India’s wind energy segment has been suffering a slowdown. Progress in the segment was affected with the end of the feed-in tariff era and the launch of competitive bidding for allocating wind power projects. Capacity additions have been restricted, with barely 2 GW of annual installations since 2017 and a large pipeline of projects remaining stuck due to land and transmission constraints, and legacy power purchase agreement issues. The disruption in supply chains and labour activity due to the pandemic exacerbated this situation. However, the road to recovery looks promising. The wind market in India is showing positive signs of revival. The government’s plans to install 175 GW of renewable energy projects by 2022 and 450 GW by 2030 are expected to provide an impetus to this recovery.

The GWEC and MEC Intelligence have released the second edition of their joint report, “India Wind Energy Market Outlook 2025”, which provides a detailed analysis of wind power’s role as a critical link in the energy transition in India. The report aims to provide a perspective on wind power growth in the country from the point of view of the wind segment, and the current and future role of the industry in supporting India’s decarbonisation and climate goals.

Last year’s outlook report expected 2020 to be a breakout year for wind installations in India, thanks to a large pipeline and multiple policy interventions to ease execution bottlenecks. However, the impact of the Covid-19 lockdowns in India was more severe than anticipated. This year’s report forecasts a surge in wind power over the next five years. The report also lists the actions needed to speed up project installation in order to support the country’s ambitious goal of installing 450 GW of renewable energy capacity by 2030. Renewable Watch presents a summary of the report, with a focus on the wind energy outlook…

Background

Driven by economic and population growth, India’s electricity demand is projected to grow at 9.9 per cent per year till 2025. Although demand dipped in 2020 due to lockdowns, going forward, it is expected to exceed pre-Covid levels. Wind power continues to be a major constituent of India’s renewable energy-based grid-connected power generation mix. It makes up about 4 per cent of the overall share of electricity generation in the country. Between 2010-11 and 2019-20, wind generation capacity grew at a CAGR of 11.39 per cent, while the overall installed electricity capacity witnessed a CAGR of 8.78 per cent. India has high growth potential for wind power. On average, the levellised cost of energy for wind in India is roughly 35 per cent lower than most coal plants providing electricity. Further, the National Institute of Wind Energy has estimated the wind power potential at 100 metres to be 302 GW, which is equivalent to about 81 per cent of India’s current installed electricity generation capacity.

Market activity

Market activity

The transition to the auction regime in 2017 led to large orders but also impacted prices, evacuation availability, and land preference for the projects. Policy interventions have been introduced that address these issues, including the streamlining of the land policy in Gujarat and Tamil Nadu, augmentation of grid infrastructure in critical bottleneck substations, and fast-tracking of the power supply agreement between the Solar Energy Corporation of India (SECI) and distribution companies. During the pandemic year of 2020, only 1.1 GW of wind power capacity was realised, while nearly 0.8-1 GW of capacity scheduled for commissioning that year slipped into 2021. Further, against the outlook of 3.3 GW, around 1.1 GW of capacity was cancelled by developers or not granted timeline extensions.

Wind energy is emerging as a crucial link for India’s green energy transition story. As of March 2021, India has 39.2 GW of installed wind power capacity and is likely to add another 20 GW over the next five years owing to its cost and its role in producing round-the-clock power. India currently has a pipeline of 10.3 GW in the central and state markets, which is expected to drive installations until 2023. Post-2023, the market is likely to be driven by 10 GW of new capacity awards to wind, majorly in hybrid formats.

In this projected growth, there is a prominent role to be played by hybrid power generation in improving capacity utilisation factors and reducing the cost of renewable energy integration. In 2020, procurement happened in all three market segments – central, state and corporate – for new hybrid projects. During the year, 0.97 GW of new capacity was awarded in stand-alone tenders, along with an estimated 2.3 GW of wind capacity in the wind-solar hybrid, peak power, and round-the-clock formats, at continuously attractive prices. Tariffs for pure-play wind power declined to about Rs 2.77 per kWh in 2021 from Rs 3 per kWh in 2020. In contrast, wind-solar hybrid tenders discovered tariffs in the range of Rs 2.41 per kWh to Rs 2.42 per kWh, offering a bold value proposition for hybrid power.

