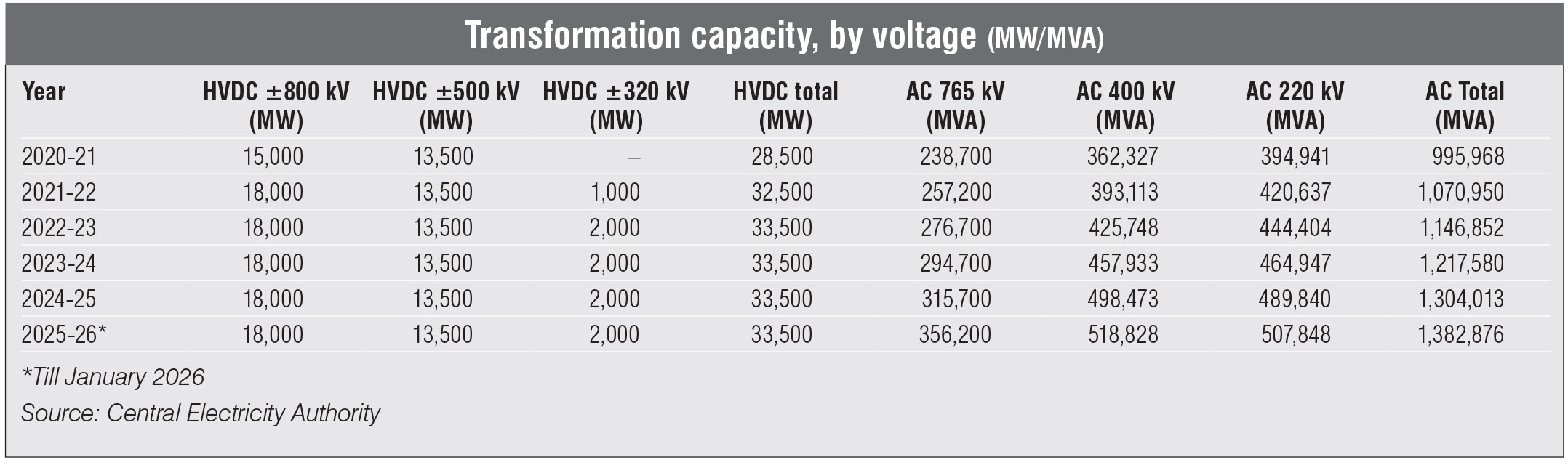

As of January 2026, the total length of transmission lines at the 220 kV level and above stood at 501,766 ckt km, comprising 59,891 ckt km at the 765 kV level, 208,639 ckt km at the 400 kV level and 213,861 ckt km at the 230/220 kV level. At the high-voltage direct current (HVDC) level, the line length stood at 9,655 ckt km at the ±800 kV level, 9,432 ckt km at the ±500 kV level and 288 ckt km at the ±320 kV level. During 2025-26 (up to January 2026), the transmission line addition target was set at 12,506 ckt km. Against this, 7,392 ckt km was achieved during the period (59 per cent of the annual target).

The transformation capacity across AC voltage levels stood at 1,416,376 MVA as of January 2026, with 356,200 MVA at the 765 kV level, 518,828 MVA at the 400 kV level and 507,848 MVA at the 230/220 kV level. Likewise, the aggregate HVDC capacity stood at 33,500 MW, with 18,000 MW at the ±800 kV level, 13,500 MW at the ±500 kV level and 2,000 MW at the ±320 kV level. Between 2019-20 and 2024-25, the AC transformation capacity grew at a CAGR of 6.7 per cent. During 2025-26 (up to January 2026), the transformation capacity addition target was set at 109,127 MVA. Against this, 86,433 MVA was achieved during the period (72 per cent of the annual target).

TBCB update

Tariff-based competitive bidding (TBCB) has grown significantly over the years, leading to faster project execution and greater private sector participation. As per the Central Electricity Authority (CEA), as of December 2025, a total of 84 transmission projects were awarded through the TBCB mechanism. Of the total awarded projects, 43 projects, with a transmission line length of 21,634 ckt km and a transformation capacity of 180,600 MVA, were secured by Power Grid Corporation of India Limited, and 41 projects were secured by private transmission service providers.

As of December 2025, a total of 74 transmission projects were commissioned under the TBCB route. Key private sector players in the segment include Resonia Limited, Adani Energy Solutions Limited, Tata Power Company Limited, IndiGrid Infrastructure Trust and Apraava Energy Private Limited.

