This is an extract from a recent report “World Energy Investment 2025” by International Energy Agency.

Overview of investment trends in India

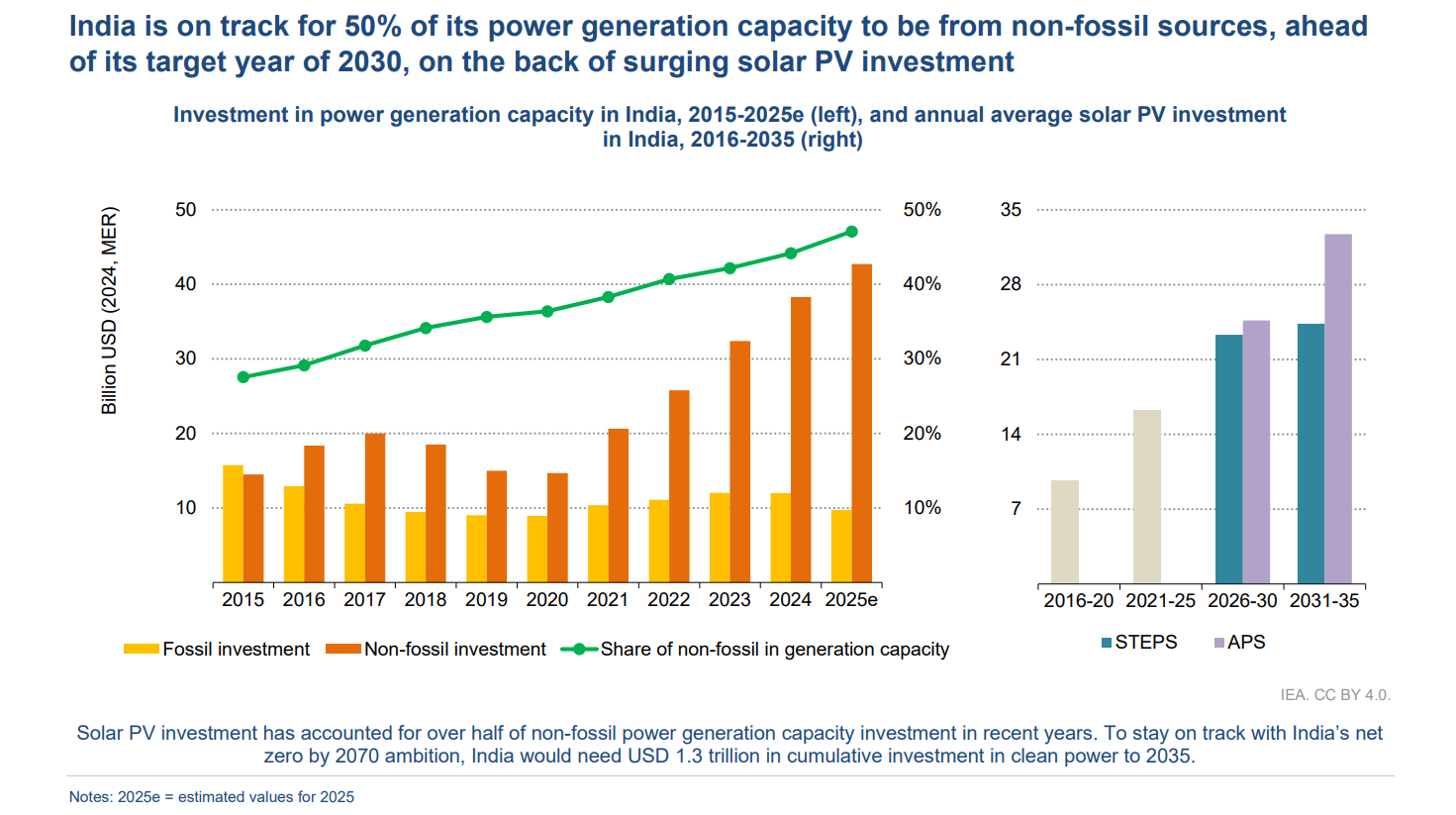

Electricity demand in India has been rising sharply owing to several factors, including increases in commercial and residential space, a surge in ownership of air conditioners and appliances and rising demand from industry. India has seen the third-largest growth in power generation capacity in the world after China and the United States over the past five years. While growth in power generation has come from all sources, there has been a surge in investment in renewables, led by solar PV, which constitutes over half of total non-fossil investment over this period. In 2024, 83 per cent of power sector investment went to clean energy. India was also the world’s largest recipient of DFI funding in 2024, receiving around $2.4 billion in project-type interventions in clean energy generation. This has helped bring the share of non-fossil power generation capacity to 44 per cent in 2024, approaching India’s target of 50 per cent by 2030. To meet these targets, and to stay on track to meet net zero by 2070, India will cumulatively need to invest $1.3 trillion in non-fossil power generation capacity to 2035. This is 16 per cent higher than the amount in the stated policy scenario in this period, signalling a shortfall in total investment under today’s policies.

This has helped bring the share of non-fossil power generation capacity to 44 per cent in 2024, approaching India’s target of 50 per cent by 2030. To meet these targets, and to stay on track to meet net zero by 2070, India will cumulatively need to invest $1.3 trillion in non-fossil power generation capacity to 2035. This is 16 per cent higher than the amount in the stated policy scenario in this period, signalling a shortfall in total investment under today’s policies.

Key government schemes

India has announced a range of measures to facilitate and support investment in power generation and its network. Notably in 2024 and 2025 India allocated over $3.5 billion in the PM Surya Ghar Muft Bijli Yojana, which has a target to install solar rooftop power generation systems in 10 million households by March 2027. For the current financial year, India has also committed $245 million to nuclear power projects, with the long-term vision of 100 GW of nuclear capacity by 2047, up from less than 10 GW today. These are among the recently announced measures that support longer-standing initiatives, such as the Production Linked Incentive scheme that encourages the domestic manufacturing of key energy components such as batteries and solar PV modules, the solar park initiative that promotes investment in utility-scale generation, and the Green Energy Corridor that has led to the investment of $2.6 billion in India’s transmission network to help evacuate electricity generated from renewable sources.

