In 2010, the Central Electricity Regulatory Commission had set the levellised tariff for solar projects at Rs 14.95 per kWh for 2010-11. Seven years later, such exorbitant rates sound unthinkable, with solar tariffs hitting a new low every year. The latest reverse auction for setting up solar projects at the Rewa solar park in Madhya Pradesh yielded the lowest solar tariffs seen yet in India. At Rs 3.30 per kWh, the levellised tariffs sank about 25 per cent below the previous lowest solar power price of Rs 4.34 per kWh for a 70 MW unit of NTPC’s Bhadla Solar Park allocated a year ago in Rajasthan. The tariff range hovered around Rs 4.35-Rs 5.05 per kWh in 2015-16, which was much lower than the lowest rate of Rs 6.01 per kWh quoted in 2014.

What led to such a decline in tariffs and how can it impact the growth trajectory of solar power in India are two key questions that need to be deliberated on.

Good timing and favourable factors

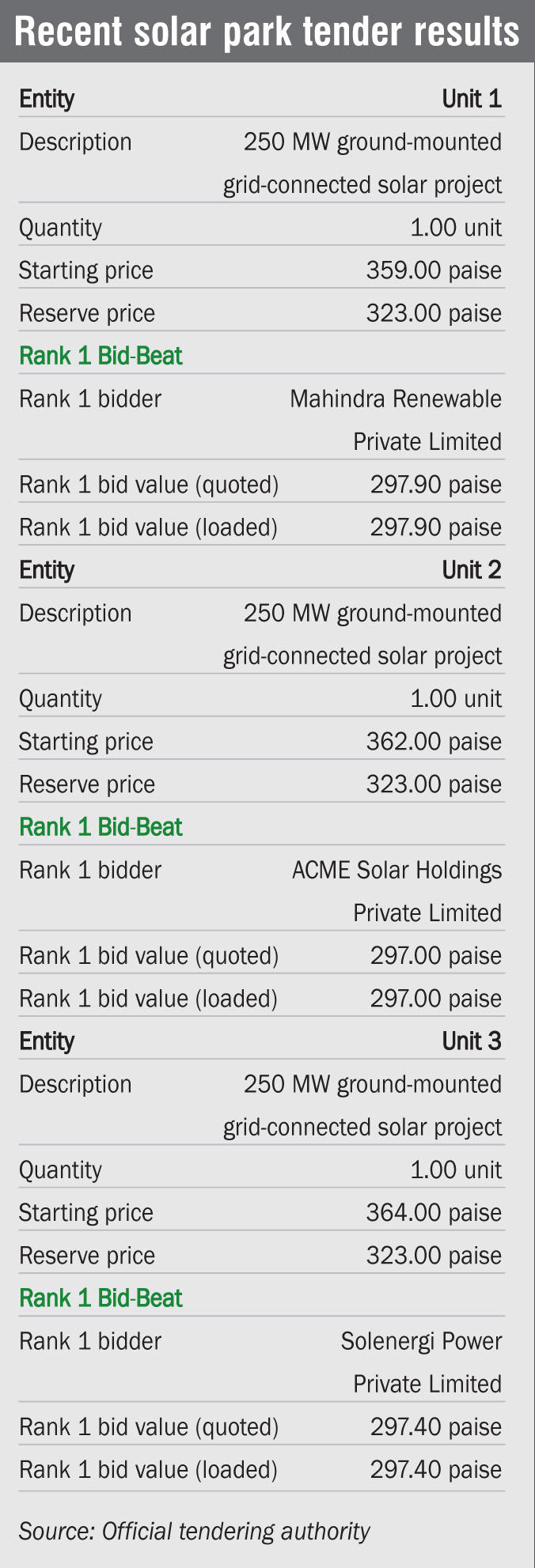

After an aggressive bidding process that lasted more than 32 hours, contracts to build and operate the 750 MW Rewa ultra mega solar power park were awarded to Mahindra Renewables, ACME Solar Holdings and Solenergi Power. The companies won contracts for 250 MW each at levellised tariffs of Rs 2.979, Rs 2.970 and Rs 2.974 per kWh respectively, after adding an annual escalation of Re 0.05 per kWh over 15 years, this translates into a levellised tariff of Rs 3.309, Rs 3.30 and Rs 3.304 per kWh respectively.

