By Harman Mangat

India’s renewable energy sector, with a target of 500 GW of non-fossil fuel capacity by 2030, progressive policies and a large untapped market potential, has attracted substantial investments from global and domestic financiers.

In the past one year, the country has maintained its status as a favourable investment destination for global investors. Drawn by compelling valuations, strategic investors have poured in capital, aiming for more exposure in the renewable energy sector. Global energy majors including Petronas, TotalEnergies, Shell and Engie have deepened their ties and collaborations. A number of deals have been structured via bonds, debt, equity investment and mezzanine financing. Some acquisitions have put the spotlight back on consolidation in this space. Commercial banks, initially cautious about backing a nascent sector, have become key lenders to it. Global private equity (PE) investors have continued driving deal-making activity and clean energy initial public offerings (IPOs) have attracted widespread investor interest.

Renewable Watch takes a look at the key financing developments in the renewables sector over the past year…

Strong IPO momentum

The renewable energy sector is experiencing a surge in IPO listings. The broadening of the capital market has influenced available investor opportunities. In the past one year, the sector has raised around Rs 200 billion via IPOs, challenging the traditional dominance of fintech, consumer and real estate offerings.

Now, every company wants to go public. Medium- and large-sized players too are capitalising on the IPO momentum. Last year, Indian Renewable Energy Development Agency Limited’s (IREDA) Rs 21.5 billion IPO was oversubscribed by 38.8 times. Building on this momentum, NTPC Green Energy filed its draft red herring prospectus to raise Rs 100 billion. Post a successful listing, on day three, the IPO was subscribed 2.55 times overall. High-profile listings such as this one set the bar high for subsequent energy IPOs. Following this, ACME Solar launched an IPO worth Rs 30 billion.

Adding to the buzz, Waaree Energies’ IPO has garnered significant interest. The issue has already raised around

Rs 43 billion and is expected to do well further, considering solar energy is a key

theme in the ongoing transition to renewable energy.

With the Securities and Exchange Board of India recently imposing tighter norms , the energy IPO market has been strengthened further, filtering out speculative traders and retaining long-term investors.

In fact, recent listing debuts have given hope to other energy firms. Vikram Solar, Solar91 Cleantech, Satvik Green Energy and Regreen-Excel have filed draft papers, while Gautam Solar, among other companies, has reportedly announced IPO plans. Further, Premier Energies launched an IPO valued at Rs 28.3 billion, Matrix and Solarworld Energy secured Rs 3.5 billion and Rs 1 billion respectively in the pre-IPO round and Alpex Solar IPO achieved a 303 times subscription rate. Further, IREDA is considering raising around Rs 45 billion via qualified institutional placements (QIPs). Meanwhile, Indowind Energy has secured Rs 0.48 billion via the QIP route. Additionally, Orient Green Power has announced plans to raise Rs 2.50 billion via QIP.

Companies operating in the wind power segment such as Inox Wind and Suzlon Energy have also effectively utilised the capital market to fund their expansion, settle debt and pursue strategic initiatives.

