The 750 MW Rewa solar tender has marked a paradigm shift in the Indian solar power market by bringing solar tariffs to Rs 3.30 per kWh, about 25 per cent lower than the previous lowest tariffs for NTPC’s Bhadla Solar Park in Rajasthan. This marks a decline of 22.3 per cent compounded annually since 2010-11, when the Central Electricity Regulatory Commission (CERC) had set the levellised tariff for solar at Rs 14.95 per kWh. Comparing the tariffs to more recent tenders exhibits a steep decline in the average rate of sale of solar power per unit, as the tariffs in 2015-16 and 2016-17 hovered around Rs 4.50-Rs 7.

Multiple factors such as the timing of the tender and ready off-takers contributed to Rewa’s success despite the challenges prevailing in the solar power segment including discom payment, land acquisition and power evacuation issues. With the recent entry of large international and domestic players in the solar space, the financial risk-taking capacity of developers has increased, leading to a rise in aggressive bidding. Another factor that worked in favour of Rewa was the sharp decline in solar module prices, which fell by about 26 per cent in 2016 alone.

However, in the aftermath of the ultra-low tariff bids, the sustainability of the segment has come onto the radar, especially in light of the recent unsuccessful tenders.

State versus centre

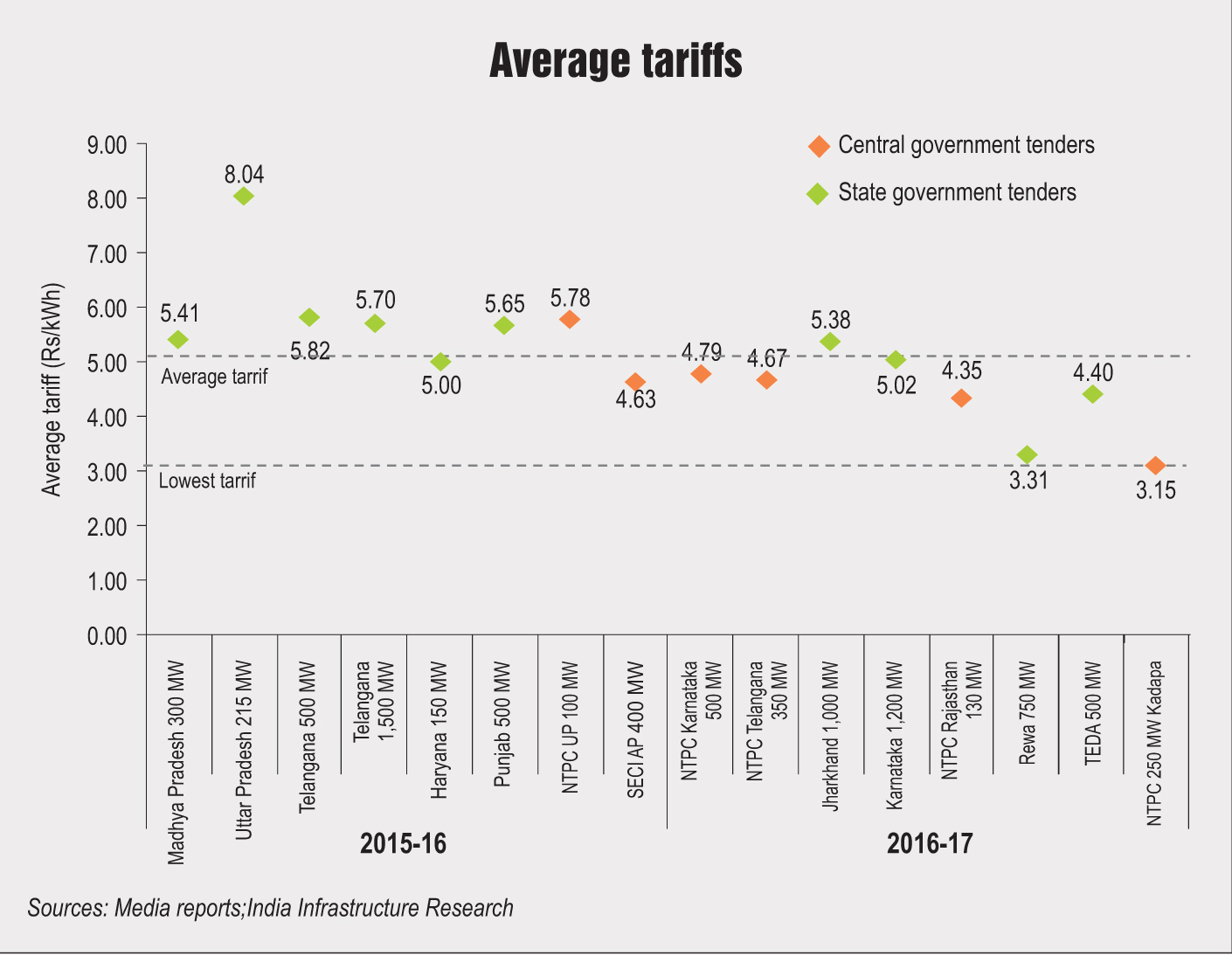

The Rewa tariff has become the new benchmark tariff against which, going forward, all tenders will be analysed. It marks a considerable deviation from other state tenders that had tariffs of around Rs 5 per kWh. The 300 MW Madhya Pradesh tender was able to fetch an average tariff of Rs 5.41 per unit, while the tariff for the 500 MW Punjab tender stood at Rs 5.65 per unit. Telangana’s two tenders of 1,500 MW and 500 MW recorded tariffs of Rs 5.82 per unit and Rs 5.70 per unit respectively, while Haryana’s state tender registered tariffs of Rs 5 per kWh.

