The rooftop solar segment has been slow to take off. The underlying reasons have been the government’s primary focus on utility-scale solar projects and the perception that rooftop solar is slow to scale up. With a modest cumulative capacity of 3.4 GW, the share of rooftop solar in the country’s total solar installed capacity is fairly low at 13 per cent.

The story so far…

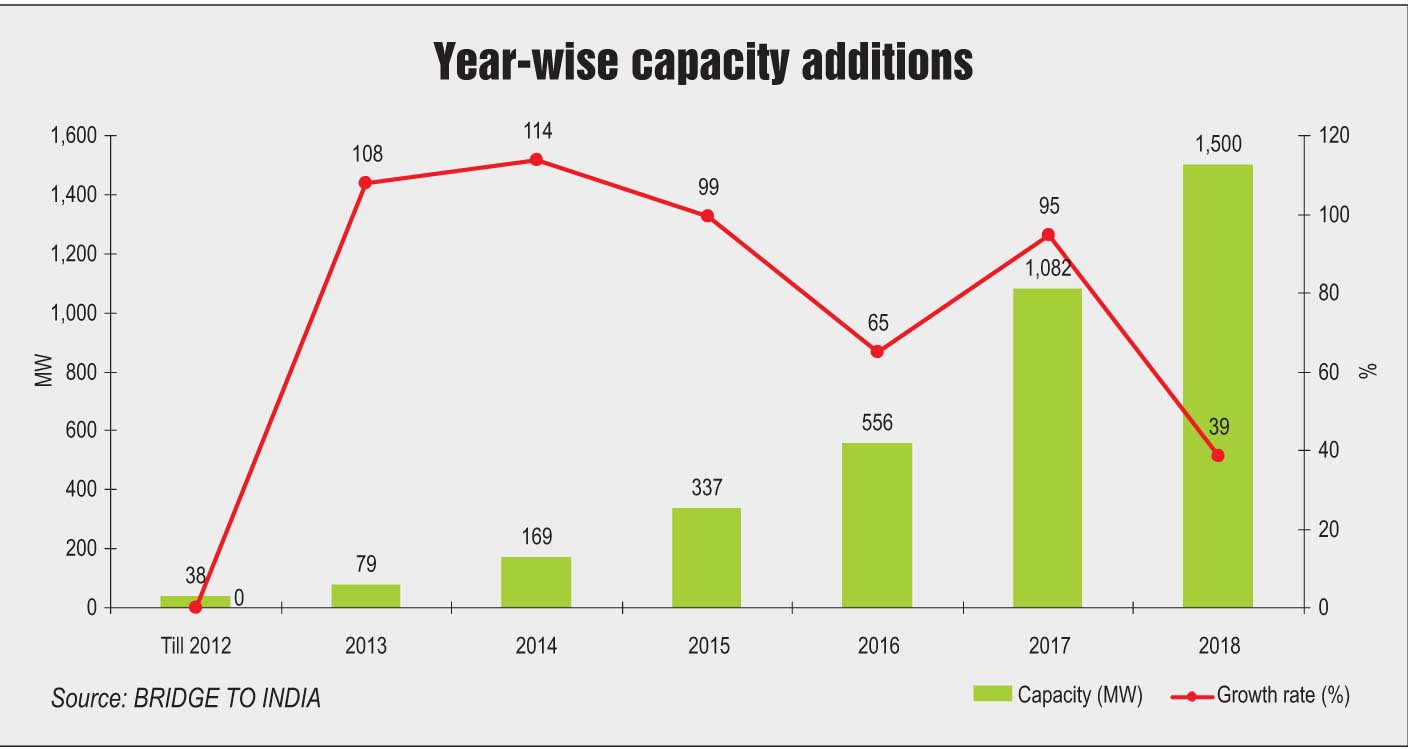

Over the past five years, the rooftop solar segment has grown at a compound annual growth rate of 85 per cent. Last year, the country added 1.5 GW of rooftop solar capacity, which is an achievement in a year plagued by uncertainties surrounding safeguard duty, and goods and services tax.

Of the 3.4 GW cumulative rooftop capacity, the commercial and industrial (C&I) category accounts for 2,376 MW, the residential category for 521 MW and the public category for 502 MW.

- C&I category: This is the most active category, accounting for over 75 per cent of the total installed capacity. C&I customers have the incentive of shifting to a rooftop solar system as they pay the highest grid tariff and also have abundant rooftop space. They also benefit from financial savings accruing from the installation. Their access to debt financing, use of the operating expenditure (opex) business model and familiarisation with the technology have led to greater uptake of rooftop solar systems.

- Residential category: The high upfront cost in the capital expenditure (capex) model and the availability of competitively priced grid electricity in urban areas have made subsidies less relevant.

- Public category: This category has a strong growth potential. However, despite the government’s support in the form of capital subsidies, the execution of projects remains patchy and the progress on tenders slow. Further, competitive auctions and a lack of standards could lead to a compromise in project quality.

States with high power consumption and a significant C&I base are ahead in the rooftop solar race. The top three states include Maharashtra, Tamil Nadu and Karnataka.

Rooftop solar market

Rooftop solar market

The rooftop solar market for capex players is fairly crowded given that there are few entry barriers. Tata Power Solar is the largest player in the capex space, though it accounts for just 5 per cent of the total annual market. Mahindra Susten and Bosch are other major players in this space. Meanwhile, start-ups such as Sunsure and Fourth Partner have entered the market and are quickly carving a niche for themselves.

An interesting trend has been the growth of the opex model, particularly in the C&I space. This model now accounts for 35-40 per cent of the incremental installations every year.

Despite industry enthusiasm over this model, a key growth constraint persists. Opex players need to raise large amounts of capital to scale up their businesses while keeping the credit-worthiness of their customers in mind. Currently, the market for opex players is less concentrated. Cleantech Solar is a leading player in the opex category. Meanwhile, many large independent power producers (IPPs) and solar players are looking to venture into rooftop solar to exploit the opex model. The biggest IPP to have entered the segment is ReNew Power, which now has an active C&I rooftop business.

Next steps

The policy framework for the segment focuses on reducing the cost of financing using capital subsidies, accelerated depreciation and cheaper credit while facilitating grid-integration through net and gross meters. The policy and regulatory framework needs a rethink given that the cost of installation of a rooftop solar system is falling. The government can start by amending the Net Metering Policy and remove the caps and constraints concerning system size, contracted load and peak demand. Meanwhile, discoms see the rooftop solar segment as a business threat fearing that it would lead to them losing paying clients. This will continue to be the case if discoms provide free net meters or earn less in lieu of cross-subsidy surcharge. Therefore, the need of the hour is to create a viable business model wherein discoms can receive, say, Re 0.50 to Re 1 per unit of the wheeling and banking charges.

For companies wishing to shift their customer base from large C&I segment to small and medium enterprises (SMEs), awareness generation about business models, system configurations and other technical aspects among target customers is paramount. To instil confidence in the SME and residential segments, a programme on quality standards will be needed for making contractors and developers accountable for generating less power from the system. Further, long-term policy visibility will go a long way in helping stakeholders plan better.

If these changes are put into effect, the country would be able to build 21 GW of capacity by March 2023. That is, in the next five years, over 18 GW of capacity would be added, translating into 3.5 GW of capacity addition per year on average.

Based on a presentation by Vinay Rustagi, Managing Director, BRIDGE TO INDIA, at Renewable Watch’s conference on “Distributed Solar in India”