By Karan Sharma

India’s renewable energy financing landscape has entered a more mature and structured phase over the past one year as policy support, budgetary allocations, increased foreign direct investment (FDI), institutional lending and public market activity have deepened capital pools for the sector. Meanwhile, the expanding equity market and initial public offering (IPO) pipeline have created a parallel route for raising capital.

That said, financing needs remain substantial. Meeting the 500 GW non-fossil fuel target by 2030 still requires more than $300 billion in aggregate investment according to EMBER, translating into an annual requirement of over $60 billion. This target is much higher than the $20.893 billion that the sector managed to mobilise across all financial instruments over the past year, as per Renewable Watch Research.

Against this backdrop, Renewable Watch reviews the key equity and debt deals, green bond issuances and IPO activity in the renewable energy sector over the past year…

Debt markets remain the backbone

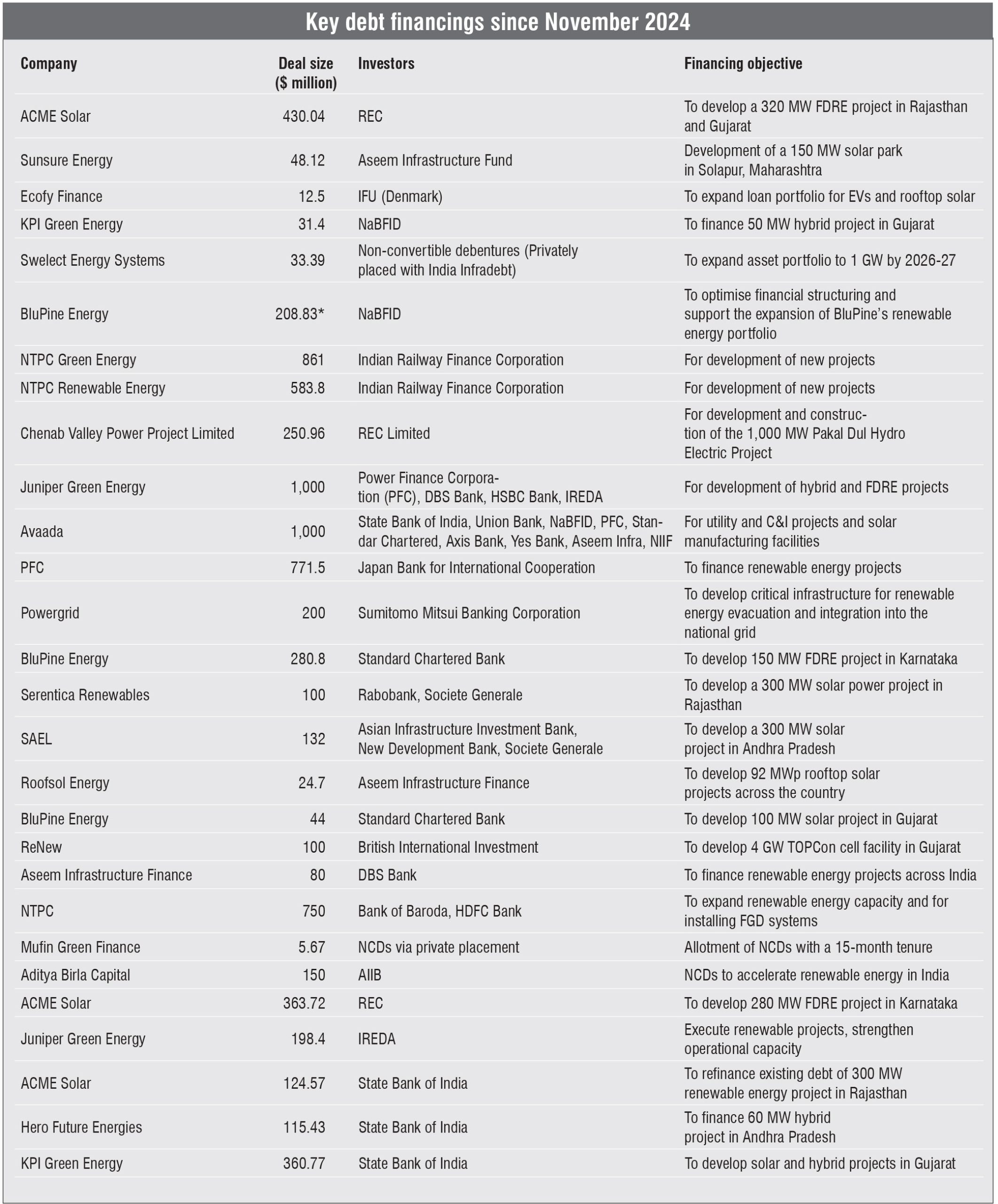

Debt remains the backbone of project finance in India’s renewables sector. As per Renewable Watch Research, over the past year, $10,098.58 million was channelled through 39 debt instruments, consisting of loans as well as non-convertible debentures. Despite active equity markets, project economics continue to rely heavily on commercial banks and development finance institutions (DFIs) to provide credit. For mature technologies such as utility-scale solar, wind and wind-solar hybrids, industry funding, DFIs and commercial banks are the primary lenders due