Asia is a leader in global development and growth, and some of the largest emerging economies are in the region – particularly in South Asia, which is home to more than 1.8 billion people. Countries in South Asia have made positive strides towards achieving the Sustainable Development Goals (SDGs), but the ongoing pandemic risks negating the progress made. It is estimated that 132 million people in South Asia could be pushed into extreme poverty due to loss of jobs and livelihoods as a result of the pandemic, and the region’s economy is set to shrink for the first time in four decades.

Sustainable Energy for All’s “Recover Better with Sustainable Energy Guide for South Asian Countries” highlights the opportunities, benefits and enablers that will help leaders from South Asian countries guide their countries on to a more long-term, sustainable and resilient development trajectory.

While Asia has made significant progress in providing energy in recent years, South Asia still has large populations without access to electricity and clean cooking. Except for Bhutan and the Maldives, countries in South Asia need to increase their efforts in providing electricity access, particularly in rural areas. The region has significantly reduced its electricity access deficits, particularly due to large-scale programmes and efforts by Bangladesh, India and Pakistan. However, in 2018 there were about 152 million people without access to electricity in South Asia, according to “Tracking SDG 7: The Energy Progress Report 2020”. Also, according to the report, there are an estimated 990 million people in South Asia without access to clean cooking solutions. The Maldives is the only country in the region to have over 95 per cent access to clean cooking, and while progress has been made by other South Asian countries, much more remains to be done.

With the onset of the pandemic, the region has faced challenges due to the collapse of international trade, reduced export orders and dwindling tourism, all of which have deeply impacted small- and medium-sized enterprises. According to a UNESCAP study titled “COVID-19 and South Asia: National Strategies and Sub-regional Cooperation for Accelerating Inclusive, Sustainable and Resilient Recovery 2020”, 140 million people from five countries in South Asia might lose their jobs, which are already unstable and informal. There is a need to make businesses more resilient to global shocks. The region has very diverse commerce and industry sectors, ranging from the textile industries of Bangladesh to the tourism hotspots of the Maldives and Nepal, and vast untapped energy efficiency and renewable energy potential that can be leveraged towards making industries more competitive, providing faster electricity access for productive use and creating new value chains and jobs. The uptake of energy efficiency and renewable energy will be critical to accelerating recovery and building resilient economies.

Country-wise progress

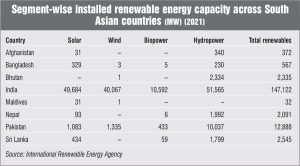

As of February 2022, India had a total installed renewable power generation capacity of 106.374 GW, with about 50.77 GW and 40.13 GW of this being attributed to solar power and wind power respectively. Over the past few years, the total solar power capacity in the country has overtaken wind power. This has mainly been due to policy and industry support for solar power, as well as the slowed-down growth in the wind space since the transition from feed-in tariffs to competitive bidding.

According to a report by JMK Research and the Institute for Energy Economics and Financial Analysis, India is projected to miss its target of having 100 GW of installed solar capacity (60 GW for utility-scale and 40 GW for rooftop) by 2022, by 22 per cent. This is particularly due to the slow uptake of rooftop solar projects (6.47 GW as of February 2022).

India’s neighbours also have high solar and wind potential, especially Pakistan. According to the World Bank, Pakistan can meet its current electricity demand by utilising just 0.071 per cent of the country’s area for solar power generation. Pakistan had announced plans to install over 1.5 GW of wind and solar between 2021 and 2023. In line with this, the country announced its decision not to approve new coal-fired power generation. In recent years, however, Pakistan’s share of renewables (solar, wind and bioenergy) has remained at around 4 per cent. The share of hydropower and nuclear is around 31 per cent and 8 per cent respectively. Likewise, Bangladesh has also planned to install over 1.2 GW of solar and wind capacity within a similar period of two years. In Bangladesh, while the share of renewable energy in the country’s power mix remains low, there is massive potential for solar and wind power. According to a report by the World Future Council. Bangladesh could deploy up to 156 GW of utility-scale solar power and 150 GW of wind power capacity.

Although the country fell short of its target of generating 10 per cent of its power from renewables by the end of 2021, it has now set a target of sourcing 40 per cent of the country’s electricity from renewables by the year 2041.

Sri Lanka also has promising potential in solar and wind energy. The country aims to add 350 MW of solar capacity by 2023. In the medium term, Sri Lanka hopes to add 1,000 MW of solar power and 780 MW of wind power by 2025. Recently, India and Sri Lanka signed an MoU to establish hybrid power plants in the island nation. The announcement came after the Sri Lankan government’s ousting of the Chinese company that had been cleared for these projects in 2021. The projects call for the development of three wind turbine farms in the Palk Strait, on the small islets of Nainativu, Analaitivu and Delft.

Other countries such as Afghanistan, Bhutan, Maldives and Nepal have witnessed slow growth of renewables. While Maldives is working on setting up microgrids and small-scale solar projects, the much larger Afghanistan has vast potential for solar, which remains unexplored. Geopolitical tensions in Afghanistan due to the Taliban’s rule are expected to derail the country’s efforts in the renewable energy space. Recently, India decided to import solar energy from Nepal, which will also join the International Solar Alliance, which is led by India. In addition, the participation of Indian firms in Nepal-based hydropower projects is also expected to increase, going forward.

The way forward

According to Mordor Intelligence’s “South Asia Renewable Energy Market – Growth, Trends, Covid-19 Impact, and Forecasts (2022-2027)” report, the South Asia renewable energy market is expected to grow at a compound annual growth rate of over 12.5 per cent in the forecast period of 2020-25.

Sustainable Energy for All’s “Recover Better with Sustainable Energy Guide for South Asian Countries” lists the key opportunities for South Asian countries in the renewable energy and energy efficiency space going forward.

Shifting investments towards utility-scale and decentralised renewable energy in the region would help not only in closing electricity access gaps, but also in developing energy security and avoiding stranded assets based on fossil fuel infrastructure. In many cases, renewables are the cheapest form of energy, so this shift can be achieved while lowering energy costs. South Asian countries should pursue large-scale investments in renewable energy to increase their share in the energy supply mix of the region. For example, they could aspire to invest 25 per cent of their stimulus budgets in on-grid and off-grid renewable energy (a combination of solar, hydro, geothermal and wind).

Governments should target direct and indirect investments that can bring down the cost of renewable energy systems considerably. Direct investments include loan guarantees or contributing capital for upfront investments. Indirect investments include the reduction or elimination of import duties and value added tax. Governments in South Asia have been committing more towards renewable energy in their national policy targets, but further efforts are required to develop the enabling policies, institutions and market to attract more investments. Covid-19 stimulus packages for the energy sector should not only be centred around clean energy but also be accompanied by market mechanisms that would incentivise investors and unpack the technological potential of integrating more renewable energy into the grid.

Countries in the region should also include support for clean cooking in stimulus budgets, targeting cleaner fuels and the supply chains needed to support the distribution of fuels and stoves, as well as public education to increase uptake. The use of clean cooking solutions such as improved cookstoves and induction cooking can contribute to fuel cost savings, reduced household air pollution, reduced drudgery-related fuel collection and more productive uses of time, according to the Global Alliance for Clean Cookstoves.

The investment potential for the renewable energy sector in South Asia between 2018 and 2030 is estimated to be around $411 billion. In 2017, the share of renewable energy in South Asia was about 42 per cent according to South Asia Monitor, but most of this was accounted for by biofuels and hydro. While there has been an increased uptake of solar and wind energy projects in the region with falling technology costs and stronger policies and incentives, the vast technical potential of solar and wind energy is yet to be realised. n