However, the 215 MW tender in Uttar Pradesh was an outlier with tariffs recorded at Rs 8.04 per unit. The key reason for such high tariffs was the poor power infrastructure of the state. Uttar Pradesh has some of the worst performing discoms and an underequipped transmission network, and ranks low on the ease of doing business parameter. Together, these challenges increase the investor risk for solar power plants, leading to the high tariffs quoted by developers.

On comparing the results of state tenders with those of central government solar tenders by NTPC and the Solar Energy Corporation of India (SECI), the difference in tariffs is visible. The central tenders over the past two years have mostly pertained to solar parks being developed by these agencies. This has been one of the biggest factors responsible for bringing tariffs below the Rs 5 per unit mark. In fact, for solar parks or central government tenders, issues such as land availability, off-taker risk and power purchase agreement (PPA) challenges are resolved to a large extent, considerably lowering the risks associated with the project. For instance, NTPC’s 100 MW tender in Uttar Pradesh recorded tariffs of Rs 5.78 per unit in 2015-16, higher than the average for central tenders but significantly lower than the tariffs recorded in the state tender.

In 2016-17, the gap between the state and central tender tariffs seems to have narrowed. While NTPC’s 500 MW Karnataka tender fetched tariffs of Rs 4.79 per kWh, the state tender in Karnataka received average bids of Rs 5.02 per kWh. NTPC’s Telangana (350 MW) and Rajasthan (130 MW) projects saw average tariffs falling to Rs 4.67 per kWh and Rs 4.35 per kWh respectively. On the other hand, the 1,000 MW Jharkhand state tender attracted bids of Rs 5.38 per kWh. The pattern of state tenders recording higher bids than central tenders has, however, remained intact until now.

Increasingly, however, state government tenders are disrupting the pattern. With tariffs having breached the Rs 4 per kWh mark, central tenders will now face stiff competition from state agencies and solar parks to become even more competitive. The fallout of this competitiveness can be seen in the results of NTPC’s auction of 250 MW at its Kadapa ultra-mega solar park in Andhra Pradesh. Tariffs discovered in this tender have breached the Rewa benchmark to reach Rs 3.15 per unit quoted by Soliaredirect, who won the entire capacity auctioned. Ostro Energy Private Limited quoted Rs 3.16 per unit but could not win any capacity.

Post-Rewa era

The Indian solar market has come a long way from being unaffordable to nearly achieving grid parity. However, the sustainability of such ultra-low tariffs is arguable. On the one hand, there are low equipment prices that have reduced costs for developers, and on the other, tariffs are falling, adversely impacting the rate of returns for investors. According to Bridge to India, projects under recent tenders with low and ultra-low bids provide an internal rate of return (IRR) of about 14.2 per cent as against an expected benchmark of 18-20 per cent in the absence of any risk contingencies. For investors, diminishing IRRs are unfavourable and may lead to decreased investments. Technological advancements and better efficiencies are required to make solar projects more profitable.

As a result of the ultra-low tariffs, it was expected that the solar energy segment had matured. The segment, which had earlier been struggling with power evacuation challenges, seemed to have finally found its feet owing to the government’s efforts.

However, recent tenders have not delivered accordingly. The 500 MW solar tender by the Tamil Nadu Energy Development Agency (TEDA) received bids for only 50 MW and from just one developer, the state’s own discom, the Tamil Nadu Generation and Distribution Corporation (TANGEDCO). The price of Rs 4.44 per kWh quoted by TEDA had to be revised to Rs 4.40 per kWh on TANGEDCO’s request. The dismal performance of the tender can be attributed to the state’s poor transmission infrastructure that has led to the backing down of most renewable energy projects, thereby leading to idle costs for developers. Consequently, developers are wary of bidding for projects in Tamil Nadu.

In a related development, NTPC retendered the 750 MW project at its Pavagada solar park in Karnataka. The park was initially tendered in February 2017. However, due to insufficient infrastructure and lack of evacuation facilities, the central agency had to reissue the tender, the bids for which can now be submitted by May 2017. The Pavagada solar park has 750 MW of capacity to be developed under the open category and another 250 MW will be developed as per the domestic content requirement (DCR) rules. Earlier this year, SECI cancelled 150 MW of capacity at the Pavagada solar park, which was to be developed under the DCR, after the World Trade Organization ruled that DCR breached international trade rules.

Meanwhile, with the cost of solar power falling to such low levels, developers and agencies have been forced to rethink the process. SECI has also extended the deadlines for bid submissions for three of its solar parks – Charanka in Gujarat, Bhadla in Rajasthan and Kadapa in Andhra Pradesh.

Meanwhile, Jharkhand’s 1,000 MW state tender that was floated in 2016 is still open with no PPAs signed yet. With an average price of Rs 5.78, the state is facing difficulties finding an off-taker. Jharkhand’s own discom has refused to purchase power at such high rates, as compared to the low tariffs for subsequent tenders in other states. With no offtakers, the state may look at cancelling the tender altogether. Bihar, Chhattisgarh and Tamil Nadu have extended the deadlines for their 350 MW, 500 MW and 550 MW solar power projects respectively, due to falling tariffs.

Conclusion

Considering that several challenges still exist in the solar energy segment for both central and state agencies, the Rewa and 250 MW NTPC Kadapa tender results could well be outliers. Going forward, with most state and central agencies reconsidering their bidding processes, it is likely that tariff bids will not touch the sub-Rs 3 levels. However, a new normal has possibly been established with tender results averaging tariffs of around Rs 3.50-Rs 4.