By Nidhi Dua

Maharashtra’s electricity demand has been rising steadily in recent years, driven by growing industrial activity, urbanisation and increasing energy consumption across sectors. Electricity consumption in the state has increased from 150,764 MUs in 2022-23 to 166,224 MUs in 2025-26. According to the Economic Survey of Maharashtra 2025-26, the state has remained power-surplus from 2022-23 to 2025-26 (up to December). The average peak demand during this period stood at approximately 23,005 MW, while the average peak supply was higher at around 24,064 MW, resulting in an average surplus of about 1,059 MW.

According to the Central Electricity Authority (CEA), as of February 2026, the total installed power capacity in the state stood at 60,904.97 MW, with thermal power contributing 27,839.02 MW and nuclear 1,068.66 MW. According to data from the Ministry of New and Renewable Energy (MNRE), the state’s installed renewable energy capacity reached 31,666.75 MW as of February 2026, with 384.28 MW of small hydro, 5,873.01 MW of wind, 2,998.3 MW of biopower, 3,047 MW of large hydro and 19,364.16 MW of solar power capacity.

Maharashtra’s solar portfolio includes 12,171.3 MW of ground-mounted solar, 5,221.2 MW of rooftop solar installations (including those under the PM Surya Ghar: Muft Bijli Yojana) and 1,971.66 MW of off-grid/Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyaan (PM-KUSUM) Component B. The state’s biopower capacity is further divided into 2,907.3 MW of biomass power/bagasse cogeneration, 16.4 MW of non-bagasse biomass cogeneration, 12.59 MW of waste-to-energy (WtE) and 62.01 MW of off-grid WtE capacity.

Renewable Watch takes a look at recent developments across renewable energy segments in Maharashtra, the evolving renewable energy regulations and the outlook for the sector…

Solar momentum

Solar momentum

Maharashtra’s progress in solar energy deployment has been notable across segments, particularly rooftop solar and agricultural solar pumps. The state has witnessed strong uptake under the PM Surya Ghar scheme. As per the scheme’s website, Maharashtra has received a total of 668,089 applications as of March 2026. Of these, 466,324 installations have been completed, covering 738,519 households across the state. This translates into a conversion rate of 69.79 per cent. Maharashtra’s cumulative installed capacity under the scheme stands at 1,724.74 MW. To further support rooftop solar adoption, the state government has approved the Swayampurna Maharashtra Residential Rooftop Solar Scheme, with a total outlay of Rs 6.55 billion. The scheme provides subsidies to eligible consumer categories to support the installation of residential rooftop solar systems across the state.

Meanwhile, the state has demonstrated mixed performance under the PM-KUSUM scheme. Under Component A, although 240 MW was sanctioned, only 4 MW has been installed so far. Under Component B, which focuses on the installation of standalone solar pumps, 575,000 pumps were sanctioned, of which 502,950 have been installed as of March 2026. Under Component C (feeder-level solarisation), 775,000 pumps were sanctioned and all have been installed.

Further, the state has supported solar irrigation through its Magel Tyala Saur Krushi Pump Yojana, which focuses on the installation of off-grid solar pumps for agricultural use. In December 2025, Maharashtra achieved a significant milestone with the installation of 45,911 off-grid solar agricultural pumps within a span of just 30 days, earning recognition from the Guinness World Records. This milestone positioned Maharashtra as the fastest deploying solar agriculture state in India and second globally after China in terms of the scale and speed of solar pump deployment by a single administrative region.

Maharashtra also aims to develop large-scale solar parks, but the progress has been slow. According to a Rajya Sabha response dated February 3, 2026, four solar parks have been approved in the state, with varying levels of progress. The Dondaicha Solar Park has an approved capacity of 250 MW, of which 100 MW has been developed. The Erai Floating Solar Park (100 MW) and the Patoda Solar Park (250 MW) are also under implementation. Meanwhile, development activities are yet to commence for the Sai Guru Solar Park (500 MW).

Maharashtra also aims to develop large-scale solar parks, but the progress has been slow. According to a Rajya Sabha response dated February 3, 2026, four solar parks have been approved in the state, with varying levels of progress. The Dondaicha Solar Park has an approved capacity of 250 MW, of which 100 MW has been developed. The Erai Floating Solar Park (100 MW) and the Patoda Solar Park (250 MW) are also under implementation. Meanwhile, development activities are yet to commence for the Sai Guru Solar Park (500 MW).

