Growth in the small-hydro power (SHP) segment has remained sluggish year after year. The industry is largely underdeveloped with an installed base of only 4,671.5 MW as of December 2019, as against an estimated potential of 20,000 MW across 6,474 sites. A total of 8,236 MUs of electricity was generated by the SHP segment in 2018-19 as compared to 7,314 MUs in 2017-18.

The main advantage of SHP plants is that they can supply electricity in stand-alone mode to remote areas with restricted grid access. Commercial SHP installations sell electricity to power distribution or trading companies or to industries. They are grid connected and have a high plant load factor (PLF). SHPs are characterised by their non-consumptive use of water, low capital investment, short gestation period ranging from 6 to 24 months, low operation costs, scope for unmanned power stations. Besides, they act as catalysts for socio-economic development in far-flung areas. SHPs are largely used to power mini-grids in these areas. Most village-scale mini-grids developed in Asia are based on small hydro, particularly those in China, Nepal, India, Vietnam and Sri Lanka. SHPs also power small industries that provide substantial local income and jobs.

Current status

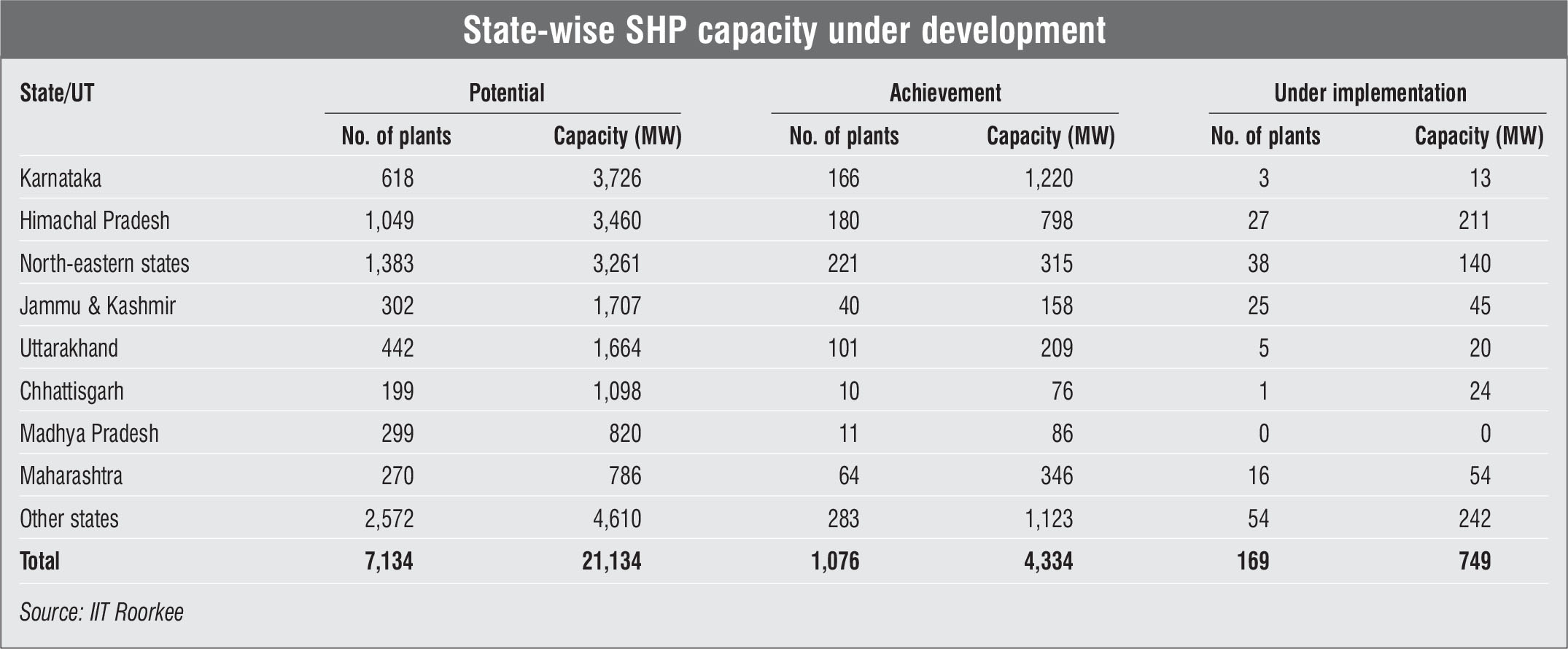

SHP development in India is focused on few states. These include Karnataka, Himachal Pradesh, Uttarakhand, Chhattisgarh, Madhya Pradesh, Maharashtra, the north-eastern states, and the union territories (UTs) of Jammu & Kashmir, and Ladakh. Of these, Karnataka has the largest installed small-hydro capacity of 1,220 MW across 166 plants. The state also has the highest SHP potential of at around 3,729 MW. Apart from this, three plants aggregating 13 MW are currently under implementation.

