High upfront costs, low consumer awareness, lack of policy and regulatory structures, and poor project visibility have been some of the key impediments in the adoption of energy storage systems. Very few developers and utilities have paid serious attention to energy storage, despite its potential in facilitating renewable energy integration into the grid, delivering peak capacity without carbon emissions, instantly adjusting the frequency of the system, and more.

This scenario, however, seems to be changing. With battery costs falling and early adopters of energy storage liking what they have seen in initial trials, the cycle from pilot and evaluation to widespread adoption is speeding up. In the past one year, there has been a surge in the issuance of storage-based tenders, both big and small. Battery technologies have improved in terms of performance and efficiency. Tariffs too are accordingly becoming more attractive.

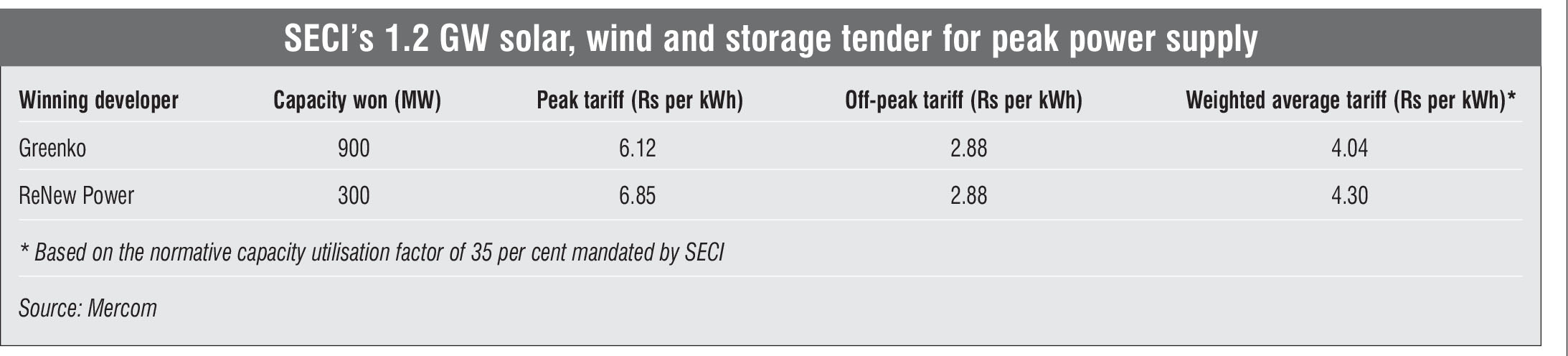

The results of the latest energy storage tender released by the Solar Energy Corporation of India (SECI) bear testimony to the growing developer confidence in battery storage technology. The procurement exercise was held by SECI to contract 1.2 GW of capacity in the form of assured supply of 600 MW of clean power for six hours per day during peak demand hours (5.30 a.m.-9.30 a.m. and 5.30 p.m.-12.30 a.m.) on a day-ahead, on-demand basis. According to sources, the successful bids comprised at least 3 GWh of energy storage capacity, including pumped hydro or battery storage and associated clean energy generation assets. The tender was aimed at securing reliable, fixed-price energy supply for state discoms, which are otherwise vulnerable to the vagaries of the spot markets.

The procurement round was oversubscribed, with bids received for 1.62 GW of capacity. Among the winners, Greenko secured 900 MW of pumped storage capacity with the most competitive tariff bid. The company offered a weighted average tariff of Rs 4.04 per kWh and a quoted peak tariff of Rs 6.12 per kWh. The second winner, ReNew Power, secured the remaining 300 MW of capacity with a weighted average bid of Rs 4.30 per kWh and a quoted peak price of Rs 6.85 per kWh. These tariffs mark a world record for renewables-plus-battery storage capacity. The weighted average is based on the normative capacity utilisation factor of 35 per cent mandated by SECI. For renewable energy supplied during off-peak hours, SECI will pay a pre-specified tariff of Rs 2.88 per kWh. The tariffs are applicable for a period of 25 years.

The price discovered under this tender implies that thermal power is getting priced out in India. The most recent thermal power tenders have yielded levellised tariffs in the range of Rs 5-Rs 7 per kWh at an annual plant load factor of 85 per cent. The average price discovered under the SECI tender is also lower than that in the recent tender for stressed thermal projects released by PTC, where the winning tariff was Rs 4.24 per kWh for a three-year supply contract. In comparison, the tariff in the SECI tender is fixed for 25 years. Moreover, the peak tariff under the SECI tender is highly competitive vis-à-vis recent peak tariffs in international markets such as the US (Rs 8-Rs 9 per kWh).

