")

Europe achieved a significant milestone of 1 million electric vehicles (EVs) in June 2018. This can be attributed to a 42 per cent growth in EV sales, both battery EVs and plug-in hybrids, during the first half of 2018. Europe’s accomplishment came a year after China reached the 1 million EV mark in 2017 while the US is yet to achieve the milestone.

In Europe, five countries – Norway, Germany, France, the Netherlands and the UK – account for the majority of the EV market. Their governments have made significant efforts to promote EV uptake in order to meet their targets for CO2 emission reduction in the transport sector. To this end, several countries offer incentives for EV deployment including purchase subsidies, registration tax benefits, ownership tax benefits and other financial benefits. The provision of affordable and accessible charging infrastructure, also known as EV supply equipment (EVSE), is critical for the growth of the EV market. Several companies including automobile manufacturers, distribution system operators (DSOs), energy utilities, charging point operators (responsible for the supply, installation and maintenance of charging points) and e-mobility service providers (eMSPs)), are investing in EVSE to support Europe’s transition to e-mobility.

To comply with the European Union (EU) alternative fuels infrastructure directive (AFI) issued in 2014, the European Commission (EC) has directed EU countries to set EVSE deployment targets for 2020 and 2025. This includes a target for establishing a publicly accessible EVSE outlet for every 10 cars by 2020. The EC guidelines also recommend the installation of one fast charging station every 60 km on the TEN-T Core Network (the total network length is 34,400 km) by 2025. Another development at the EU level that is expected to boost EV and EVSE uptake is the European Parliament’s approval of a revised directive on energy performance buildings. It promotes pre-wiring for charging points in buildings and mandates countries to make legal provisions for a minimum number of charging points in non-residential buildings from January 1, 2025.

E-mobility and EV uptake

Most EU countries are focusing on e-mobility for future passenger cars while only few countries such as Italy, Hungary and Czech Republic are prioritising natural gas as an alternative fuel for the transport sector. Europe is expected to witness successive waves of EV deployment according to a report, “Roll-out of public EV charging infrastructure in the EU: Is the chicken and egg dilemma resolved?”, published by the European Federation of Transport and Environment (T&E) in September 2018. The report categorises countries into frontrunners, followers and slow starters based on their EV uptake. The frontrunners include 11 countries, Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Luxembourg, Netherlands, Sweden and the UK. Italy, Portugal and Spain fall in the category of followers, while EU13 (Bulgaria, Croatia, Cyprus, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Romania, Slovakia and Slovenia) and Greece are the slow starters.

In 2017, 91 per cent of EV sales in Europe (about 217,500 EVs) were in the frontrunners group, 8 per cent in the followers group and 2 per cent in the slow starters group. The frontrunners group is expected to sell 5-7 per cent EVs (1 million annual sales by early 2020s) to comply with the CO2 emission regulations for new cars. The EC is working on its legislative proposal (presented in November 2017) for setting new CO2 standards for cars and vans in Europe for the period after 2020. This combines CO2 targets for 2025 (15 per cent reduction from the 2021 level) and 2030 (30 per cent reduction) for zero- and low-emission vehicles with a technology-neutral incentive mechanism.