The two domestic players Mahindra and ACME, and Actis Advisors-backed Solenergi started the bidding at Rs 4.09, Rs 3.87 and Rs 3.62 respectively. These did not include the Re 0.33 per kWh that is added in the final levellised tariff. The low tariff is a joint product of a number of factors pertaining to the basic concept of a solar park, in which the risk of projects and the number of clearances required for the plant can be minimised. The size and location of projects, payment guarantee terms, deemed generation benefit, longer construction timeline, recent solar module price crash and annual tariff escalation for 15 years – all these factors led to the low winning bid.

The Rewa solar park project, built on 3,390 acres, is insulated against the most critical risks traditionally encountered by generation projects: power offtake and grid availability. The Delhi Metro Rail Corporation (DMRC) and the Madhya Pradesh Power Management Company will buy all the power generated at the park. Apart from a payment guarantee, the state government will also pay compensation to the developers if grid availability is not sufficient for power transmission from the park.

The timing for the bid was, moreover, perfect. It was conducted at a time when solar components have become cheaper. Also, the Union Budget 2017-18 has made solar-tempered glass, used in solar equipment, duty-free. It has also decreased the countervailing duty on raw materials used in solar equipment from 12.5 per cent to 6 per cent. Solar module prices have already fallen significantly in the past year. In the European Union spot market, crystalline modules in Southeast Asia were priced at around Rs 29.19 per watt power in December 2016, about 15 per cent lower than the cost in January 2016.

In a significant budget announcement, the government confirmed that it will go ahead with the second phase of its solar power park programme for promoting a capacity addition of 20,000 MW. The first scheme, Development of Solar Parks and Ultra Mega Solar Power Projects, was rolled out on December 12, 2014 with a target of 20,000 MW.

The bid timing – following the Solar Energy Corporation of India’s (SECIs) inclusion as a beneficiary in a tripartite agreement among the Government of India, the state governments and the Reserve Bank of India (RBI) – also worked well. The tripartite agreement serves as a payment security mechanism for central government undertakings whereby, in the event of a payment default by a state government undertaking including discoms, SECI can withhold central government’s financial assistance to the states. NTPC has been a beneficiary of this agreement since 2002 and past experience shows that the tripartite agreement acts as a strong deterrent to payment defaults by state government undertakings. SECI is India’s largest procurer of solar power but its financial strength has been a cause of concern despite it being wholly owned by the Government of India and a payment security fund being set up. According to BRIDGE TO INDIA’s analysis of previous bids, tariffs for SECI’s tenders are higher by up to Re 0.20–Re 0.50 per kWh as compared to NTPC’s tenders. However, its inclusion in the tripartite agreement has led rating agency ICRA to enhance SECI’s domestic credit rating from AA- to AA+, which was a big achievement for developers just before the Rewa bidding started.

The solar park, which is set to be completed by April 2018, is being supported by the International Finance Corporation (IFC), a member of the World Bank Group. IFC has extended its global expertise to structure and implement the project, and will help attract private investments of about $750 million. IFC’s work on this project will be supported by its partnership with the Department of Foreign Affairs and Trade, Government of Australia. Meanwhile, the cost of capital has recently come down due to demonetisation, which has led to banks having increased credit-creating capacity and to decreased rates of interest. To add to this, RBI has delivered a succession of rate cuts since 2015 with inflation falling by almost half since 2014, driving down the cost of finance.

Evolution of solar parks

Solar park development in the country has come a long way. The solar park concept emerged with the success of the Charanka Solar Park in Patan, Gujarat, which was followed by the Bhadla Solar Park in Rajasthan. Although these parks acted as a powerful mechanism for the rapid development of solar power projects, there were several challenges.