Overall, some solar initiatives in Maharashtra have witnessed slower progress compared to their planned targets. For instance, the Mukhyamantri Saur Krishi Vahini Yojana 2.0, launched in May 2023, aims to supply daytime electricity to 100 per cent of agricultural pump consumers by installing 16,000 MW of solar capacity by December 2026. However, only about 2,887.8 MW has been installed so far. Similarly, the solar-based cold storage initiative, launched in December 2020, targets the establishment of 800 solar-powered cold storage units for agricultural produce, but only 22 units have been set up to date.

BESS and PSP ambitions

Maharashtra has been actively investing in both battery energy storage systems (BESSs) and pumped storage projects (PSPs). According to the CEA, the installed energy storage capacity in Maharashtra is estimated at 2,844 MW by 2034-35. Furthermore, the state has an estimated pumped storage potential of 56,355 MW. Of this, 400 MW is currently operational – the Bhira PSP (150 MW) and the Ghatgar PSP (250 MW). In addition, 2,500 MW is under construction, 6,300 MW has received approval from the CEA and is yet to be taken up for construction, while 24,800 MW is under survey and investigation.

Maharashtra has also been expanding its footprint in the BESS segment. In April 2025, Tata Power received approval from the Maharashtra Electricity Regulatory Commission to install a 100 MW BESS in Mumbai over the next two years. Later, in November 2025, Godawari New Energy announced plans to establish a 10 GWh BESS manufacturing facility in Maharashtra.

Green hydrogen drive

Maharashtra was the first state in India to approve and notify a dedicated green hydrogen policy. The state cabinet cleared the Maharashtra Green Hydrogen Policy in July 2023, with a target to achieve 500 kilotonnes per annum of green hydrogen production by 2030 and position the state as a key clean energy hub. The state’s policy focus is underpinned by a sizeable and growing industrial demand base.

Reflecting early progress under this policy framework, in July 2025, Hygenco Green Energies commissioned a green hydrogen and green oxygen production facility in Chhatrapati Sambhaji Nagar. The project will supply green hydrogen and oxygen to Sterlite Technologies Limited’s glass preform manufacturing facility.

Harnessing CBG

The compressed biogas (CBG) sector in Maharashtra is gradually expanding, although most of the registered projects are still in the early stages of development. As per the GOBARdhan portal, 262 CBG/bio-CNG plants have been registered in the state so far. Of these, 201 plants have not yet started construction, while 39 are currently under construction. Only 22 plants have been commissioned till date.

Recent developments indicate steady progress in the sector. In October 2025, a cooperative multi-feed CBG plant was inaugurated at the Maharshi Shankarrao Kolhe Sahakari Sakhar Karkhana in Kopargaon, Ahilyanagar district. Built at an investment of around Rs 550 million, the plant will produce 12 tonnes of CBG and 75 tonnes of potash granules per day using sugarcane by-products such as jaggery and molasses. Further, in December 2025, Engineers India Limited commenced site activities for its CBG plant at the MIDC Halkarni Industrial Area in Kolhapur district. The project has a production capacity of 5 tonnes per day of CBG.