Targets for EV charging infrastructure

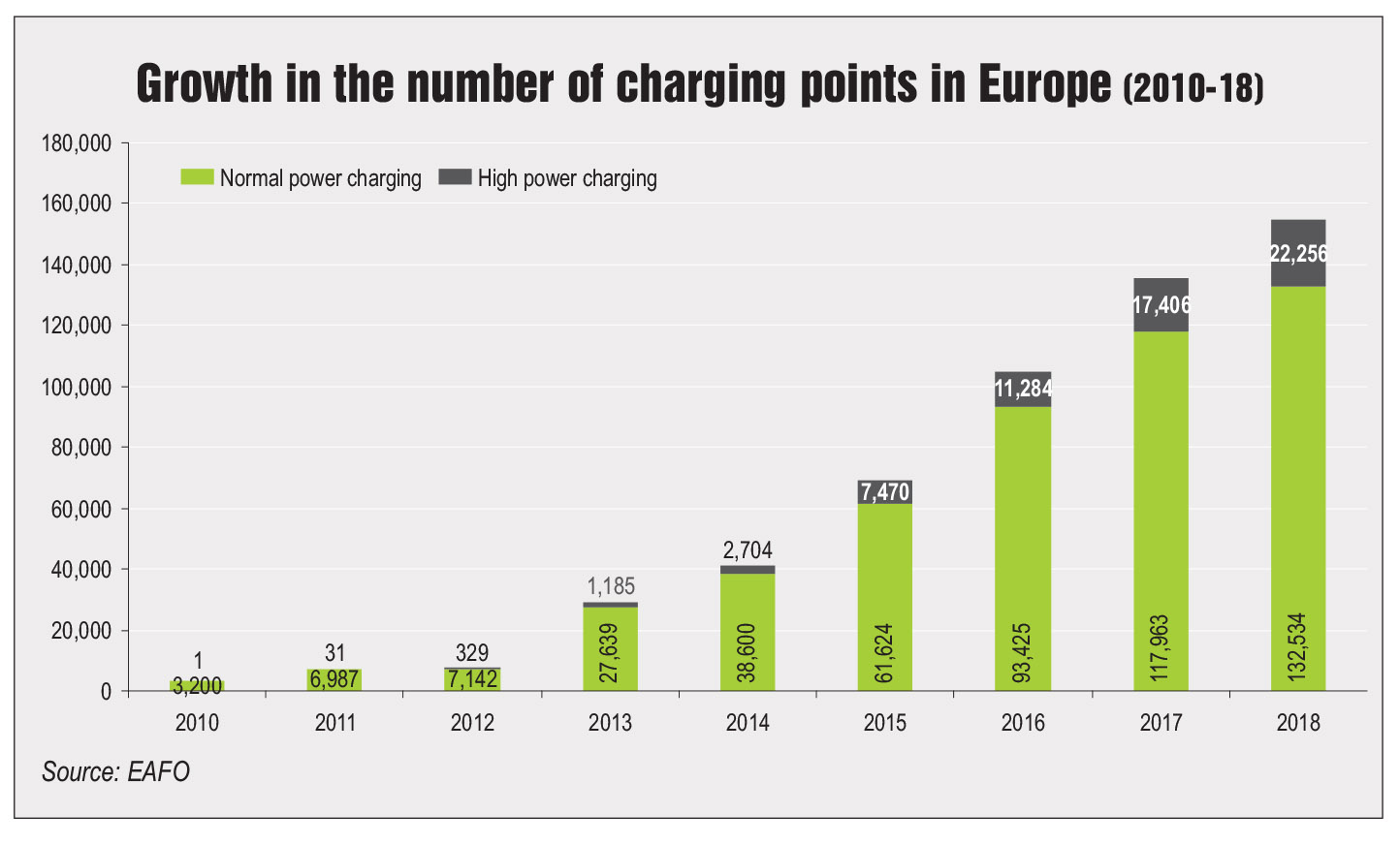

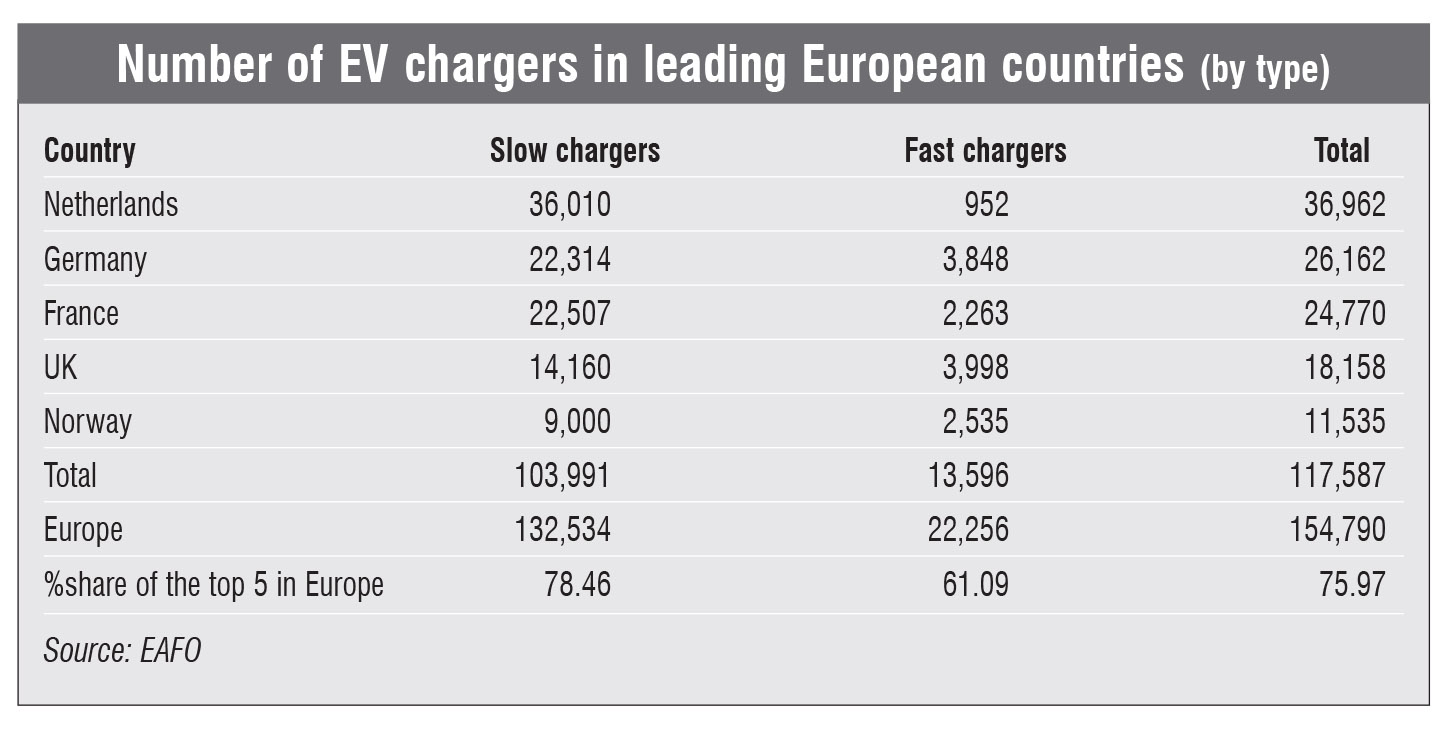

There are 154,790 publicly accessible charging points across 33 European countries, as per the European Alternative Fuels Observatory (EAFO) data, as accessed on November 2, 2018. Of these, 86 per cent are slow, or normal power chargers of less than 22 kW while fast chargers of more than 22 kW account for the rest. EV manufacturers in Europe use fast charging systems of various standards including CHAdeMO, combined charging system (CCS), Type 2AC, and Tesla Superchargers. There are over 5,000 CCS chargers across 2,550 public fast charging stations on Europe’s main roads. These stations (with an average of two CCS chargers) are placed every 60 km on an average on EU motorways covering 76,500 km.

The top five EV countries account for over 78 per cent of the slow chargers and 61 per cent of the fast chargers in Europe. According to the T&E report, western and northern Europe are ahead of southern, central and eastern Europe in charger deployment. In western and northern Europe, the public chargers and EV ratio is expected to reach the recommended 10:1 ratio with the growth in both vehicle and charger numbers by 2020. The EV market in southern, central and eastern Europe is 5-10 years behind the frontrunners. E-mobility will spread to these regions as EV technology becomes more affordable.

To meet the AFI directive objective of 10:1 EV to public charging points ratio by 2020, about 220,000 chargers are expected to be installed. These include 1,000 ultra-fast charging points (150-350 kW) along the European motorway network. This infrastructure will allow users to charge for up to 400 km in only 15 minutes. Further, 50 kW fast chargers will complement the existing fast charging points, which will almost double by 2020. This implies that there will be one recharging point every 34 km along the strategic TEN-T Core Network.

Slow chargers, fast chargers and grid impact

Slow chargers, fast chargers and grid impact

Slow public chargers are commonly found in urban areas, where they can be combined with private off-street parking points. The number of slow public chargers varies across cities depending on the availability of off-street parking and the number of cars, among other things. The Netherlands has the highest number of slow chargers at 36,010 followed by France and Germany. In most countries in the EU, the number of EVs per public slow charger is significantly below 10 except in Belgium and Sweden, which have around 20 EVs per charger. While fast chargers currently form a small proportion of total EVSE in Europe, the continent is emerging as one of the most popular destinations for the deployment of direct current fast charging stations.