to the established and risk-averse nature of these technologies as well as their ability to be scaled up rapidly. As for emerging technologies such as green hydrogen and utility-scale energy storage, government incentives and viability gap funding remain essential for achieving bankable returns.

The Power Finance Corporation and the State Bank of India were reportedly the largest lenders during the past year, with outstanding renewable loans exceeding $9.5 billion and $9 billion respectively, as of March 2025. Further, PSU non-banking financial institutions (NBFCs) such as the Indian Renewable Energy Development Agency, the Indian Railway Finance Corporation (IRFC), REC Limited; DFIs such as the Asian Development Bank, Japan Bank for International Cooperation (JBIC) and the National Bank for Financing Infrastructure and Development; and commercial and international banks such as HDFC Bank, Standard Chartered Bank and Sumitomo Mitsui Banking Corporation have also been the key financiers of renewable energy projects over the past year.

Some of the major debt deals that were signed over the past year include ACME Solar’s $430.04 million loan from REC in November 2024 to fund the development of a 320 MW firm and desptachable renewable energy project in Rajasthan and Gujarat; PFC’s $771.5 million loan from JBIC for renewable energy project financing in January 2025; and NTPC Green Energy Limited’s (NGEL) $861 million loan from IRFC in March 2025. These transactions over the past year indicate that both PSU as well as private developers are securing large, long-tenor loans from NBFCs, underscoring their critical role in renewable funding.

