The operations and maintenance (O&M) of wind power plants plays a key role in the development of the wind energy segment and the broader energy transition, by ensuring that wind turbines are able to operate at their full potential during their useful life. In addition, the after-sales service business continues to be an increasingly important source of revenue and employment for the wind industry.

In this article, Renewable Watch looks at the market forecasts for the global wind O&M segment, and the future outlook…

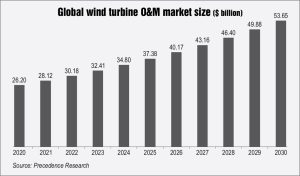

Market forecasts

In 2021, the Global Wind Energy Council (GWEC) stated that the global wind O&M service market will see double-digit growth from 2020 to 2024. According to the report, wind turbine and component suppliers generally capitalise on their relationships with asset owners from original equipment sales to sell their service offerings. However, some asset owners with large fleets provide their own in-house O&M services, or acquire independent service providers and specialised independent players to perform these services in order to reduce dependency on OEMs.

The high cost of O&M increases the share of the offshore segment in the global wind O&M value market. According to Lucintel, while offshore wind accounted for 22 per cent of the global wind O&M market in 2020, in terms of total wind installations, it contributed only 5 per cent. Offshore wind O&M is almost 4-5 times more expensive than onshore O&M. Meanwhile, the global wind turbine O&M market is expected to reach $27.6 billion by 2027 from $17.9 billion in 2020, growing at a CAGR of 6.4 per cent, according to a report by Research and Markets. The onshore wind turbine O&M market, meanwhile, is projected to record a CAGR of 4.7 per cent and reach $22.3 billion by the end of this period. However, the CAGR of the offshore wind turbine O&M segment has been revised to 17.6 per cent for the next seven-year period.

Geographical trends

Geographically, Europe is the largest wind O&M market, followed by Asia Pacific (APAC) and North America. China and Taiwan are the major contributors in the APAC offshore O&M market. The global wind O&M market of $28.6 billion in 2025 can be broken up as follows: China 29 per cent, the US 14 per cent, Germany 10 per cent and others 47 per cent.

In 2020, Europe had the largest share, accounting for approximately 46 per cent of the global O&M market, followed by APAC at approximately 34 per cent, North America at around 16 per cent, and the rest of the world at around 4 per cent. Onshore wind accounted for approximately 78 per cent of the total O&M market while offshore wind accounted for approximately 22 per cent. Low levels of accessibility and availability, as well as logistical issues, make offshore wind O&M services difficult to render, resulting in them being more expensive than onshore wind O&M. Going forward, a surge in the number of out-of-warranty wind turbines will greatly promote development of the wind farm O&M market, according to Lucintel.

According to a GlobalData report, “Wind Turbine Operations & Maintenance Market – Global Market Size, Trends, and Key Country Analysis to 2025”, China will be the largest wind O&M market in the world with a share of 27.4 per cent by 2025. This can be attributed to a rise in the installation of wind power projects in the country. A large installation base, government plans and strict environmental laws are the key drivers for the growth of the country’s wind power market and, consequently, its wind O&M market.

The US is expected to remain the second largest wind O&M market in 2025. Germany, the largest European wind O&M market, is expected to hold an 11.9 per cent share by 2025. These countries are expected to lose some market share due to the emergence of newer markets, such as India and the UK. According to GlobalData, the share of India in the global wind O&M market is expected to reach 6.4 per cent by 2025, while the UK’s share should reach 7.1 per cent.

It has been well established that offshore wind projects incur higher O&M costs than onshore wind projects. This is primarily due to their higher maintenance requirements and logistics costs, and the lack of skilled manpower. It is estimated that the offshore wind O&M market will continue to grow to reach $5.04 billion in 2025, representing an 18.4 per cent share of the total wind power O&M market. The UK, Germany and China will be the largest contributors, with investments of $1.46 billion, $0.86 billion and $0.69 billion respectively.

Future outlook

In view of technology and other cost considerations, the focus of the industry has shifted to reducing O&M costs. One of the main reasons for rising O&M costs in the industry is the failure of components such as blades and gearboxes, particularly in old wind turbines, and the high cost of logistics. With the growth of the industry and the entry of more companies providing specialised O&M services, the cost of wind O&M is gradually decreasing.

While the use of smart technologies is increasing the initial upfront costs, technological innovations are helping the industry reduce the overall wind O&M costs. One such innovation is the use of direct drive technology. This technology eliminates the gearbox, one of the major areas of failure in a turbine, thus reducing O&M costs in the long run.

While the use of smart technologies is increasing the initial upfront costs, technological innovations are helping the industry reduce the overall wind O&M costs. One such innovation is the use of direct drive technology. This technology eliminates the gearbox, one of the major areas of failure in a turbine, thus reducing O&M costs in the long run.

Tension control measurement technology for turbine bolts is another innovation that is helping reduce costs. Over 90 per cent of wind turbine failures are due to insufficient bolt tension in wind installations, and this can be minimised through proper tension control measurement, according to GlobalData.

Another common market trend is the use of predictive maintenance, which enables O&M service providers to schedule work in advance. This reduces O&M costs by reducing the number of plant visits and the manpower requirements, and allowing certain issues to be resolved remotely.

Going forward, increasing consolidation in the wind O&M segment is expected. Leading turbine OEMs have been continuously acquiring independent service providers. One of the key reasons for this has been the need to limit competition in the industry. This trend is expected to continue, going forward, as many players are interested in expanding to different countries.

However, growing bigger will not help O&M companies increase their margins and expand their operations. Service providers need to significantly invest in emerging technologies that not only improve the efficiency of wind plants, but also help in reducing costs in the long run.

According to Lucintel, the increasing use of predictive maintenance, artificial intelligence (AI), and drones with high definition cameras and thermal cameras for wind blade inspection; growing innovations with respect to key components; and an increase in the distance from shore and depth of offshore wind farms, are key emerging trends in the wind O&M market. To strengthen their position in this market, companies can target post-warranty turbines, long-term contracts and partnerships with wind farm owners in different regions to gain access to new locations and new customers. They can also increase the use of AI and automated drones for O&M services.

According to GWEC’s Global Wind Report 2023, with 78 GW, 2022 was the third-best year ever for new capacity added globally. The total installed global capacity reached 906 GW, representing a year-on-year growth of 9 per cent. GWEC expects this figure to reach 100 GW for the first time in 2023. Going forward, GWEC Market Intelligence forecasts 680 GW of new capacity addition from 2023-2027, at the rate of 136 GW per year. This significant addition will be a big positive for the wind O&M industry. However, the Indian wind market needs to catch up in order to provide better opportunities to domestic O&M players.