Debt for development

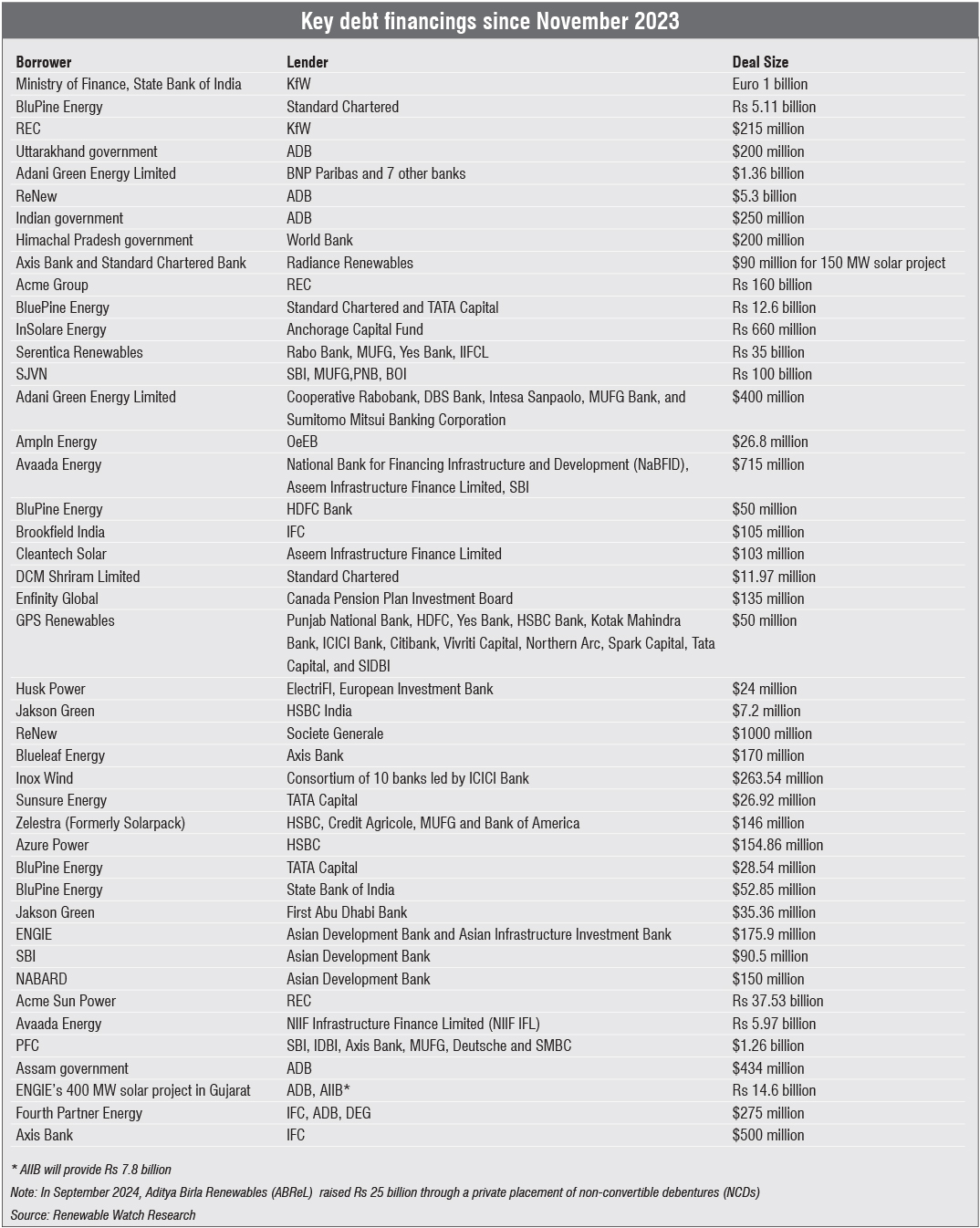

India has progressively strengthened its global market position in renewable energy. This growth has been supported by large amounts of domestic and global debt capital. As per Renewable Watch Research, between November 2023-November 2024, the debt market has touched over Rs 1 trillion.

Multilateral development banks such as the Asian Development Bank (ADB), Asian Infrastructure Investment Bank (AIIB), KfW and the World Bank have played a crucial role in channelling funds to the sector. Complementing these lending efforts, domestic commercial banks including Axis Bank, State Bank of India and Punjab National Bank, along with various state governments and energy companies have helped mitigate risk perceptions among investors. However, private non-banking financial companies, once pioneers in energy financing, have been slowly overtaken.

Key recent debt financings include ADB sanctioning a $434.25 million loan to support renewable energy development in Assam, a $240.5 million loan for solar rooftop projects and a loan, in collaboration with AIIB, worth Rs 14.6 billion for a solar PV plant in Gujarat.

Other recent debt deals include Sunsure Energy securing a long-term loan of Rs 2.26 billion from Tata Capital to strengthen solar projects and Cleantech Solar obtaining long-term green financing worth Rs 8.55 billion from Aseem Infrastructure Finance to expand its commercial and industrial (C&I) portfolio in India.

Equity moves

The renewable energy sector continues to attract long-term investors, with sustained interest from private equity and venture capital firms. The overall uptick in equity financing can be attributed to the robust pipeline of government-backed assets. As per Renewable Watch Research, during November 2023-November 2024, merger and acquisition activity, including asset sales, touched over

Rs 200 billion.