Equity flows deepen

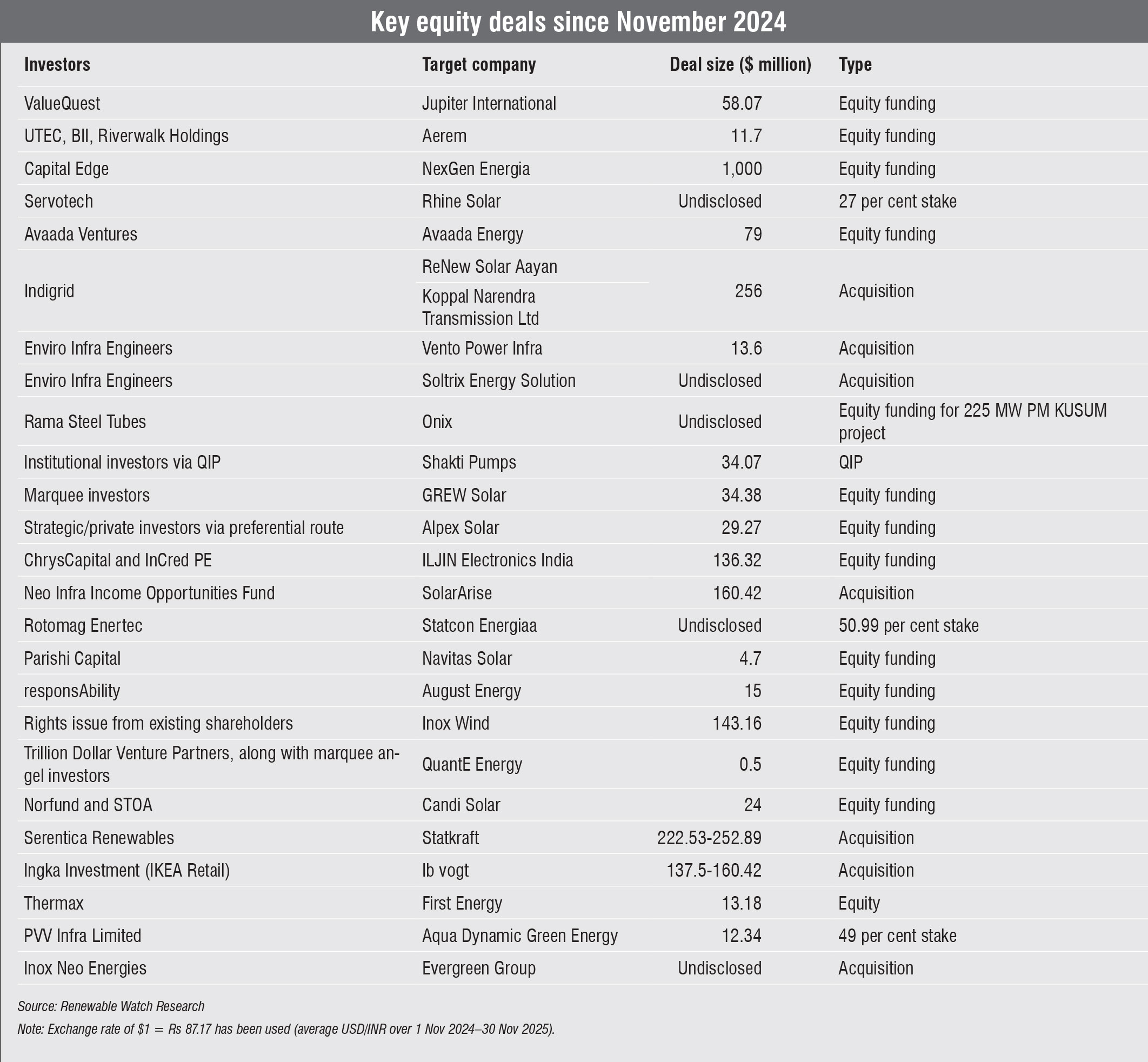

Private equity (PE) has continued to commit sizeable sums to scale capacities and consolidate portfolios. Over the past year, equity funding totalling $6,466.409 million across 45 deals has been tracked by Renewable Watch Research. PE and strategic investors have been active across multiple entry points, with transactions spanning acquisitions, stake purchases on renewable energy platforms, rights issues, qualified institutional placements (QIPs) and corporate joint ventures (JVs).

FDI liberalisation, allowing up to 100 per cent foreign ownership under the automatic route, has been a significant policy enabler for this rise of equity deals in the sector, ever since its November 2022 implementation. It led to a 50 per cent year-on-year increase in FDI in during 2022-23 and 2023-24. Sectoral FDI inflows during 2024-25 stood at about $4 billion as of March 2025, supporting both project development and domestic manufacturing initiatives.

Some of the most significant equity deals over the past year were NexGen Energia’s $1 billion equity investment from Capital Edge to scale compressed biogas infrastructure in April 2025, IREDA’s $234.7 million QIP in June 2025 to strengthen its lending capacity for renewables and Inox Wind’s $143 million rights issue in July 2025 to raise funds to support its expansion plans across the wind supply chain. These deals indicate that PE and institutional investors are focusing on companies with clear and credible deployment pipelines.

Acquisition and JV activity remained strong as PSUs, sovereign funds and private developers continued to secure operating portfolios and long-term revenue streams. Key transactions include ONGC–NTPC Green JV’s $2.3 billion enterprise-value acquisition of Ayana Renewable Power, completed in March 2025; Brookfield’s sale of roughly $900 million worth of operating solar and wind assets aggregating 1.6 GW to Gentari Renewables; and Siemens Gamesa’s $500 million–$550 million majority stake sale of its India wind business to a TPG-led investor group.

IPO momentum builds

Public listings have emerged as an important capital-raising strategy for renewable energy companies. Over the past year (from November 2024 to November 2025), the total fresh-issue capital raised through IPOs amounts to $2,498.72 million, including offer for sale, as tracked by Renewable Watch Research. Key issuances included ACME Solar’s $274.44 million IPO and NGEL’s $1,145.87 million IPO, both issued in November 2024; Vikram Solar’s $171.88 million IPO in August 2025; and Emvee Photovoltaic Power’s $245.66 million IPO in November 2025.

