India’s renewable power capacity has reached 89 GW as of August 2020 on the back of timely policy interventions from the government as well as a competitive market landscape that attracts private sector participation and a large number of investors. However, recent months have witnessed a slowdown in solar and wind capacity addition along with waning investor interest due to sectoral challenges. The banking sector mess and the price volatility of currency have worsened the situation. This has been further exacerbated by the Covid-19 crisis, leading to a decline in overall investments as financiers wait and watch for conditions to stabilise before taking any new financing decisions. Thus, new innovative financial instruments need to be evolved to drive up private sector investments in order to enable the country’s energy transition.

This is especially important as, in September 2019, the country announced a target to achieve 450 GW of renewable power capacity by 2030. Based on India’s Nationally Determined Contribution, the country would require $ 170 billion annually for climate change-related mitigation activities. This translates to $ 2.5 trillion of investments between 2015 and 2030. Thus, India would need to match the set targets with the right investments, which is why identifying sources of finance, the instruments for mobilising this finance and their final destinations becomes significantly important. Against this backdrop, the report “Landscape of Green Finance in India” by the Climate Policy Initiative, supported by the Shakti Sustainable Energy Foundation, analyses the various green finance flows in India during 2016-17 and 2017-18 throughout their value chain, from source to end beneficiaries. Both public and private sources of capital as well as the financial instruments used for carrying these transactions have been tracked in this report. Finally, it identifies the various gaps and opportunities for scaling up green finance in India. Renewable Watch presents the key findings of the report…