For discoms, this tariff has a clear upside. They can procure renewable energy as their main power source and not have to bear the burden of the central transmission utility charges. They can also use this power to meet their renewable purchase obligations.

In this article, Renewable Watch takes a look at the key developments and trends in the energy storage space over the past one year and how these are likely to define the way forward.

Storage economics

Storage economics

Using batteries to power vehicles and store electric energy in the grid was once thought to be a completely uneconomic proposition. Today, declining battery storage costs have made this possible. Moreover, battery storage also offers advantages over existing fossil fuel generation and internal combustion technologies. As battery technology prices continue to fall, the economic benefits of energy storage applications will become evident. According to a recent industry report, the engineering, procurement and construction (EPC) cost of battery storage is expected to reduce by 15-20 per cent, from the present range of $300-$320 per kWh to $250-$270 per kWh by 2021. With falling battery prices, the peak tariffs are also anticipated to come down significantly over the next few years.

The declining cost of lithium-ion battery technology is the primary trend driving market growth for the energy storage industry this year. Since 2013, prices have dropped by nearly 73 per cent.

The downward price trajectory of lithium-ion technology continues to confound many projections that had forecast the price to plateau or even reverse. Instead, several industry experts now believe that the cost reductions will continue as lithium prices are expected to fall by a further 45 per cent by 2021. Bloomberg New Energy Finance has observed an 18 per cent reduction in prices every time the cumulative volume doubles, implying that an average battery pack could cost only $94 per kWh by 2024 and $62 per kWh by 2030.

Policy push

Policy push

Not only is the industry working hard to make energy storage a viable proposition, the government too is doing its bit by creating awareness about the technology. In the past two years, the central and state agencies have come up with several initiatives to encourage the adoption of energy storage systems. Some of the key initiatives are highlighted below:

- In January 2020, the Ministry of New and Renewable Energy (MNRE) released a draft policy for the supply of round-the-clock (RTC) power to discoms, which would be a mix of renewable energy and electricity generated by coal-based plants. According to the draft policy, a generator has to supply power such that at least 51 per cent of the annual energy supplied comprises renewable energy.

- In April 2019, the MNRE issued draft guidelines for storage battery testing in test labs under the Implementation of Quality Control Order on Solar PV Systems, Devices and Components Goods 2017. These guidelines are yet to be finalised.

- In March 2019, the cabinet approved the National Mission of Transformative Mobility and Battery Storage, which included phased manufacturing programmes, valid till 2024, to support e-mobility and battery storage.

- In the Union Budget 2019, the government reduced the customs duty on Cobalt matter (a key ingredient in advanced lithium-ion batteries) from 5 per cent to 2.5 per cent.

While the central government has been taking initiatives to promote storage technologies, the state governments are yet to come up with storage-specific policies for the sector. Andhra Pradesh and Madhya Pradesh are the only states that have invited expressions of interest for the setting up of battery manufacturing plants and installation of energy storage facilities.