State of the sector

State of the sector

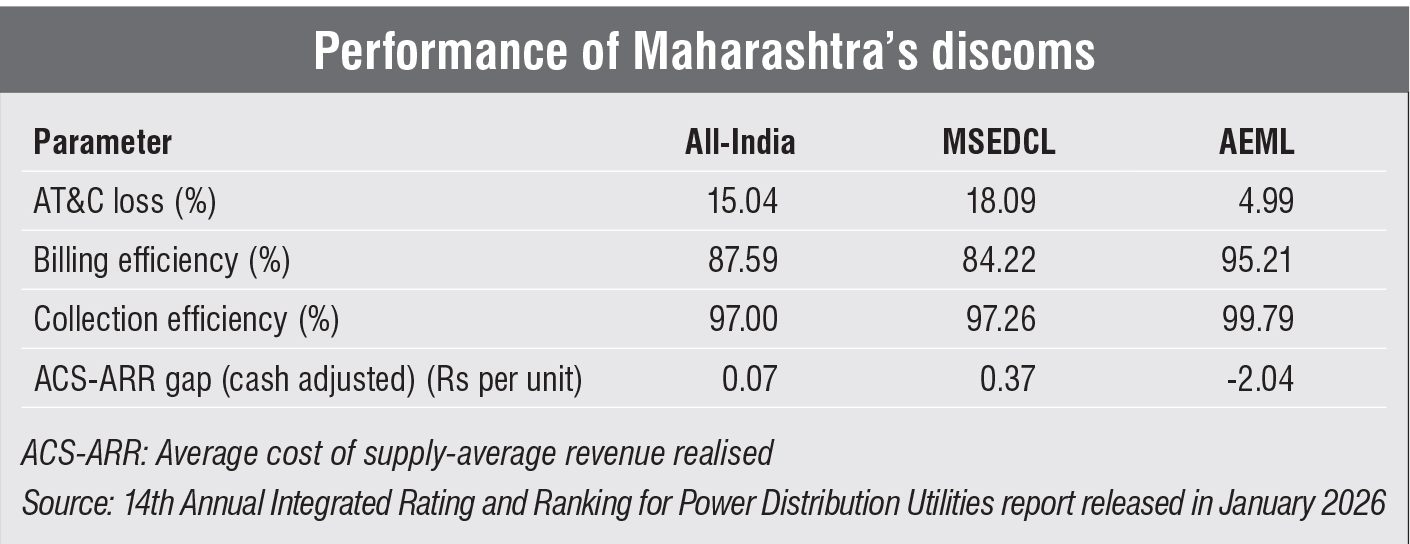

As the share of renewable energy in India’s power mix continues to increase, the operational and financial health of discoms has become increasingly critical, particularly given the variable nature of renewable generation and the growing demand for reliable power supply. In this context, the performance of Maharashtra’s discoms presents a mixed picture when compared with the all-India average. State-owned Maharashtra State Electricity Distribution Company Limited (MSEDCL) underperformed compared to the national average on several operational parameters (see table). The utility recorded higher aggregate technical and commercial (AT&C) losses and lower billing efficiency. Although its collection efficiency remained broadly comparable to the national level, the discom reported a higher ACS-ARR gap. In contrast, Adani Electricity Mumbai Limited (AEML) performed significantly better across most parameters. The utility reported significantly lower AT&C losses along with stronger billing and collection efficiency. It also recorded a negative ACS-ARR gap, faring better than both MSEDCL and the national average.

Further, smart meter roll-out is gaining traction in Maharashtra as part of efforts to improve billing efficiency and reduce distribution losses. Data from the National Smart Grid Mission indicates that 23,564,747 smart meters have been sanctioned in the state, of which 9,204,549 have been installed so far, translating into an installation progress of about 39.06 per cent. This installation progress is significantly higher than the national average of 25.88 per cent.

Additionally, Maharashtra’s per capita electricity consumption is higher than the national average across all major sectors. In 2024-25, the overall per capita electricity consumption in Maharashtra stood at 1,299.4 units compared to 1,010.6 units at the all-India level. The difference is particularly evident in the industrial sector, where consumption in Maharashtra reached 511.7 units as against 340.6 units in India, highlighting the state’s position as a key industrial hub. Similarly, commercial consumption was higher at 127.4 units in Maharashtra compared to 95.1 units nationally. Higher consumption is also observed in the agriculture and domestic sectors, at 300.4 units and 290.9 units respectively, in Maharashtra, compared to 205.5 units and 273.1 units at the national level. This trend has persisted in Maharashtra since 2022-23.

On the generation side, Maharashtra recorded an average renewable energy generation of about 21,324 MUs per year between 2022-23 and 2024-25. In addition, the state generated 17,761 MUs of renewable energy in 2025-26 (till December 2025). As per the CEA’s renewable generation reports, Maharashtra recorded an average renewable energy generation of 40.19 MUs per day in February 2026. Of this, solar power accounted for 29.38 MUs while wind accounted for 10.80 MUs. Other renewable sources, including biomass, bagasse and small hydro, did not contribute to the state’s renewable generation during the month.

The CEA’s quarterly report on under-construction renewable energy projects released in September 2025 indicates that Maharashtra has over 9 GW of renewable energy projects under construction. This includes 3,524.3 MW of solar capacity, 3,701.9 MW of wind capacity and 2,190 MW of hybrid capacity. Maharashtra’s project pipeline reflects its focus on developing a diversified renewable energy mix.