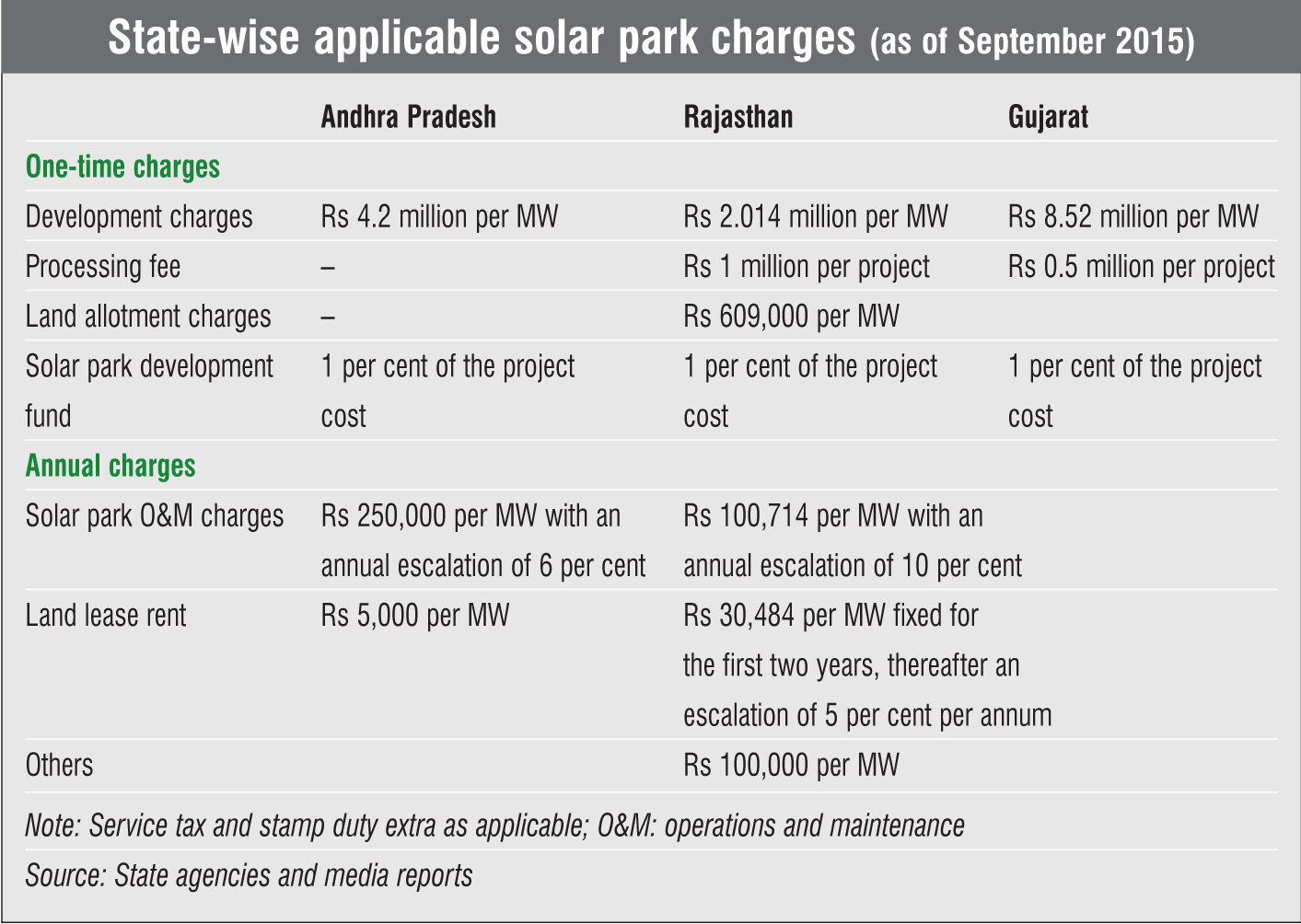

The Charanka Solar Park was the first-of-its-kind, large-scale solar park in the country, with contiguous developed land, transmission connectivity, and provision of other amenities and infrastructure. It enabled a solar power developer to get fully developed land along with transmission and other facilities and therefore set up a power project immediately. The park has a capacity of 590 MW, out of which 224 MW has already been commissioned by 20 developers. But being the first such project to be implemented in the country, it had its own share of difficulties. For instance, delays in setting up the transmission network from the park led to the delayed commissioning of projects, which in turn led to confusion related to the tariff to be paid by discoms. Project sizes were too small and led to the entry of some non-serious players, resulting in defaults. These projects eventually had to be cancelled. In the case of the Bhadla Solar Park, land acquisition was a key reason for the initial set of delays, followed by issues related to the poor power offtake track record of state utilities. Solar park charges were also high, offsetting the benefits of economies of scale offered by solar parks. These did not augur well and developers had to accordingly quote higher bids to factor in the higher risks.

Next was the solar park in Andhra Pradesh, which was an improvement in terms of land allotment charges and processing fee, but still carried high development charges. Most of the issues faced by the solar parks set up so far or those currently under implementation have been addressed by the Madhya Pradesh government while designing the Rewa solar park. The way the Rewa solar park model has been structured with cost-effective infrastructure, coupled with robust safeguards against grid interruptions and payment delays, has definitely set a benchmark for the industry.

Some industry experts believe that the low bids quoted by developers may not be feasible. However, the record low bids for solar power projects may not be a threat to the sector after all. According to a report by the Institute of Energy Economics and Financial Analysis (IEEFA), these bids are not only commercially viable, but they are replicable and sustainable as well. “This trend is not occurring in a policy vacuum. The draft National Electricity Plan, released in December 2016, calls for a fivefold expansion to 258 GW of renewable capacity by 2027, an expansion that would reduce the thermal power capacity share to 43 per cent of India’s total from 66 per cent today,” the report states. It adds that the solar auction results mean this target will be much easier and more cost-effective to achieve. The per-unit power purchase costs are tumbling, and, importantly, these prices are not only commercially viable but are likely to be beaten in 2018 and again in 2019 as total solar costs continue to decline globally at a rate of 10 per cent annually, the IEEFA states.