A larger pipeline remains at the registration stage and is expected to be launched over the remaining financial year. IPO issuance, particularly in FY 2025-26, has increasingly become a preferred route for various renewable energy companies to access markets and public capital. In the first quarter of FY 2025-26, $1,185.97 million of IPO issuance value was recorded in draft red herring prospectus (DRHP) filings. By the second quarter (Q2), this DRHP pipeline had expanded to $2,343.30 million. Q2 FY 2025-26 also saw the highest number of issuances in the sector, accounting for the majority of proceeds tracked till date, with $434.28 million raised through fresh IPO issues.

This IPO wave is driven by two major factors. One, developers and manufacturers are seeking long-duration capital to increase capacity and reduce debt reliance. Second, investor appetite for disclosed, regulatory-compliant renewable firms has risen, supported by improving valuations and liquidity in listed financial instruments.

Bonds gain traction but hurdles remain

Bond markets are an underutilised but growing source of term capital for the sector. Over the past year, over $1,829.37 million has been raised through 11 bond issuances aimed at funding green or renewable energy initiatives, ranging from green municipal bonds to perpetual bonds. Green bond issuances have provided companies with tenors and investor bases not always available from bank loans or other financial instruments.

NBFCs such as IREDA, REC and municipal bodies remain active borrowers in bond markets to refinance and expand their lending programmes. A combination of upcoming refinancing needs for maturing dollar-denominated debt and a growing domestic investor appetite for “greenium”, that is the marginal pricing benefit from green-labelled bonds, suggests that bond financing may play an increasingly important role in the sector, provided pricing and labelling hurdles are addressed.

Nevertheless, international bond markets remain underutilised for Indian renewables. At the sovereign level, green bond performance remained inconsistent. The Reserve Bank of India attempted to reissue $573.59 million of 30-year sovereign green bonds in June 2025, but all bids were rejected due to higher yield expectations. These auctions, with the exception of the debut 2023 issuances, have consistently shown weak demand and limited market depth.

Conclusion

The financing environment in the sector has clearly matured over the past year, but the gap between available capital and required capital remains the most important lens for evaluating the outlook and decisions. Capital formation has improved across instruments – debt, equity, bonds and IPOs – yet the real measure will be whether these flows translate into commissioned capacity, operating portfolios and stable cash flows.

In the debt market, lending remains concentrated among a few PSUs and large commercial banks. This creates pricing bottlenecks for emerging technologies such as hydrogen, offshore wind and storage. Blended finance, credit enhancement and guarantee mechanisms can be key instruments for securing low-cost project debt and bringing new lenders into the market. Multilateral and bilateral DFIs will also need to take a stronger role in early-stage de-risking, particularly for segments where revenue certainty is still evolving.

Meanwhile, despite more diverse and improved equity flow, the pool of investors willing to fund capacity creation outside proven models remains small. Mitigating this requires clearer demand signals, faster approval cycles, and transparent, time-bound incentive frameworks. Without these, even well-designed equity instruments such as QIPs and rights issues will concentrate capital in established players, while new entrants struggle to scale.

The bonds market faces even more fundamental barriers – the absence of greenium, limited liquidity and labelling challenges. For bonds to play a meaningful role, the market requires standardised labelling, a more stable climate finance taxonomy and incentives that nudge institutional investors towards longer-duration bonds while enabling participation from retail investors. Moreover, post-issue disclosures will allow investors to track the deployment of proceeds over time. This transparency is essential to sustain investor confidence as the sector scales.

This applies to IPOs as well. While issuances have increased, the long-term effectiveness of an IPO depends on consistent post-listing performance and regular disclosure of the utilisation of proceeds, confirming whether capital is being deployed as stated in the offer documents. The absence of uniform reporting across issuers creates an information asymmetry for investors, particularly retail participants. To strengthen this, companies will need to publish clear deployment timelines and make their reporting more transparent.

Going forward, the financing outlook depends on tightening the link between capital mobilisation and on-ground progress. It remains to be seen in the coming year whether the sector can convert this financial momentum into bankable projects, and whether that momentum can drive the next phase of the energy transition.