Various deals have taken place during the past year. Two key recent deals in the sector are Brookfield’s $845 million investment (via Brookfield Global Transition Fund II) in its joint venture (JV) with Hyderabad-based Axis Energy Ventures, and TotalEnergies’ investment of $300 million through a 50:50 JV with Adani Green Energy.

Asset sales and acquisitions of special purpose vehicles have also taken place. Recently, Reliance Industries Limited sold REC Solar Norway AS to Elkem ASA for around $22 million.

Big investments have also come in from sovereign wealth funds such as GIC, the Abu Dhabi Investment Authority, CPP Investments, and the National Investment and Infrastructure Fund. In a recent development, Enfinity Global signed a financing deal worth $135 million with CPP Investments for the development and construction of 1.2 GW of solar and wind projects. Global PE players such as Goldman Sachs, KKR and Global Infrastructure Partners have also contributed to the evolving investment landscape.

Banking on bonds

India’s green bond market has seen rapid growth in recent years. As per Renewable Watch Research, companies have increasingly tapped into both the domestic and international bond markets with the cumulative value of green bond issuances reaching over $45 billion till September 2024.

With the launch of its first sovereign green bond in 2023, the government has established a new route for financing climate goals. The performance of the first two tranches, worth Rs 80 billion each, exceeded expectations, with the issuance selling at a yield of five to six basis points lower than the sovereign yield of a similar tenor. The issue was oversubscribed by four times.

Building on this success, the Reserve Bank of India has announced plans to issue Rs 200 billion in sovereign green bonds in four equal tranches (Rs 50 billion each) during the second half of 2024-25. It may also exercise a greenshoe option of up to Rs 20 billion for each of these auctions.

REC Limited has also raised $500 million via green dollar bonds for a number of renewable energy projects. This was part of a $10 billion global medium-term programme of the company. The five-year note has a coupon rate of 4.75 per cent per annum, to be paid semi-annually. It has a maturity date of September 27, 2029. This is the first US dollar bond issuance by an Indian public sector enterprise in 2024.

All in all, these bond issuances have been indicative of a growing policy commitment to increase domestic financing capacity.

Financing outlook

In line with India’s climate and renewable energy goals, the government allocated Rs 191 billion to the Ministry of New and Renewable Energy in Union Budget 2024-25, which is 46 per cent higher than the previous year’s allocation. Besides continued budgetary support, private players have assumed bigger roles. For instance, JSW Energy and the Adani Group have announced investments worth Rs 1.5 trillion and Rs 2 trillion, and aim for 20 GW and 40 GW of capacity respectively by 2030. This sort of fiscal support and private investment are expected to accelerate sector growth.

Going forward, energy IPOs will remain a strategic investment opportunity. The solar, wind and green hydrogen segments are likely to maintain their robust investment trajectory while energy storage companies will emerge as a key asset class, attracting significant corporate funding and signalling the need for more debt and equity financing. For lenders, greenfield, hybrid, round-the-clock and C&I rooftop projects will remain key focus areas. PE interest is expected to persist, fuelled by rising energy demand and increased capacity addition targets. Continued interest from foreign investors will further boost inbound investments.

With rising confidence and domestic investors set to increase their allocation to the energy sector, green bonds are here to stay. Matured green bonds are also likely to require refinancing in the future. Furthermore, companies are on the look-out to refinance overseas debt with rupee bonds.

Despite all the positives, a few underlying challenges persist. These include the high cost of borrowing, the lack of working capital and readily available cash due to payment delays, and the risk of funding greenwashing projects. There is also the risk of investor interest dwindling if there are instances of corporate governance malpractices.

That being said, the Indian renewable energy financing landscape seems to be robust. With multiple sources of funding, a favourable policy environment (allowing 100 per cent foreign direct investment under the automatic route, for instance), soft loans from IREDA and capital subsidies from the government, these challenges are being overcome.

Key future investment focus areas include helping states accelerate the adoption of renewable energy, including flexible generation; battery storage and pumped hydro; domestic manufacturing of solar and wind components; and rooftop solar deployments. Future progress will hinge on collaborative efforts to reduce sector risks, attract strategic investments and tap emerging financing avenues.