With the growing focus on renewable energy, the power sector across the world is currently undergoing transformation, moving from conventional to alternative sources of energy. In some countries, the annual renewable capacity addition has surpassed that of conventional energy, indicating a shift in policies and investments in favour of renewables. The global solar photovoltaic (PV) market grew considerably in 2015-16 on the back of increased investments in both developed as well as emerging economies. The annual market for new capacity was up by around 25 per cent as compared to 2014, with about 50 GW being added during the year to bring the cumulative solar PV capacity to around 227 GW. The capacity addition is estimated to have involved the installation of about 185 million solar panels. Globalisation continued in the solar PV segment even though about a third of the total capacity addition came from the top three countries – China, Japan and the US.

Renewable Watch takes a look at the global status of solar PV technology…

Current scenario

The solar PV installation market has moved away from the developing countries to emerging economies, especially in Asia and Africa, where there is still a large gap between the demand and supply of power. Solar PV has become a feasible alternative for areas without grid access. Most of these countries have planned roadmaps for the development of solar power through government programmes aimed at meeting the growing demand for power. In addition, falling tariffs and capital costs as well as increasing awareness regarding the potential of solar PV in mitigating climate change also work in favour of the segment. Notably, the developed markets in Europe saw low capacity additions during the year.

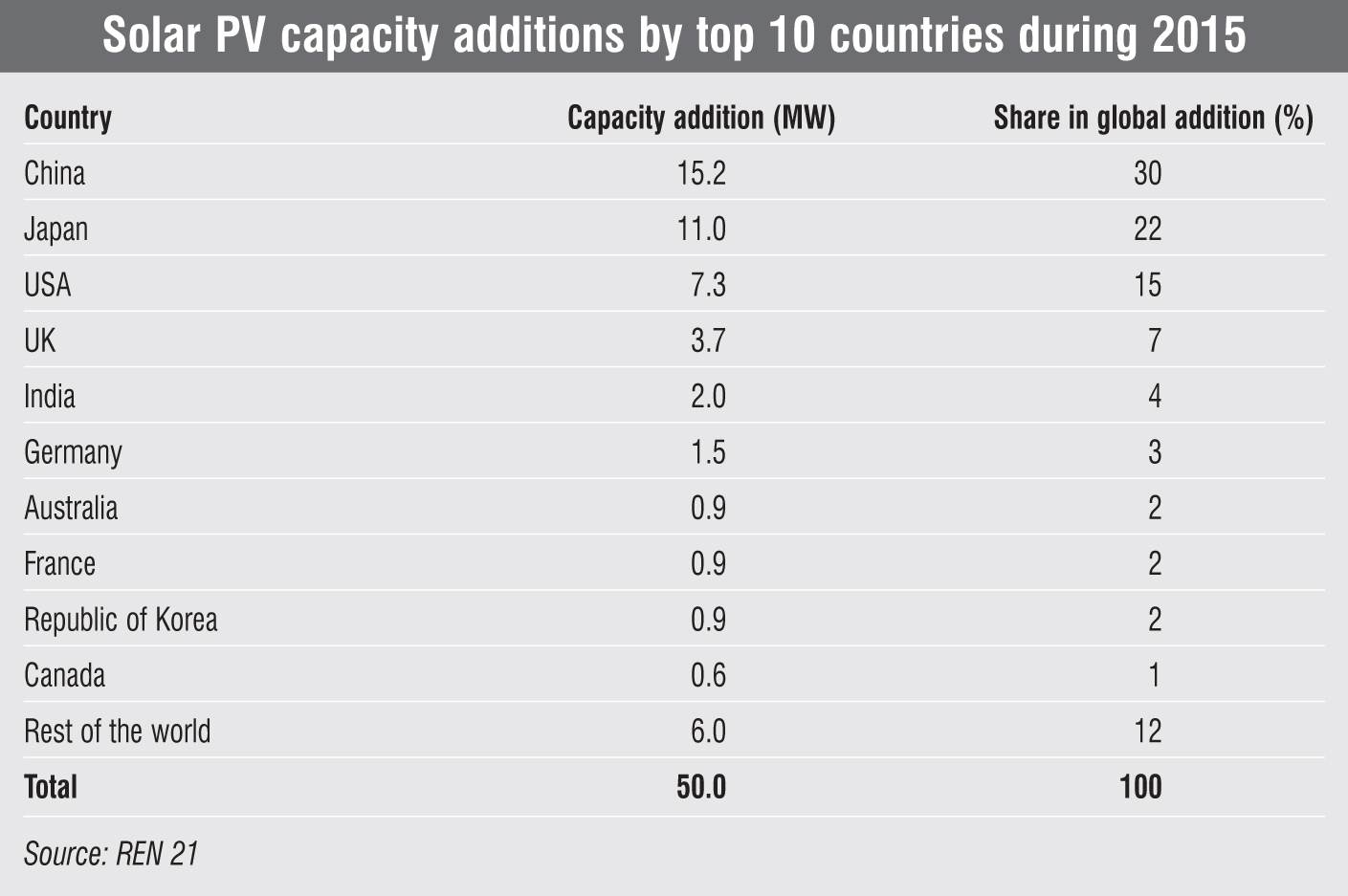

China and Japan were the top two markets, followed by the US in the third spot. Other countries in the top 10 list included India, Germany, Republic of Korea, Australia, France and Canada. Asia surpassed all other regions in terms of solar PV capacity addition for the third year consecutively. Every continent reached at least 1 GW of installed capacity as of end-2015 and around 22 countries surpassed 1 GW of solar PV installations.