Himachal Pradesh has the second largest potential of 3.4 GW in the SHP segment. However, the installed capacity is relatively lower than Karnataka vs at just about 800 MW. Apart from this, around 211 MW of capacity across 27 SHP plants is in the pipeline. The north-eastern region has an SHP potential of over 3 GW, but the installed capacity is only about 10 per cent, or 315 MW. Another 140 MW is at various stages of development.

Upcoming capacity

Arunachal Pradesh has a significantly under-developed SHP potential. There are 15 projects aggregating 821.9 MW that have been proposed in the state. The units of these projects range from as small as 700 kW to as high as 37.5 MW. The tariffs proposed for these projects fall between Rs 2.82 per kWh for the Divri plant in West Kameng district and Rs 6.12 per kWh for the Pachuk I plant in East Kameng district. The median of the proposed tariffs is Rs 3.78 per kWh. The median tariff indicates the increasing competitiveness of SHP projects in remote states such as Arunachal Pradesh. Meanwhile, Uttarakhand has proposed the development of 77 projects with a total capacity of 38 MW. Most of these projects are in the micro-to-mini hydro power category with an average proposed capacity of 250 kW. Bihar has also started developing its SHP potential. It has 24 proposed projects with a total capacity of 63.6 MW.

KREDL experience

Karnataka is the only state in India with almost equal conventional and renewable energy capacities. Of the 29.9 GW of total installed capacity in the state, 15.1 GW or 50.45 per cent is in the conventional segment and 14.8 GW or 49.5 per cent is in the renewable and unconventional power segment. The SHP segment contributes 903 MW or 3 per cent to the overall installed capacity of Karnataka, as of December 2019. The prevailing SHP tariff set by the Karnataka Electricity Regulatory Commission is Rs 3.95 per kWh.

Karnataka has an SHP potential of around 3,000 MW. In addition, about 258 plants with a total capacity of 1,342 MW are in the pipeline. Of these, plants aggregating around 1,000 MW of capacity are stalled due to environmental concerns in the Western Ghats and the lack of forest clearances. Further, about 764 MW of installed capacity has been cancelled due to delays in obtaining clearances by developers. Karnataka Renewable Energy Development Limited (KREDL) has set a target of 17 MW for 2019-20.

For KREDL, the primary challenge in the development of the state’s SHP potential is the fact that most of it lies in the Western Ghats region. Environmental concerns and the impending legal suits have slowed down annual capacity addition in the region. For the rest of the state, the implementation of projects is getting delayed due to lengthy procedures in obtaining clearances from the irrigation and forest departments.

Key challenges

Key challenges

The SHP segment faces significant challenges in the hydrology, geology, construction, performance, power evacuation and financing aspects. From the technological perspective, the absence of detailed feasibility reports impacts stakeholders’ investment decisions. Meanwhile, the development of the irrigation and rural industrial segments and the decrease in the PLF of SHPs remain key issues. Since most SHPs are located in remote areas, providing transmission connectivity is a challenge, which can delay the commissioning of the plant.

There are considerable institutional challenges plaguing the segment as well. The lack of hydrological data for sites and the unavailability of other basic data prevents developers from choosing the optimum capacity and design of plants. At the same time, the shortage of skilled technicians and the lack of specific guidance for project development at the site result in cost and time delays, which lead to higher tariffs.

Financing has remained a critical challenge for the SHP segment, especially with the increasing solar and wind power development. Long gestation periods and higher costs associated with SHPs lead to higher tariffs and considerable offtaker risk. Therefore, raising long-term finance for these projects becomes difficult. Moreover, since the biggest offtakers, discoms, are struggling with their own finances, untimely payments create a cash flow issue, thus hampering plant operations. On the regulatory front, not much has happened over the years. SHP has been put on the back burner as the solar and wind power segments have become more attractive.

The way forward

The outlook for the SHP segment looks uncertain owing to policy ambiguity at the central level and weak investor sentiment. The industry remains under-developed with a low installed capacity. The sector has set a target of 5,000 MW to be achieved by 2022. Considering that only 107 MW was added in 2018-19 and the segment continues to add capacity at the same pace, it is expected to miss the target.

However, policy changes, like those made by the Himachal Pradesh government to defer free power provision for 12 years, are a beacon of hope. Going forward, other states/UTs with large hydropower potential such as Jammu & Kashmir, Uttarakhand and Arunachal Pradesh should come up with similar investor-friendly measures. To receive the social and economic gains that SHP projects offer, government agencies need to provide financial and technical support to scale up development in the SHP segment. n

Based on presentations by Srinivas Appa, General Manager, KREDL, and Mukesh Kumar Singhal, Professor, Alternate Hydro Energy Centre, IIT Roorkee, at a Renewable Watch conference on “Hydro Power in India”