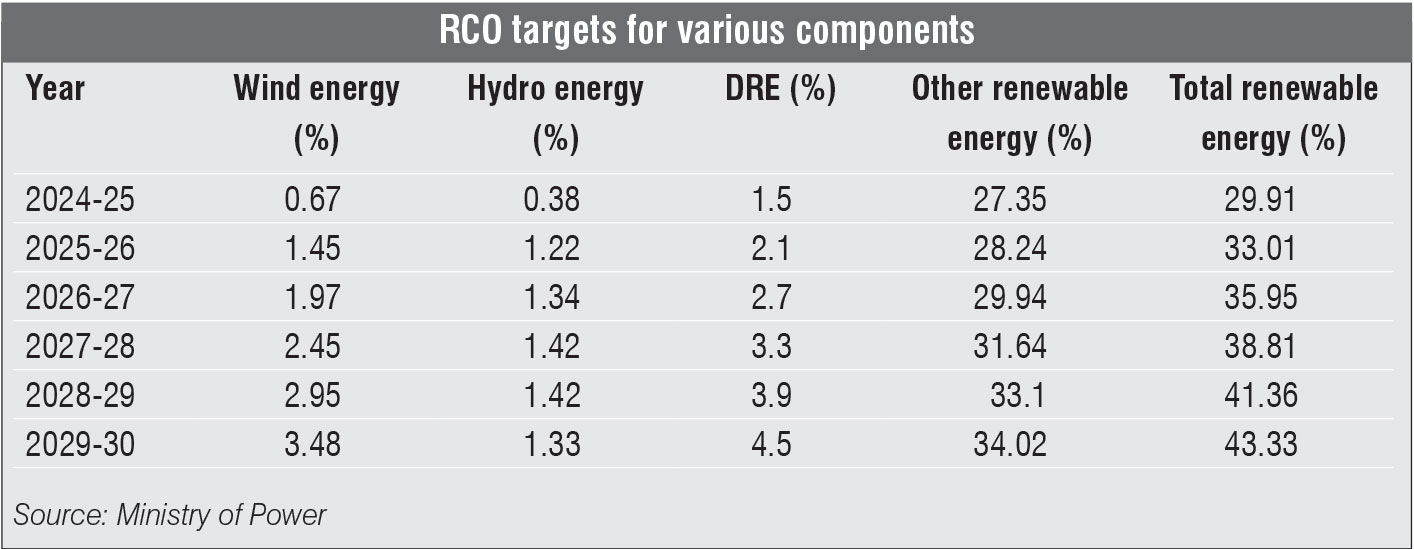

In a push to accelerate India’s decarbonisation goals and increase renewables consumption, the Ministry of Power (MoP), in consultation with the Bureau of Energy Efficiency (BEE), issued a draft renewable consumption obligation (RCO) notification in August 2025, specifying the mandatory year-wise RCO trajectory for all designated consumers, including captive power plants, distribution licensees and open access consumers. To strengthen enforcement and align them with 2030 goals, RCO targets have been specified from 2024-25 to 2029-30, starting at 29.91 per cent and rising in a graded manner to 43.33 per cent with specific quotas for wind, hydro, distributed renewable energy and other sources.

To recall, the RCO mechanism was introduced through a 2022 amendment to the Energy Conservation Act, 2001, which applies to designated consumers, including captive power users and open access consumers, and mandates year-wise consumption targets for renewable energy up to 2029-30. Unlike the renewable purchase obligation (RPO), which was limited to grid-based procurement, the RCO also captures on-site and behind-the-meter sources, thereby covering all forms of renewable electricity consumption.

A closer look at the latest notification and its implications…

Details of the latest draft

In the July draft, the RCO comprises four components – wind, hydro, distributed renewable energy (DRE) and other renewables, each with separate targets for each year. Notably, the share of DRE is mandated to rise from 1.5 per cent in 2024-25 to 4.5 per cent by 2029-30.

The notification clearly states that its provisions supersede all previous RPO-related directives, including those dated October 1, 2019 and October 20, 2023.

As per Clause 6 of the August 2025 notification, designated consumers must submit their RCO compliance reports by May 30 of the following year. These reports are to be certified by the designated plant head and must be independently verified by a BEE-accredited energy auditor by July 31. The consumption data must be based on actual measurements and energy accounting, including meter readings certified by the respective state load dispatch centre (SLDC) or other authorised agencies.

The notification defines electricity consumption as the net self-consumption, excluding auxiliary consumption, and excludes electricity from nuclear sources, waste heat recovery (except from waste heat recovery steam generators in combined cycle gas turbine captive plants) and 50 per cent of fossil fuel-based cogeneration.