In addition, several new entrants, such as Sekura Energy Limited, Renew Transmission Ventures Private Limited, Resurgent Power Ventures Private Limited, G R Infraprojects Limited, Dineshchandra R. Agrawal Infracon Private Limited, Megha Engineering and Infrastructures Limited, Reliance Industries Limited, H.G. Infra Engineering Limited, Shivalya Construction Company Private Limited and Techno Electric & Engineering Company Limited, have entered the transmission market.

Key policy and regulatory developments

In January 2026, the Ministry of Power (MoP) released the Draft National Electricity (NEP) Policy, 2026, to replace the 2005 policy. The draft placed strong emphasis on a flexible and consumer-oriented transmission system, with priority on strengthening intra-state networks and planning for open access-driven power flows. It assigned the CEA responsibility for preparing rolling 5-year and 10-year transmission plans, based on which Central Transmission Utility of India Limited and state transmission utilities were required to draw up capacity expansion plans addressing generation growth, congestion, redundancy and right-of-way (RoW) constraints.

In January 2026, the Ministry of Power (MoP) released the Draft National Electricity (NEP) Policy, 2026, to replace the 2005 policy. The draft placed strong emphasis on a flexible and consumer-oriented transmission system, with priority on strengthening intra-state networks and planning for open access-driven power flows. It assigned the CEA responsibility for preparing rolling 5-year and 10-year transmission plans, based on which Central Transmission Utility of India Limited and state transmission utilities were required to draw up capacity expansion plans addressing generation growth, congestion, redundancy and right-of-way (RoW) constraints.

In December 2025, the CEA released a Rs 6.42 trillion master plan to evacuate nearly 76 GW of hydropower and pumped storage capacity from the Brahmaputra basin. The plan proposed a phased transmission build-out of about 31,397 ckt km of lines, including 21,000 ckt km of HVDC corridors, and around 109,935 MVA of substation capacity to integrate the Northeast region’s hydro potential with the national grid. The first phase, scheduled up to 2035, covered about 9,922 ckt km of lines and 41,760 MVA of capacity, while the remaining was planned for implementation thereafter.

In September 2025, the Central Electricity Regulatory Commission notified the third amendment to the Connectivity and General Network Access Regulations, introducing procedural and compliance reforms. The amendments included provisions for the reallocation of unutilised ISTS bay capacities, revised renewable connectivity norms, stricter land and financial closure requirements, expanded eligibility for smaller renewable generators, and enhanced compliance monitoring by load despatch centres.

In September 2025, the Central Electricity Regulatory Commission notified the third amendment to the Connectivity and General Network Access Regulations, introducing procedural and compliance reforms. The amendments included provisions for the reallocation of unutilised ISTS bay capacities, revised renewable connectivity norms, stricter land and financial closure requirements, expanded eligibility for smaller renewable generators, and enhanced compliance monitoring by load despatch centres.

In March 2025, the MoP issued revised RoW compensation guidelines for transmission lines, introducing a two-part structure with 100 per cent land value for the tower base area and pro-rata compensation for the line corridor, based on the higher of the circle rate or the preceding year’s average sale deed rate. The norms apply only to future projects where work has not commenced, and compensation has not been disbursed. In January 2026, the supplementary guidelines were amended to fast-track valuation by mandating the appointment of three valuers on the same day and the selection of two reports by lottery to fix the reference market rate. If the variation between the two is within 20 per cent, their average is adopted; otherwise, the rate is capped at 10 per cent above the lower valuation or derived from the average of the two lowest valuations.

Technology implementation

The transmission segment is increasingly deploying advanced technologies to move bulk power efficiently over long distances, with HVDC corridors emerging as the backbone for evacuating renewable energy from solar parks, wind zones, pumped hydro projects and green hydrogen hubs to distant load centres. Key developments include the 6 GW, 950 km Rajasthan-Uttar Pradesh HVDC link being executed by a Hitachi Energy-Bharat Heavy Electronics Limited consortium, a planned undersea HVDC cable between the Andaman & Nicobar Islands and Odisha, a proposed India-Sri Lanka HVDC interconnection, and a large-scale HVDC-led transmission build-out for evacuating hydropower from the Brahmaputra basin under a Rs 6.43 trillion master plan.

Advanced conductor technologies are gaining traction, particularly high-temperature low-sag conductors that offer significantly higher ampacity and better performance. India has emerged as the largest market for these conductors, with reconductoring projects enabling substantial capacity enhancement on existing lines without tower modifications. Utilities are also selectively adopting insulated cross-arms, often in combination with advanced conductors, to increase voltage levels, improve clearances and reduce RoW requirements in constrained corridors.

