As India accelerates its journey towards embracing green hydrogen as a sustainable energy source, important questions have surfaced about the urgency of this transition. Are we moving too fast into the green hydrogen era? Is it merely a speculative bubble? Should we wait for developed countries to drive down technology costs before we start making significant investments? These questions are indeed valid; however, it is essential to begin by addressing the fundamental question of “why” before delving into the “how”.

The “why” behind green hydrogen

The International Energy Agency estimates that hydrogen will contribute more than 10 per cent to the world energy mix by 2050 in a net-zero scenario. That is substantial, amounting to nearly $0.5 trillion of value globally. Hydrogen is crucial for decarbonising hard-to-abate sectors such as steel, heavy-duty transport, chemicals and certain manufacturing processes. Thus, there is a consensus that investing in hydrogen is a strategic move in the right direction. The next question is of India’s competitive positioning in the global context while we address the issue of timing.

India’s competitive edge

As India boldly enters the green hydrogen space, a crucial question arises: when is the right time to seize this opportunity? To answer that, we should first examine India’s competitive standing on the global stage.

As India boldly enters the green hydrogen space, a crucial question arises: when is the right time to seize this opportunity? To answer that, we should first examine India’s competitive standing on the global stage.

India is likely to be in the lowest quartile in terms of cost of production of green hydrogen globally. There are three reasons for this.

- Good quality of renewable energy resources, including ample solar and wind potential, along with a mature ecosystem for renewables.

- A vast and well-developed national transmission grid that allows renewable energy to be tapped at optimal locations, delivering cost-efficient electricity to hydrogen electrolysers.

- A strong talent pool in manufacturing, engineering and construction, offering both capability and cost competitiveness in building these projects.

Few nations can boast of such a trifecta of competitive advantages. However, one area where India faces a slight disadvantage is the cost of capital, which is a very important factor for green hydrogen development.

The timing dilemma

The consensus is that competitively, India is well positioned, but the central question revolves around timing. Should the nation adopt green hydrogen technology early or wait for further reductions in technology costs? Two compelling reasons support early action:

- Global trade opportunities: Early entrants have the opportunity to establish themselves as significant players in the nascent global hydrogen trade, securing substantial market shares and forming long-lasting trade partnerships. Estimates by Alvarez and Marsal suggest a global trade volume of $24 billion-$36 billion by 2030, which is likely to grow to $150 billion-$330 billion by 2050.

- Domestic industry decarbonisation: Embracing green hydrogen early will facilitate the early decarbonisation of the domestic downstream industry. There is no doubt that countries and companies that are better prepared for decarbonisation will gain long-term competitiveness in the global economy. This includes sectors such as steel, automotive and chemicals, where India has a large, well-established industrial base. Furthermore, the competitiveness of these sectors in a global market will be at risk if they do not prepare for a decarbonising world in advance.

Hydrogen can help these industries in achieving this goal, provided we have a hydrogen ecosystem. It is no surprise that the US and China, the two largest economies, have focused their entire hydrogen programme on domestic demand to get their downstream industries ready for the future! The rationale for early action is clear – to secure a larger share of the global trade and prepare the domestic downstream industry for decarbonisation.

The “how” of green hydrogen implementation

The most effective strategy at this juncture involves creating demand for hydrogen in downstream sectors. This approach not only fuels investments in upstream areas but also fosters supportive ecosystems and prepares downstream industries for the hydrogen transition.

The Indian government has already taken significant strides by introducing the generation-based incentive (GBI) scheme for hydrogen production and the production-linked incentive (PLI) scheme for electrolyser manufacturing. Moving forward, what India needs is a comprehensive programme designed to stimulate demand.

To achieve this, an approach of combining a mandate programme with a viability gap funding (VGF) scheme is proposed to incentivise the downstream industries to transition. In this context, priority sectors such as refineries, steel, fertilisers and heavy-duty transport may be identified in a calibrated fashion. For each of these sectors, a viability gap assessment can be conducted to determine the financial support required to transition to hydrogen in a phased manner. The VGF can be based on the current cost of green hydrogen production and the cost of adapting existing industrial processes to hydrogen.

We can draw inspiration from global models such as the German H2Global initiative, which serves as a market facilitator, bridging the viability gap between sellers and buyers.

Unlocking the green hydrogen potential

To illustrate the potential impact of such an approach, let’s consider the goal of creating a demand for 1 million tonnes of hydrogen by 2027. Assuming a viability gap of $1 per kg of hydrogen, this translates into an annual requirement of $1 billion in VGF.

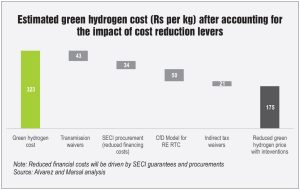

In tandem with stimulating demand, the second important lever is helping the hydrogen industry to reduce costs. While the government has already announced benefits in the form of interstate transmission cost waivers (which potentially save costs by 9-14 per cent) and banking of renewable power, in addition to the GBI and PLI schemes, there are a few additional areas that deserve attention.

- Lowering the cost of financing by de-risking projects: A critical aspect is de-risking projects by offering some level of offtake guarantees through take-or-pay arrangements. Initiating procurement models on behalf of procurers, similar to the successful SECI model for solar and wind, can significantly reduce costs.

- CfD model to enable RTC renewables: A unique contract for differences (CfD) model can be designed to enable round-the-clock (RTC) renewables especially for interstate supply of power to electrolysers. The temporal mismatches between renewable energy generation and electrolyser consumption are addressed by buying and selling power in the power exchange. The CfD will fund the difference between the buy price and the sell price, ensuring a predictable stable cost of renewable power for the electrolyser. Given potential constraints in wind capacities available for the hydrogen sector, this model will enable greater use of solar power in the mix, as the CfD allows its conversion into RTC power in the power exchange. This concept requires some debate among stakeholders.

- Reducing taxes on equipment: There is a need to address the impact of indirect taxes on equipment. Measures to reduce or refund the taxes can help to save 6-10 per cent in the final cost of hydrogen.

The implementation of these cost reduction strategies could lead to a substantial reduction of 43-46 per cent in green hydrogen production costs, enhancing its financial viability. These measures, while costly, may be provided to the first 1 million tonnes of hydrogen capacity, compensating early movers for the higher risks and costs they incur compared to late movers in a reducing cost curve environment.

Path to a sustainable future

While these initiatives require significant budgetary support, it is essential to view them in context. Our estimate is that the total outlay required to support this programme would be in the range of $4 billion-$12 billion cumulatively till 2030. This investment is expected to bridge the viability gap in different sectors and support cost reduction initiatives. While this number may look large, let us view this in the context of India’s economy and energy imports. Over the next seven years, India’s cumulative oil import bill will be in the range of a staggering $1 trillion-$1.4 trillion. India is exposed to a significant volatility of oil prices. During the past 10 years, our oil import bill ranged from a low of $64 billion (in financial year 2016) to a high of $158 billion (in financial year 2023).

In the long term, hydrogen will help mitigate this exposure for India. What we need is just about 1 per cent of our annual crude oil import bill to support the hydrogen economy. The payoffs are substantial: By 2030, hydrogen could provide approximately $3 billion-$5 billion in export revenues, substitute imports of $7 billion-$16 billion (mainly LNG), and do much more in the decades that follow. A bold stance by the government would make a difference, both in terms of inspiring confidence as well as bridging viability gaps. In essence, India stands at a crossroads: are we prepared to take bold steps to turn the hydrogen ambition into a reality?

By Santosh Kamath, Managing Director, Alvarez and Marsal