In a recent interview to a news daily, Manu Shrivastava, managing director, Madhya Pradesh Urja Vikas Nigam Limited, said, “These are rigorous companies and they would have thought it over in terms of risks. We have a bid security of Rs 250 million for each of the three developers. And once they sign the power purchase agreement, the performance guarantee will be Rs 750 million for each of the units.” This clause has helped keep non-serious players away from participating in the auctions.

Key lessons and conclusions

Besides setting a benchmark, the Rewa tender needs to be looked upon as an example for future learning. It will have an impact on industry expectations from upcoming solar parks being planned in the country.

It would also help open up the long-term open access market, especially for bulk public sector consumers. A unique element of this project is that about 25 per cent of the power output will be sold to DMRC using interstate open access transmission. DMRC will assume all open access-related risks and costs, expected to be about Re 0.50 per kWh. It will save more than 50 per cent on its power cost bill and draw more consumers to this market. The Madhya Pradesh government is already planning to develop more projects for supplying power to other bulk consumers across the country.

A key learning from the tariff structure set by the regulator is related to tariff escalation. According to Shrivastava, “Any discom or consumer finds it easier to pay lower prices initially. In this case, DMRC would always compare our rate to the Delhi discom rates, which increase every year. So for fair comparison, it is reasonable that our tariffs should also increase slowly rather than being a fixed number. This is important for improving the acceptability of solar power in the country.”

This auction has made solar photovoltaic the lowest-cost power source and a favourite for powering India’s future economic growth. Both consumers and independent power producers will take notice and adapt their strategies accordingly. Successful bids for new thermal power plants in India in the past two years have been in the range of Rs 3.93 -Rs 4.98 per kWh. For wind power, most states are still offering feed-in tariffs of Rs 4-Rs 6 per kWh, though the upcoming auctions may take the tariff to about Rs 4 per kWh. Gas-based power is simply not viable in India due to the high cost (over Rs 6 per kWh) and short supply of feedstock. This clearly makes solar power a key contender for future power capacity addition in the country.

By Dolly Khattar