Key findings

Key findings

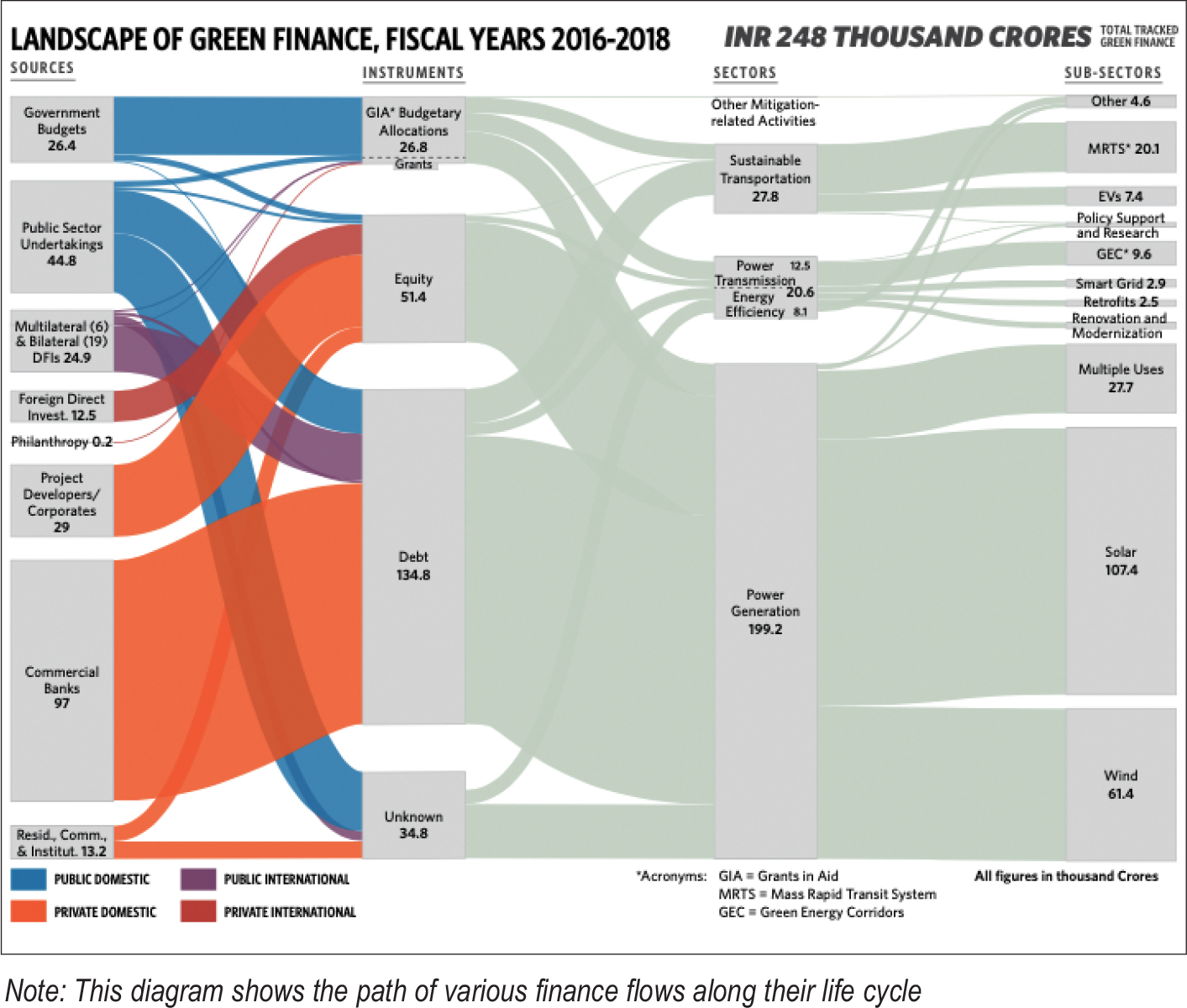

The total green finance flows tracked during the two years 2016-17 and 2017-18 amount to Rs 2,480 billion. Of this, the finance flows for 2016-17 total Rs 1,110 billion and for 2017-18, they total Rs 1,370 billion. The average annual finance flow for the two years is Rs 1,240 billion.

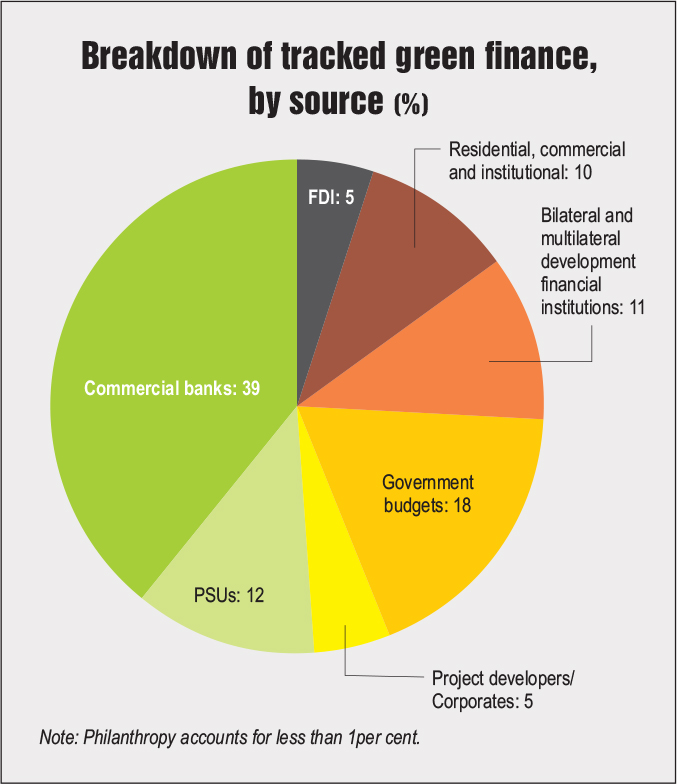

- Domestic sources of finance: During the years 2016-18, the largest share of green investments came from domestic private investors totalling about Rs 1,390 billion. The share of debt and equity was 63 per cent and 51 per cent respectively. Nearly 40 per cent of these funds came from commercial financial institutions and almost all the funds were directed towards renewable energy investments. Meanwhile, (37 per cent) of public finance came from central government ministries and state departments, and the bulk 63 per cent from dedicated public sector undertakings (PSUs). About 70 per cent of public finance was disbursed for power generation followed by 20 per cent in total for energy efficiency and power transmission, and 10 per cent for sustainable transportation. Based on the data tracked by the study, dedicated PSU expenditure on climate mitigation activities more than doubled in 2017-18 from 2016-17. At the same time, their budgetary allocations in these activities also increased by 36 per cent.