To address land and space constraints, utilities are increasingly deploying steel monopole structures and narrow-based towers, which require smaller footprints, enable faster construction and are better suited for urban and semi-urban areas. Monopoles are now being used across several states to overcome RoW challenges and support infrastructure expansion alongside urban development.

To address land and space constraints, utilities are increasingly deploying steel monopole structures and narrow-based towers, which require smaller footprints, enable faster construction and are better suited for urban and semi-urban areas. Monopoles are now being used across several states to overcome RoW challenges and support infrastructure expansion alongside urban development.

Digitalisation is reshaping transmission operations and maintenance, with utilities deploying real-time monitoring systems, internet of things sensors, drones, geographic information system (GIS) platforms and advanced analytics to shift from time-based to condition-based maintenance. Dynamic line rating systems are being used to unlock additional capacity from existing assets through artificial intelligence (AI)-driven, real-time assessment of conductor capability, while digital substations with remote monitoring are enhancing operational efficiency at extra-high-voltage levels.

For renewable energy evacuation, these digital tools improve the real-time visibility of variable generation and enable more accurate forecasting and congestion management. Enhanced grid analytics and dynamic capacity assessment help minimise curtailment and maximise the utilisation of existing transmission corridors, thereby facilitating the smoother integration of large-scale solar and wind capacity into the grid.

The use of digital twins is expanding, enabling grid operators to simulate network behaviour, anticipate contingencies and optimise planning and operations by integrating supervisory control and data acquisition systems, phasor measurement units, GIS and sensor data. Drone-based inspections and robotics are becoming mainstream for surveying, construction monitoring and asset inspection, reducing safety risks, costs and outage requirements.

Renewable energy evacuation

Adequate transmission evacuation remains critical for large-scale renewable energy integration, with the Green Energy Corridor (GEC) scheme forming the backbone of green power evacuation. GEC Phase I, launched in 2015, targets about 24 GW across eight states through 9,767 ckt km of transmission lines and 22,689 MVA of substation capacity, of which around 9,136 ckt km and 21,413 MVA have already been commissioned. While Phase I has been completed in states such as Madhya Pradesh, Rajasthan, Tamil Nadu and Karnataka, progress in other regions has been affected by RoW and wildlife-related challenges.

GEC Phase II, approved in 2022, covers seven states, including Gujarat, Himachal Pradesh, Kerala, Uttar Pradesh and Tamil Nadu, and aims to evacuate around 20 GW through about 7,574 ckt km of lines and 29,737 MVA of capacity. The phase is being implemented by state transmission utilities with central financial assistance of 33-40 per cent and is scheduled for completion by 2025-26.

Further, GEC Phase III is currently in the advanced planning and preparatory stage, with the government working on its scope and state-level coverage. Discussions with states are under way, and initial project preparations have begun, indicating movement towards implementation. However, the phase is not yet fully rolled out or under nationwide construction.

Beyond the GEC framework, transmission development is being aligned with large renewable energy zones to support multi-gigawatt solar and wind parks through dedicated ISTS corridors. In parallel, dedicated green transmission is being planned for emerging segments such as green hydrogen and ammonia, with ISTS lines envisaged to support about 19-20 GW of green hydrogen capacity by 2030, offshore wind evacuation of about 10 GW, and coastal transmission infrastructure for nearly 70 GW of green hydrogen demand by 2032.

Outlook

Looking ahead, transmission expansion is set to accelerate in line with generation growth and renewable energy integration. As per the CEA’s NEP (Transmission), about 114,687 ckt km of transmission lines and 776,330 MVA of transformation capacity at 220 kV and above are planned during 2022-27, followed by another 76,787 ckt km of lines and 497,855 MVA of capacity during 2027-32. HVDC capacity additions are expected to scale up sharply in the latter period, reflecting the growing need for long-distance bulk power transfer.

Looking ahead, transmission expansion is set to accelerate in line with generation growth and renewable energy integration. By 2031-32, the transmission network is projected to reach about 648,190 ckt km of line length and 2,345,135 MVA of transformation capacity, supported by HVDC bipole capacity rising to nearly 66,750 MW. To enable this expansion and system strengthening, the NEP estimates a cumulative investment requirement of about Rs 9 trillion up to 2031-32.

Project execution visibility remains strong, with significant transmission capacity already under construction and a large pipeline of schemes under planning and bidding, indicating sustained investment momentum and robust growth prospects for the transmission sector over the medium term.