China added 15.2 GW to bring its total cumulative solar PV capacity to 44 GW, surpassing Germany to become the largest solar PV market that comprises about 19 per cent of the world’s total installed capacity. Among all provinces, Xinjiang, Inner Mongolia and Jiangsu were the top performers of the year with 2.1 GW, 1.9 GW and 1.7 GW of capacity addition respectively. Large-scale installations accounted for 86 per cent of the country’s total installed capacity, while rooftop systems and small installations accounted for the remaining share.

In Japan, nearly 11 GW was added to the grid, bringing the total capacity to around 34.4 GW. Despite the record growth, the residential segment market remained low, with only 0.9 GW of installed capacity. Meanwhile, commercial and utility-scale projects led the growth in the segment. The problem of unavailability of land is being resolved by utilising abandoned farmland and golf courses. The share of solar PV stood at 10 per cent of Japan’s peak electricity supply and accounted for 3 per cent of the total power generation in 2015.

In the US, solar capacity additions exceeded the new natural gas capacity for the first time. After a three-year decline, the European solar market picked up with an addition of 7.5 GW of capacity, of which the UK (3.7 GW), Germany (1.5 GW) and France (0.9 GW) added nearly 75 per cent. Latin America’s cumulative capacity grew by 100 per cent with 1.1 GW added in 2015. Honduras and Chile were at the forefront with 0.4 GW of capacity addition each, while growth in Brazil and Mexico was limited due to poor economic conditions.

Rapid capacity addition in countries like India and China, and the lack of proper grid infrastructure led to roadblocks and curtailment, resulting in less-than-expected growth in solar capacity. China suffered due to poor grid availability while India witnessed project delays in many states. Given the ambitious targets of these two countries and increased technology adoption owing to its cost effectiveness, grid congestion is likely to be a key hurdle in segment growth.

Technology trends

There are two technologies in the solar PV domain, crystalline-silicon and thin-film PV modules. The solar revolution began with thin-film technology; however, over the years, crystalline-silicon (monocrystalline and polycrystalline technologies) increased its market share to become the most popular form of solar PV technology. Among these, monocrystalline has gained considerable share over polycrystalline due to its higher efficiency. The former is 2 per cent more efficient than polycrystalline and thin-film technologies, and it has a higher average power output of 4-8 per cent. Polycrystalline cells can be combined with multilayered solar cells and are beneficial for distributed solar PV systems.

The uncertainty and variability of solar energy are major challenges faced by markets across the globe. To this end, energy storage solutions, which were discontinued after the initial success of solar technology as off-grid systems gave way to grid-connected solar systems, have been brought back into the system. As the quantum of installed solar capacity grows, grid integration is becoming increasingly difficult; therefore, energy storage solutions are becoming a necessity.

A team of scientists is developing a high performance technology with two junction gallium arsenide cells, which has already achieved around 30 per cent efficiency. With the help of additional layers, researchers expect efficiencies to reach 50 per cent. Meanwhile, a group of scientists at the Los Alamos National Laboratory, New Mexico, is working on a new design involving quantum dots. These are nanometre-sized crystals that have the ability to confine energised electrons. The process, known as “multiple exciton generation”, can potentially recover about 66 per cent of light energy normally lost as heat.

Technological innovations in the solar PV segment are focused on bringing about improvements in the manufacturing process by streamlining it to lower costs by using advanced material and improving the efficiency of modules. The Perovskite technology increased its efficiency by about five times in the past six years, but is yet to see commercialisation. Passivated emitter and rear cell coating technology was introduced during the year and seems promising for increasing cell efficiency in standard production processes. Innovations have also continued in areas such as solar windows, spray-on solar and printed solar cells. German company Merck and UAE-based Emirates Insolaire have announced new building-integrated solar PV products for building facades.

Market consolidation

The solar PV industry continued to witness consolidation with some of the top manufacturers even going out of business due to huge debt. Notable among these were US-based SunEdison, which had to file for bankruptcy in April 2016; US-based Recurrent Energy, which was acquired by Canadian Solar; and Conegra, which was acquired by SunPower. Engineering, procurement and construction companies continued their vertical integration in the operations and maintenance business even as new financing options emerged in the form of solar leases, power purchase agreements and green bonds.

Future outlook

The solar PV segment is expected to grow significantly over the next few years on the back of ambitious targets set by countries like India and increased solar PV installations in the emerging markets of Africa and Asia. China is likely to continue its domination of the PV market as it raises the installation targets to increase renewable energy generation and address the country’s major pollution problem. In addition, China is likely to increase its manufacturing capacity to cater to the growing demand in the global markets, especially in Asia and Africa. Technological advancements are expected to improve efficiencies and bring in a greater degree of automation in the segment. Overall, the solar PV segment is headed towards a positive future.

Based on the Global Status Report 2016 by REN 21