Some of the concerns pertaining to EV penetration include overloading of the existing infrastructure, which may adversely impact the grid, the health of the existing distribution transformers and the quality of the power supply to consumers. Therefore, adequate planning and infrastructure development is required. Studies indicate that a network of fast chargers may cost less than slow charger if grid reinforcement is not required. To mitigate the impact of fast chargers on the grid, they may be combined with energy storage systems. These storage devices can be used during peak demand hours with applicable time-of-use rates. Also, vehicle-to-grid (V2G) technologies, currently at the testing/pilot stage, will help EV owners feed the energy back into the grid and help energy providers meet demand during peak periods. There are at least 18 V2G pilots (ongoing and completed) across 10 European countries including Germany, the Netherlands, the UK, Denmark and Norway.

EVSE investments

Overall, the cumulative investment in public charging is estimated to reach Euro 12 billion by 2030, which is a small proportion of the Euro 100 billion annually invested by the EU in transport infrastructure as per the T&E report. The spending on private charging by 2030 is expected to reach Euro 20 billion.

So far, both the public and private sectors have invested in EV charging infrastructure. The T&E study estimates that the initial need for government subsidy and investment will gradually reduce during 2020-25 in the frontrunners group. According to another study by Fuelling Europe’s Future II, the investment in EV charging infrastructure will be entirely private in 2025. Chargers will be installed at parking sites, retail stores and shopping malls to attract higher rents and more customers. Fast chargers will be funded by private players as the increasing number of EVs on the road will make it a viable business model. Several private players have committed significant investments (in many cases without any involvement of public money) in ENVSE. In Belgium, Allego, a charge point operator, plans to install 2,500 public charging stations by 2020. Meanwhile, the joint venture (JV) of Nuon-Heijmans is installing 2,480 charging points in Noord-Brabant and Limburg in south Netherlands without any subsidy. The JV has entered into a 10-year contract with the two provinces. While Heijmans will install and maintain the charging points, Nuon will provide financing and related energy services.