Compliance routes

Compliance can be achieved through three mechanisms. The first is consuming renewable electricity through self-generation or procurement from external sources. The second route involves the purchase of renewable energy certificates (RECs), including those linked to virtual power purchase agreements (VPPAs). The third option allows designated consumers to pay a buyout price, as determined by the Central Electricity Regulatory Commission (CERC), in lieu of meeting the prescribed renewable consumption targets. The sums received shall be credited to the Central Energy Conservation Fund and 50 per cent of the shall be given to the State Energy Conservation Fund. Additionally, the wind, hydro and other renewable components are fungible, which means that surplus in one can meet the shortfall in another, with the exception of the DRE component. Non-compliance will attract penalties under the Energy Conservation Act, 2001. The notification also designated BEE and state-designated agencies (SDAs) to monitor compliance, and any of these entities may initiate proceedings before the adjudicating officer.

What the draft gets right

A key strength of the notification is its multiple compliance options, which offer flexibility to entities. This way, designated consumers can meet their obligations through direct consumption of renewable energy, purchase of RECs (including those linked to VPPAs) or through payment of a buyout price. The framework also introduces component-level fungibility across wind, hydro and other renewable energy. If an entity exceeds its target in one of these components, it may offset shortfalls in the others. However, shortfalls in DRE cannot be offset by surplus in other components. This non-fungibility is intended to preserve policy space for decentralised energy solutions, such as rooftop solar, mini-grids and small-scale renewable systems. This is a critical step in ensuring wider geographical and social participation in the energy transition, as these technologies are often deployed by micro, small and medium enterprises, local entrepreneurs and even under the flagship PM Surya Ghar: Muft Bijli Yojana. The notification also provides clear treatment for captive power plants. For industrial consumers generating their own electricity, the RCO applies to self-consumed electricity, excluding auxiliary consumption. This ensures that captive consumption is brought within the renewable transition framework, without penalising internal operational requirements. Similarly, cogeneration from fossil fuels is partially exempt, with only 50 per cent of self-consumed electricity from such systems subject to RCO in recognition of the efficiency benefits of cogeneration. There is also clarity on exclusions. For example, electricity from nuclear sources and power generated through fossil-based waste heat recovery (WHR) are not included in the RCO calculation. However, WHR-based electricity from steam generators in combined cycle gas-based captive plants is included. Lastly, the notification reinforces the democratisation of energy access.

Concerns

While the RCO framework introduces a more comprehensive approach to renewable energy compliance, there are several concerns that still remain around the binding nature and legal clarity.

Although the buyout mechanism offers several compliance options, there are still some issues with the legal foundation under the Energy Conservation Act, 2001. For instance, the act does not explicitly attribute the role of setting such a price to the CERC, nor does it specify how buyout funds are to be administered. Although the notification states that these funds will be deposited in the central and state energy conservation funds, there is no exact methodology to give clarity on how they will be utilised. Specifically, the second compliance route, which is the REC market, may not be as effective.

Meanwhile, large steel and aluminium makers have sought changes to the proposed regime, proposing a downward revision in the mandatory share of renewable energy in their consumption and exclusion of electricity generated from waste heat gases from the ambit of RCO. Steel producers have also urged the government to exclude transmission losses from RCO calculations to improve resource optimisation and reduce financial burdens. Steel and aluminium producers are mandated to meet 33.01 per cent of their total captive electricity consumption from renewable sources in the current financial year, up from 29.91 per cent in FY2025.

Despite the announcement of higher RCO targets and potential penalties, trading volumes and prices of the REC market go through sluggish trading patterns throughout the year, where they remain low at the start of the year and then rise as the year ends, as entities aim to meet their obligations. This highlights volatility in supply and demand throughout the year. Additionally, although the notification recognises regional variation in topography or geography, it does not grant individual states or SLDCs the ability to set their own RCO targets. Instead, all targets are centrally specified by the MoP, which will limit state-level flexibility to set targets. The notification also appears to have made the enforcement structure more complex than it needs to be. BEE, SDAs and adjudicating officers are to initiate non-compliance proceedings; however, this multi-agency approach might risk creating overlaps or jurisdictional conflicts. Despite the provision of three overlooking entities, there is no mention of a centralised compliance ledger that may tackle the problem of double-counting or data reporting integrity. These are all concerns that are likely to appear for group companies that operate in multiple states.

The way forward

The RCO framework offers a path to scale up renewable energy consumption across the industrial, commercial and distribution segments. Its long-term trajectory will likely create demand certainty for clean energy investments. However, its effectiveness will ultimately depend on how well central directives are translated into state-level execution.

The central government’s target of 500 GW of non-fossil fuel capacity by 2030 depends not only on capacity addition but also on actual consumption and utilisation. The introduction of state-wise obligation indicators or adaptive compliance benchmarks could improve alignment with regional load and generation patterns. In parallel, market-based mechanisms require further strengthening.

Going forward, the success of the RCO will rest on how well it is integrated with broader reforms in the power sector. It will also be necessary to align it with emerging policies on energy storage and carbon markets to achieve both decarbonisation and grid reliability goals. A unified and coordinated policy approach will be key to ensuring that the RCO serves as an effective instrument for driving India’s clean energy transition.

By Ali Siddiqui