Foreign direct investment

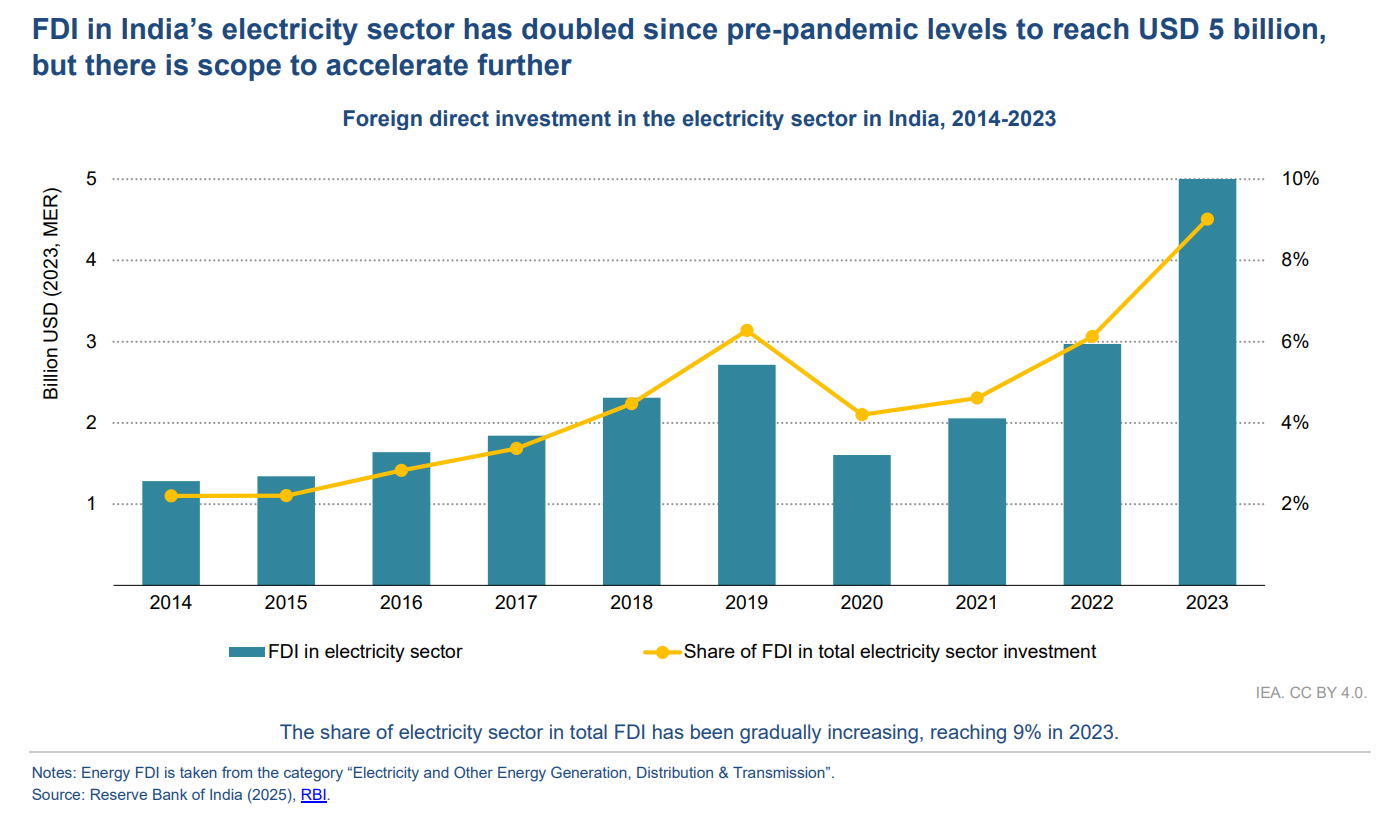

While a large share of the investment in India’s power generation capacity and transmission networks is met by domestic sources, foreign direct investment (FDI) has been growing steadily, reaching $5 billion in 2023, nearly double the pre-pandemic levels. This is promoted in part by rules permitting 100 per cent FDI across electricity generation sources (with the exception of nuclear) and transmission infrastructure. However, foreign portfolio investment (i.e., investment into financial assets such as stocks) in energy has taken a hit in the past two years due to a range of macroeconomic and sectoral factors, even as the longer-term trend has been one of steady growth. Challenges in renewable project execution

Challenges in renewable project execution

While India’s cost of capital for grid-scale renewable energy is one of the lowest among its emerging market and developing economy counterparts, it is still 80 per cent higher than in advanced economies. These higher financing costs affect the financial viability of projects, leading to higher energy prices. Real and perceived risks affect the attractiveness of projects to investors, both domestic and international. These include risks related to land acquisition, offtaker risk and risks arising from the inadequacy of transmission infrastructure, which has impeded 60 GW of renewable capacity in India.

Offtaker risk arising from the inability of distribution companies to pay generation companies fully and on time is cited as a key risk by investors. As of March 2025, distribution companies in India owed over $9 billion in unpaid dues. The accumulated losses of distribution companies in India stood at $75 billion in 2023. To address these risks, India has been incorporating a slew of reforms. These include Ujjwal DISCOM Assurance Yojana scheme, which seeks to improve the financial health of distribution companies by restructuring debt and promoting operational efficiencies; introducing late payment surcharge rules that penalise distribution companies for late payments to generation companies and provide a framework for clearing legacy dues; and establishing the Payment Security Mechanism of the Solar Energy Corporation of India, which includes escrow accounts, a payment security fund and state government guarantees in case distribution companies fail to pay developers. These are among the various measures that have sought to mitigate risks and unlock greater investment in the sector.

Access the full report here.