Outlook

Outlook

The state faces several challenges that need to be addressed going forward. High grid tariffs across consumer categories and high consumption levels under both MAHADISCOM and BEST remain a concern. The lowest tariffs are charged for BPL (below poverty line) consumers at Rs 3.09 per unit under MAHADISCOM and Rs 3.86 per unit under BEST. Residential tariffs increase significantly with higher consumption slabs, reaching up to Rs 19.15 per unit under MAHADISCOM and Rs 14.45 per unit under BEST for consumption above 500 units. Commercial consumers face some of the highest tariffs, with rates ranging from Rs 13.09 per unit to Rs 19.04 per unit under MAHADISCOM and between Rs 8.81 per unit and Rs 9.73 per unit under BEST, depending on the load category. Industrial tariffs are comparatively lower, ranging from Rs 8.64 per unit to Rs 10.17 per unit for the LT industry under MAHADISCOM and from Rs 8.51 per unit to Rs 9.69 per unit under BEST, while HT industry tariffs stand at Rs 10.78 per unit and Rs 7.88 per unit respectively. These retail tariffs are considerably higher than the average cost of power procurement. During 2024-25, the average cost of electricity purchased was Rs 5.73 per unit for MAHADISCOM and Rs 6.16 per unit for BEST.

While high commercial and industrial (C&I) tariffs in Maharashtra could affect manufacturing competitiveness, a positive aspect is that they provide an incentive for C&I consumers and high electricity consuming residential consumers to shift towards renewable energy solutions.

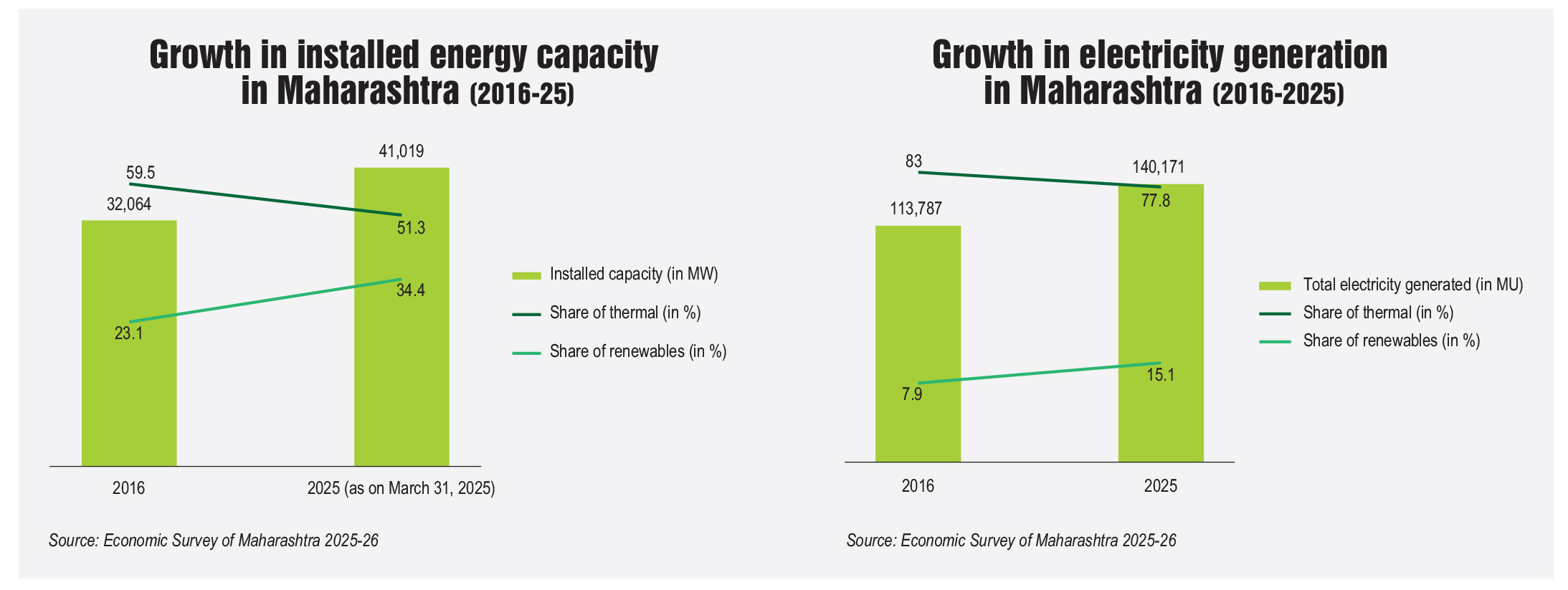

Another challenge in the state apart from high grid tariffs is the heavy dependence on thermal power despite the expansion of renewable capacity. According to the CEA, as of January 2026, out of the total installed capacity in Maharashtra, the share of thermal is around 43 per cent, while that of renewables is over 52 per cent. However, installed capacity alone does not accurately reflect the actual contribution of different energy sources to electricity generation. According to Maharashtra’s Economic Survey 2025-26, over 77 per cent of the total power generation in the state in 2024-25 came from thermal sources while the share of renewables was only about 15 per cent. Also, energy generation from renewables in the state increased by 15,994 MUs between 2010-11 and 2024-25, whereas thermal generation increased by 56,314 MUs during the same period, indicating that growth in renewable electricity generation has been relatively slower.