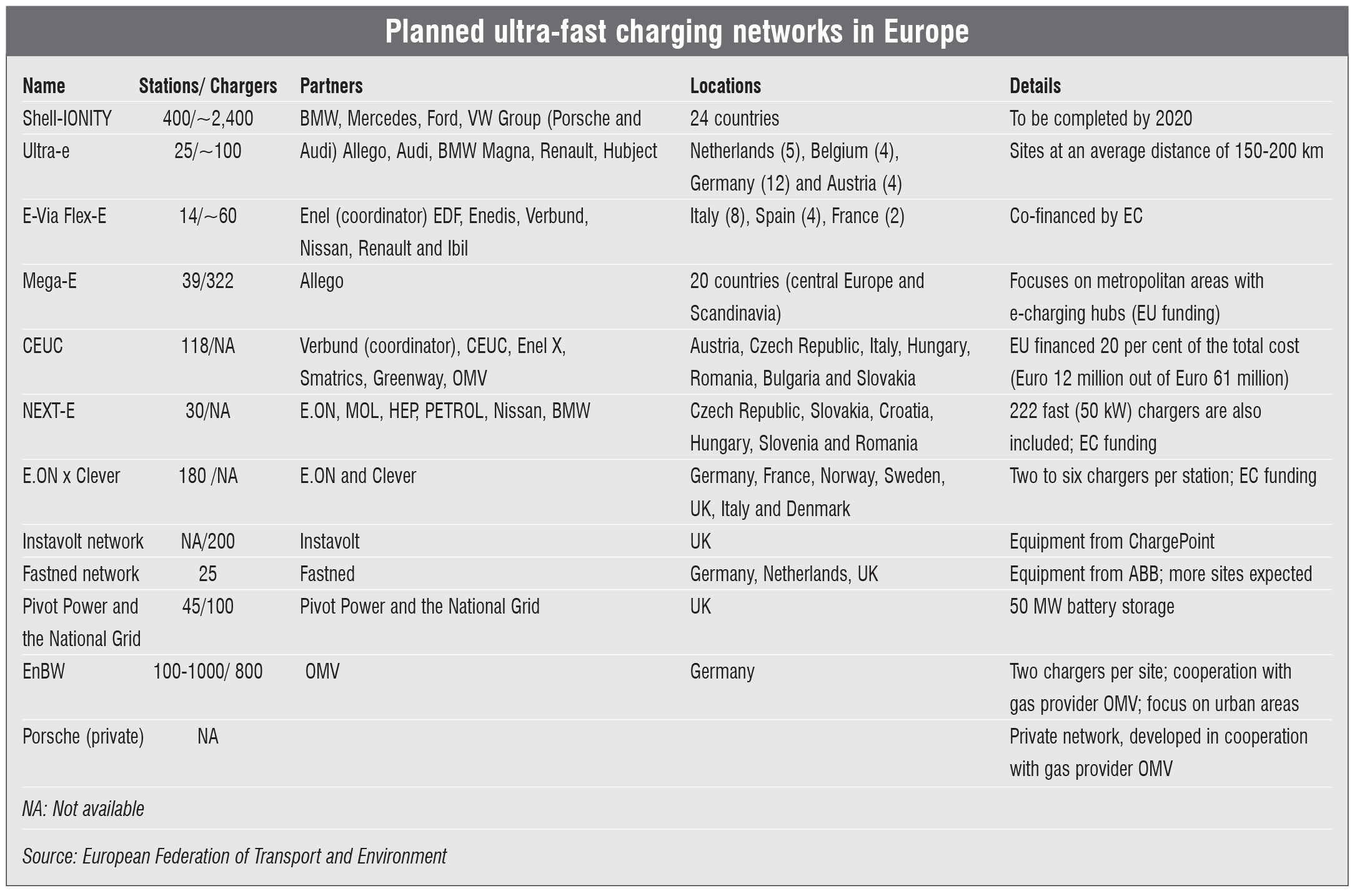

Ultra-fast charging networks

Ultra-fast charging networks

European energy and grid utilities are actively participating in the installation of public fast and ultra-fast charging networks. For instance, the National Grid in the UK is working with local Pivot Power LLP to develop one of the world’s largest networks of rapid EV charging stations. The GBP1.6 billion project will entail the installation of 2,250 MW of batteries at 45 electric substations across the country to provide charging at competitive rates. The network will initially support 100 fast chargers of 150 kW each, and later accommodate 350 kW ultra-fast chargers. The project will give the system operator more choice and flexibility for managing the demand on the grid while facilitating large-scale EV charging. In May 2018, Pivot Power announced its plans to make batteries operational at 10 sites over the next 18 months.

Germany-based utility enBW has collaborated with gas provider OMV to install and maintain more than 1,000 ultra-fast charging sites by 2020. The chargers will not be restricted to motorways, but will be set up in urban centres as well. Initially, enBW plans to set up 100 charging stations across Bavaria and Baden-Württemberg.

Austria-based energy company Verbund is leading the Central European Ultra Charing (CEUC) project, which aims to deploy 118 high power chargers across seven EU countries at an investment of Euro 61 million. Besides, there are several other ultra-fast charging network projects coming up across Europe.

The way forward

The way forward

Europe is rapidly developing a significant EV charging network to make 100 per cent electricity-based long distance travel possible. According to the T&E report, the biggest constraint in the shift to e-mobility is the limited availability of EVs and minimal EV marketing rather than the lack of infrastructure. There are only about 30 battery and fuel cell electric models available for sale as compared to the 370 conventional fuel based models. In this context, the proposed car CO2 regulations will drive the transition to zero emission solutions. To ensure a comprehensive EU-wide EVSE roll-out, T&E has made several recommendations for policymakers. This includes targeted EU investment in infrastructure, the revision of the AFI directive, the creation of an EU fund dedicated to urban recharging, grid upgradation, building recharging, creation of tailored loan and grant schemes for small companies, and the introduction of open standards for e-mobility services. It is exciting times ahead for the EV market as EU countries gear up for a transformation in the mobility landscape.