- International sources of finance: The tracked green finance flows from international public sources amounted to Rs 120 billion in both years, translating to a share of 10 per cent for both 2016-17 and 2017-18. Meanwhile, 75 per cent of official development assistance and other official flows were from bilateral agencies and the rest from multilateral agencies. About 56 per cent of the bilateral funds went towards financing sustainable transportation, in the form of loans for developing metro rail projects, and metro projects in Delhi and Mumbai received 45 per cent and 25 per cent of these funds respectively. At the same time, 40 per cent of multilateral funds were utilised for the development of solar parks and rooftop solar projects.

According to the study, for international private finance, equity was used in the case of foreign direct investment (FDI) while grants were used for philanthropy. Interestingly, FDI of Rs 120 billion each was allocated exclusively to clean energy in both 2016-17 and 2017-18. Wind and solar accounted for half of this amount. However, FDI in the clean energy space still accounts for only 1 per cent of the total FDI flows into the Indian economy.

- Dominant financial instruments: Debt remained the predominant financial instrument out of a myriad of options used by public and private actors. Meanwhile, grants-in-aid and budgetary allocations contributed 90 per cent of all the finance channeled from state budgets. This was utilised for direct mitigation activities such as procurement, installation, construction, renovation and maintenance of facilities as well as indirect activities such as research and development (R&D), and administrative expenditure. A significant amount of public funds were disbursed through several dedicated PSUs that supported essential indirect activities such as R&D, capacity building, and project finance through debt.

Sectors and subsectors for green finance

Nearly 80 per cent of the tracked green finance in 2016-17 and 2017-18 went towards power generation. Of this, 80 per cent went towards the solar PV and onshore wind power segments. Meanwhile, roughly 43 per cent of the average annual finance for both years went towards sustainable transportation. Capital expenditure on mass rapid transit systems and the sale of electric three-wheelers were the predominant contributors in this space.

A total of Rs 200 billion went towards the energy efficiency and power transmission segments over the two years. These investments focused on infrastructure development, retrofits, renovation and modernisation, smart grids, and green energy corridors. Driven by funding from domestic and international public actors, about 47 per cent of these investments went towards green energy corridor projects followed by smart grids at 14 per cent, under the National Smart Grid Mission. The main financiers, with 34 per cent share, included PSUs such as Energy Efficiency, and NTPC Limited, the Bureau of Energy Efficiency and NTPC Limited, while 33 per cent of finance came from central and state budget investments. The data for private investments is limited in the energy efficiency and power transmission space, and probably for this reason public financial institutions make up a larger share of these investments.

Outlook

During the course of the study, various challenges were identified in measuring green finance flows in India. These include non-availability of data on fund disbursement at multiple levels within the value chain, non-standardised reporting of data due to the lack of a harmonised green finance taxonomy in the country, large variations in granularity and format, and categorisation of data at the state level and data confidentiality issues arising from the absence of a climate-related financial disclosure policy in the country. Thus, it is critical to put emphasis on proper data tracking as this would help in understanding the status and need for green finance investments in the country.

Overall, the study indicates that India’s green investments are on the rise. However, the investments tracked during 2016-18 across the power generation, energy efficiency and power transmission, and sustainable transportation segments are far behind the estimated investment requirements mentioned in national and international studies, and represent just 10 per cent of the total finance requirement. Thus, a business-as-usual approach may be insufficient to address the issue of access to finance and more result-oriented measures may need to be explored. The study identifies two key opportunities to scale up green finance in the country. First, transparency should be increased via an integrated domestic measurement, reporting and verification system. This will streamline green finance attributes and identify financial constraints. Second, a comprehensive climate budget tagging framework should be developed to track climate-related expenditure in national budget systems. And last, building on the PSUs’ role in mobilising and increasing green capital flows, each PSU should be given more responsibility in line with their mandates, expertise and reach. This will further enhance private sector participation in green finance.

Based on the report “Landscape of Green Finance in India” by the Climate Policy Initiative