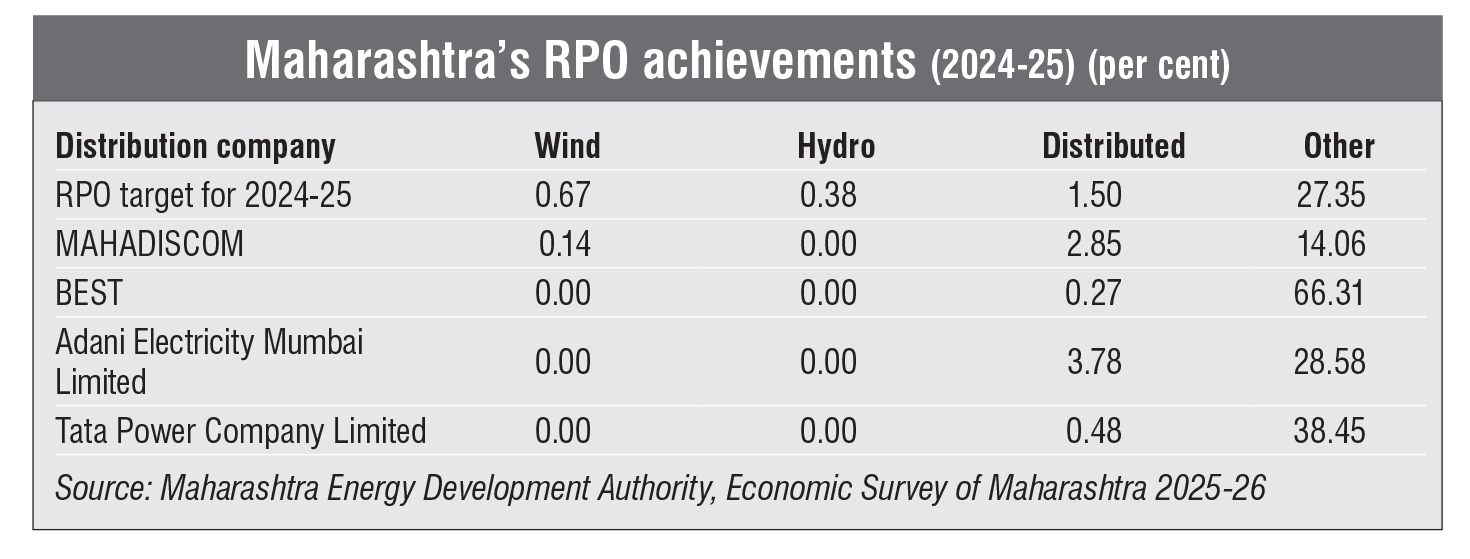

Furthermore, the distribution utilities of Maharashtra also fall short of meeting their renewable purchase obligation (RPO) targets. Against the wind RPO target of 0.67 per cent, MAHADISCOM achieved only 0.14 per cent, while BEST, AEML and Tata Power reported no wind procurement. Similarly, the hydro RPO target of 0.38 per cent was not met by any of the discoms. While distributed renewable procurement exceeded the 1.5 per cent target in some cases, such as AEML at 3.78 per cent and MAHADISCOM at 2.85 per cent, overall compliance remained uneven.

Looking ahead, the Maharashtra government has approved the Maharashtra Renewable Energy and Energy Storage Policy 2025-2035 to support the long-term expansion of clean energy. According to the policy, by 2035, the state aims to develop 100 GW of renewable energy capacity along with around 100 GWh of energy storage capacity. However, the current installed renewable capacity in the state is only about 31 GW, indicating that nearly 69 GW of additional renewable capacity will need to be added over the next decade to meet future targets. This translates into an average requirement of about 6.9 GW of renewable capacity addition each year. In comparison, between March 2021 and March 2025, the state added renewable capacity at an average rate of around 3 GW per year. Therefore, achieving the new target will require a significant acceleration in renewable energy deployment, along with faster transmission expansion, smoother land acquisition processes, and better coordination between renewable energy project development and grid infrastructure planning.