Outlook

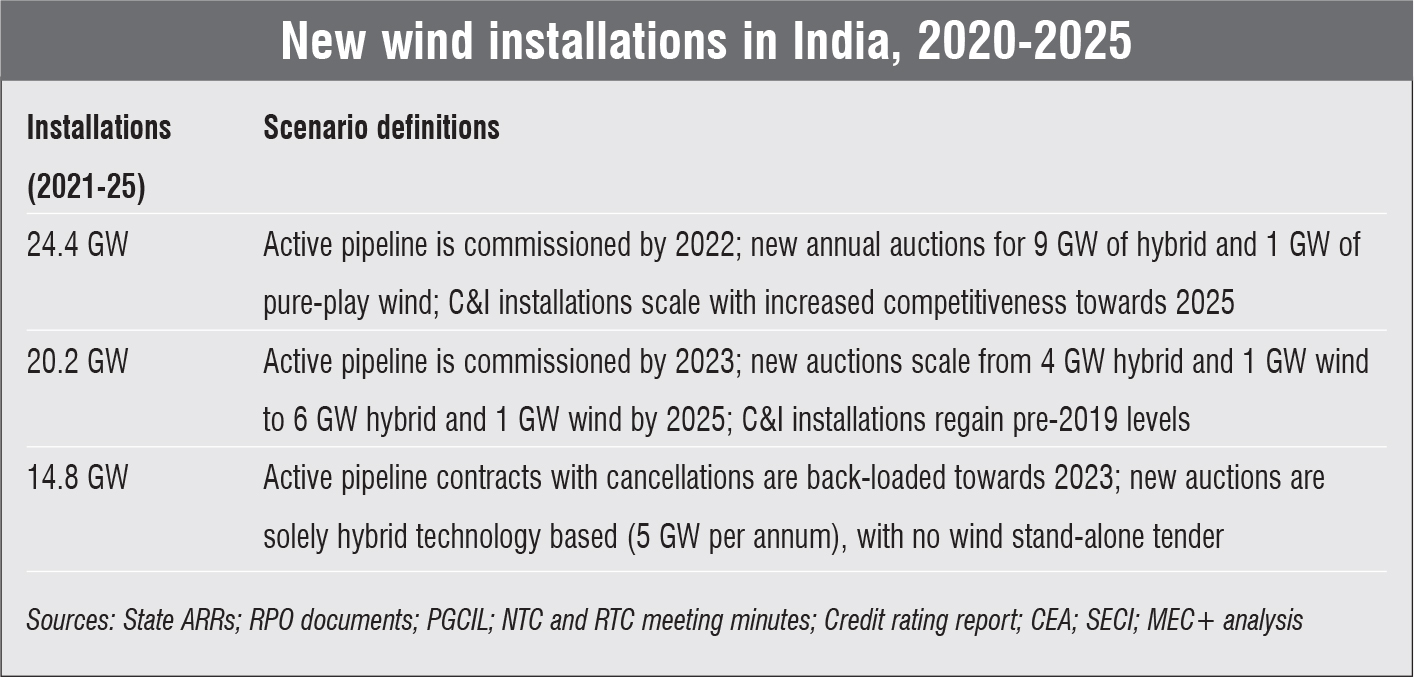

Over the period 2021-25, India is expected to install nearly 20.2 GW of wind capacity, 90 per cent of which will come from central tenders, followed by corporate procurement and, lastly, state markets. Supportive interventions have been introduced enabling the sale of clean power in a green power market, which is likely to emerge as an attractive avenue for resource-rich and surplus-producing states to earn revenues. In an ambitious scenario, nearly 24.4 GW of capacity can be expected in the next five years, driven mostly by high demand for price-competitive hybrid auctions. In a conservative scenario, the net volume installation can decrease to 14.8 GW if the existing pipeline shrinks and new auctions are limited or sporadic. New waves of the Covid-19 pandemic are likely to keep the situation closer to the conservative scenario. In addition to the wide range of volumes between scenarios, the market is expected to be uneven across the next five years. Among states, capacity is expected to move outside of Gujarat and Tamil Nadu into Karnataka and Madhya Pradesh for wind auctions and Rajasthan for hybrid auctions, given the diversification of bidding substations. Meanwhile, Gujarat and Tamil Nadu are likely to continue contributing the largest share in the volume commissioned.

Post-2025, the market will offer multiple opportunities including offshore wind, repowering, as well as the largely untapped potential of the commercial and industrial consumer base. The government is exploring multiple pathways to kick-start the offshore wind sector in India, including near-shore development, demonstration projects and decentralised development. In the context of repowering, India has the potential of nearly 2.9 GW of projects with sub-MW turbines and more than 15 years of operational lifetime. A repowering policy has been launched by the states of Gujarat and Tamil Nadu. By 2030, the repowering opportunity is likely to double with nearly 4.5 GW of potential for replacement. However, to realise the opportunity, there needs to be more clarity on incentives, land procurement and owner aggregation in order to bring in more investments. Developing India as an export hub will create another long-term growth driver.

Original equipment manufacturers and the wind supply chain continue to invest in building a manufacturing base in India for cost-competitiveness and regional export opportunities. India is already the second largest wind supply chain manufacturing hub in the world, with further expansions in the offing, in line with the government’s Make in India initiative.

The way forward

To properly utilise the wind resource potential in India, additional steps can be considered by various stakeholders. These include strengthening consensus and coordination between the centre and relevant states; charting out a road map defining volume, frequency, composition and pricing expectations; and improving supply chain utilisation. Improvement of supply chains would entail setting up of R&D facilities, removing trade and non-trade barriers for integration within the global supply chain, and facilitating technology transfer. n

Based on the report “India Wind Energy Market Outlook 2025”, published by GWEC and MEC Intelligence in June 2021

By Meghaa Gangahar