The central government’s announcement of a 37 GW bidding trajectory for offshore wind power up to 2029-30 could be a potential game changer for the segment. In line with this, the Ministry of New and Renewable Energy (MNRE) is expected to release an offshore wind tender in the next three to four months to lease 4 GW of wind energy blocks off the coast of Tamil Nadu. In a separate development, the ministry has released a strategy paper outlining various development models for utility and open access offshore wind power projects along with viability gap funding (VGF) and other financial incentives.

Offshore wind is a clean, affordable and scalable resource. These projects have higher plant load factors (PLFs) and are more efficient compared to onshore projects. These factors make offshore wind an important resource for the country’s energy security. In view of its complementary nature with solar power, offshore wind is useful in providing round-the-clock clean power, and managing peak demand in the country.

Recent developments to create a competitive offshore wind market will help elevate the wind industry’s sentiment, and accelerate India’s journey towards its green energy goals. “Offshore gives great opportunity with higher PLF and the government is moving in the right direction. The technology and size of the turbine do not pose a problem on the manufacturing side,” says D.V. Giri, secretary general, Indian Wind Turbine Manufacturers Association.

37 GW bidding trajectory for offshore wind

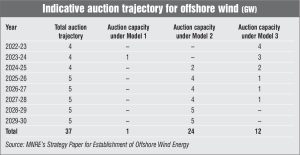

As per the central government’s bidding trajectory for offshore wind energy projects, 37 GW of wind energy projects are planned to be bid out by 2029-30.

- A project capacity of 4 GW per year for a period of three years will be bid out, starting with the current financial year (2022-23), for development off the coast of Tamil Nadu and Gujarat. The power from these projects will be eligible for open access/captive consumption/bilateral third-party sale/merchant sale.

- Subsequently, a project capacity of 5 GW will be bid out every year for a period of five years, that is, up to 2029-30.

The project capacity of 8 GW bid out in the first two years starting 2022-23 will be entitled to the benefits of green attributes like carbon credits. Bidding for the first 12 GW will be conducted on a single-stage two-envelope model, wherein bidders will be evaluated based on their techno-commercial capabilities and only the technically qualified bidders will proceed to financial evaluation. Financial evaluation will be based on the quoted lease fee per square km of seabed area. The bidder offering the highest lease fee per square km of seabed area will be declared the winner for allocation of the project.

The evacuation and transmission of power from the offshore pooling substation to onshore transmission will be provided free of cost for all offshore wind capacities that will be bid out up to 2029-30. The MNRE, through its implementing agency, will issue the first bid in the next three to four months for leasing out offshore wind energy blocks equivalent to 4 GW capacity off the coast of Tamil Nadu.

MNRE’s strategy paper for offshore wind energy projects

The MNRE has released a strategy paper outlining development models for the establishment of offshore wind energy projects.

Model 1: Under the first model, which will be followed for demarcated offshore wind zones where the MNRE/National Institute of Wind Energy (NIWE) has carried out detailed studies, the MNRE (or its designated agency) will enter into a lease agreement for a 30-year period with the successful bidders.

The offshore wind power developer will be required to pay the annual floor lease fee of Rs 100,000 per square km per year. Currently, one zone off the coast of Gujarat will be considered under the model.

Model 2 (A): Under the second model applicable to offshore wind sites identified by the NIWE for which detailed surveys have not yet been carried out, the developer may select a wind site within the identified zone and carry out the required surveys. The MNRE, through its implementing agencies, will issue bids fo

r the procurement of 2 GW of offshore wind power capacity tentatively in financial year 2024-25. Necessary central financial assistance in the form of VGF for initial p

rojects will be provided to achieve a predetermined tariff for these projects.

Model 2 (B): Developers that have carried out studies and surveys may also develop offshore wind projects for sale of power on a merchant basis or under bilateral agreements through the open access route or for captive consumption. The benefits of this model are provision of the power evacuation infrastructure from the offshore pooling delivery point, waiver of transmission charges, renewable energy credits with multipliers, carbon credit benefits, etc. as determined by the Government of India or the state government from time to time.

Model 3: NIWE will identify from time to time large offshore wind zones within the exclusive economic zone, but not covered under the other two models. The proposed offshore wind sites within these zones would be allocated for a fixed period on a lease basis through single-stage two-envelope bidding. Project development will be carried out by the prospective developer and the power generated from the projects will be either used for captive consumption under the open access mechanism or sold to any entity through a bilateral power purchase agreement or through the power exchanges. Benefits like provision of the power evacuation infrastructure from the offshore pooling delivery point, waiver of transmission charges, renewable energy credits with multipliers and carbon credits as determined by the central government or state government from time to time will be applicable. The evacuation of power from the offshore pooling delivery point to the onshore meeting/interconnection point will be the responsibility of Powergrid for all the above models. Meanwhile, the developer will set up the offshore wind project, including the offshore pooling station, at the 220 kV voltage level. Metering for the purpose of energy accounting will be done at the respective onshore pooling stations.

Issues and challenges

Despite the enormous potential, offshore wind energy development in India is lagging. The offshore wind power policy was release in 2015, besides there is a target for setting up 30 GW of offshore capacity capacity by 2030. How ever, no project taken off in the segment yet. This is attributable to significantly higher costs for off shore wind projects compared to other renewable energy sources. The tariffs for offshore wind energy are significantly higher than those for onshore projects and other renewable energy source. Industry estimates suggest that the tariff for offshore wind energy projects is expected to be Rs 12-Rs 14 per unit, making it difficult for any entity to buy power unless there is VGF either on the project or on the tariff. Meanwhile, the component costs are higher for offshore projects. As per the Lok Sabha’s 17th Standing Committee on Energy, the per megawatt cost of an offshore wind turbine is two to three times the cost of an onshore wind turbine. The project development of offshore is very different from onshore. Offshore wind projects require a very different infrastructure at the port level along with material holding equipment, barges and other support ancillary services for project development inclusive of under-water cables. Building manufacturing capabilities near the ports would be crucial as component sizes for offshore are much larger and may be more costly to transport across longer distances. Other challenges are lack of financing, subsea cabling, grid interconnection and operation, and development of the transmission infrastructure. There is also uncertainty regarding data as offshore wind data and studies in India are largely inaccessible or insufficient at present.

Conclusion

One of the key positives in the offshore wind energy development is the maturing of off-shore wind energy technology and the subsequent softening of the equipment prices. Globally, offshore wind costs have come down by one-third of what it used to be a decade ago. This is due to the maturity of the local industries and with localisation of components and supply chain. Overall, in light of recent developments, the industry is upbeat about offshore wind energy development in the country after a lag of several years. This is expected to be an important resource in the country’s energy mix and contribute towards the country’s decarbonisation initiatives, green energy goals and energy security going forward. That said, the legacy issues and challenges such as lack of adequate funds, inadequate supporting infrastructure and transmission constraints need to be tackled for the segment to take off.