Project pipeline

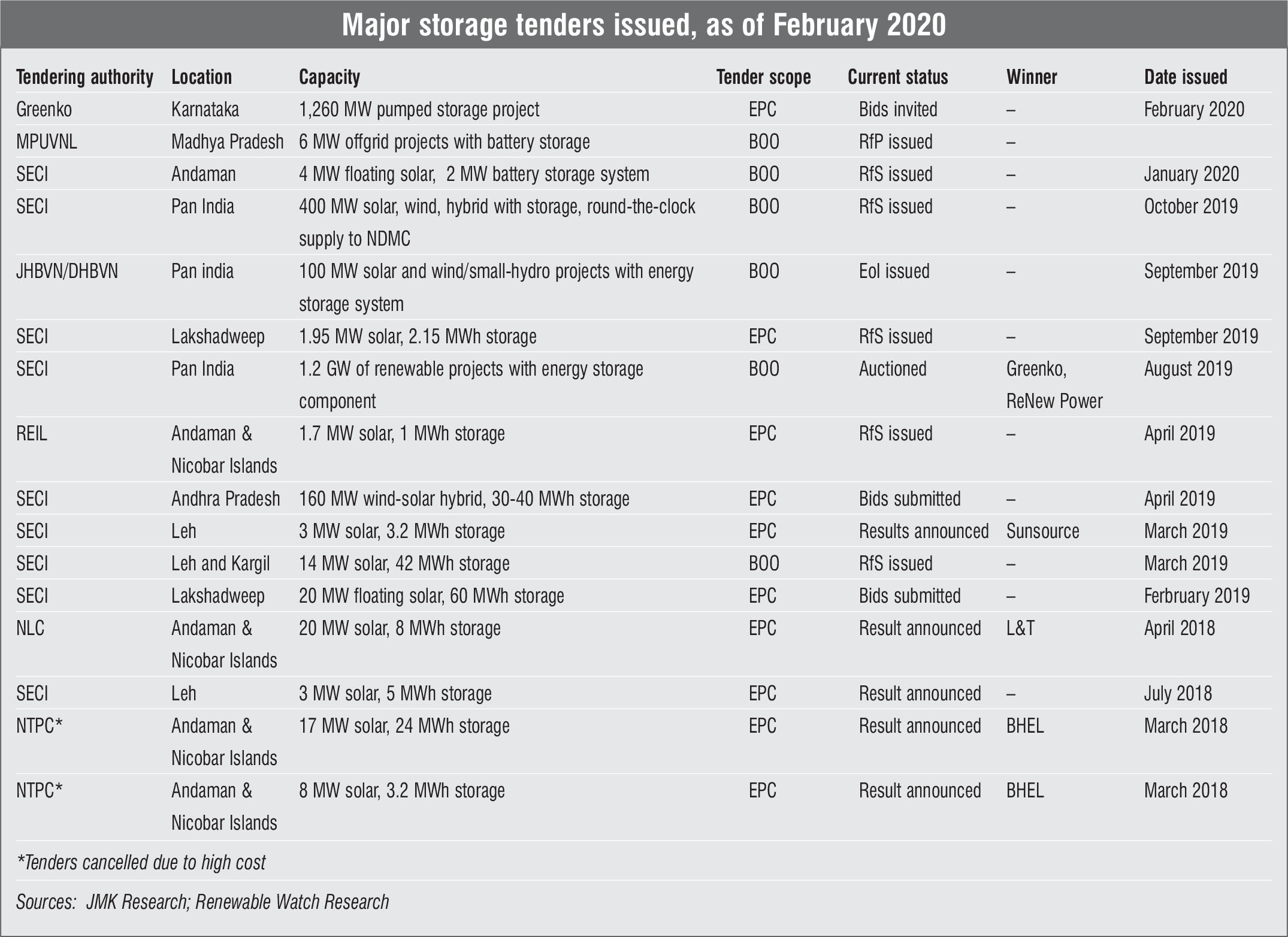

Apart from various policy measures, there has been an increase in storage tenders released by SECI, NTPC, Rajasthan Electronics & Instruments Limited, NLC, Uttar Haryana Bijli Vitran Nigam and Dakshin Haryana Bijli Vitran Nigam during 2019. However, the design of many of these tenders is making project implementation unsustainable. In most of these tenders, the storage capacity is so high that it leads to infeasible solar+storage tariffs and eventually, to the cancellation of many tenders. It is hoped that as the market matures over time, these operational and execution challenges will get addressed

Meanwhile, India’s first and biggest battery storage system of 10 MW was commissioned at Tata Power Delhi Distribution Limited’s (TPDDL) Rohini substation in Delhi in 2019. This project was undertaken by AES in partnership with Mitsubishi Corporation for about $9 million. Other large storage-based projects are expected to come up under the SECI tender that concluded recently. The tender has given a great start to the energy storage segment in 2020.

The way forward

The way forward

The Indian electricity sector is expected to witness a major transformation over the next decade with respect to demand growth, energy mix and market operations. As per Central Electricity Authority (CEA) estimates, by 2029-30, the share of renewable energy generation is likely to increase from 18 per cent to 44 per cent while that of thermal will reduce from 78 per cent to 52 per cent. The projected installed capacity in 2029-30 is around 832 GW and will comprise 291 GW of thermal, 17 GW of nuclear, and 523 GW of renewable energy (including 73 GW of hydropower). This shift will be driven by the falling costs of solar panels and battery storage systems, which will play a key role in addressing the intermittency issue of renewables as well as load balancing.

Renewables plus storage is anticipated to become a viable solution for managing peak loads in the next 12-18 months. For commercial and industrial (C&I) customers that wish to integrate rooftop solar, solar plus storage could provide an economical option in states with higher tariffs for C&I customers. This can fuel exponential growth in storage systems.

Overall, energy storage systems will prove to be valuable assets. They will help create ancillary service opportunities for improving grid reliability. Moreover, with the enforcement of grid discipline and penalties for deviations, energy storage will facilitate grid integration by dealing with intermittencies. Backed by policy support and effective implementation by government agencies, renewable energy and storage hybrid projects will drive growth during the next decade.

By Dolly Khattar