India’s power sector is witnessing a significant transformation, driven by the rapid integration of variable renewable energy into the grid. This transition has disrupted traditional load patterns, creating an urgent need for greater flexibility in grid operations. In response, utilities are increasingly adopting standalone battery energy storage systems (BESSs) across the power sector supply chain, encompassing generation, transmission and distribution. For utilities, BESS is emerging as a key enabler for meeting peak power demand, ensuring power quality, supporting renewable integration and enhancing overall grid reliability.

The rationale behind this lies in the evolving nature of India’s electricity demand curve, which has become significantly peakier. While solar generation peaks in the afternoon when demand is relatively low, the demand surges in the evening hours when solar output declines sharply. This mismatch between supply and demand has created a need for storage solutions that can bridge this gap.

Given the limitations of thermal plants in ramping up and down quickly, the evening peak deficit poses significant operational challenges for grid operators. The absence of flexible generation leads to the curtailment of surplus solar during the day. This is where battery storage systems prove crucial, as these systems can store excess solar power during the day and discharge it in the evening to meet the peak demand, thereby avoiding both curtailment of renewables and inefficient coal cycling. Thus, BESS offers a viable solution by supporting grid balancing and enhancing the utilisation of renewable energy.

Recognising this, the Indian government has given a significant push to the BESS segment through a budget allocation of Rs 37.6 billion for viability gap funding (VGF) for 13.2 GWh of capacity (increased from the initial target of 4 GWh given the fall in battery prices). To benefit from this incentive, several states have issued a wave of standalone BESS tenders in recent months. According to Renewable Watch Research, around 12 standalone BESS tenders have been issued since January 2025, and five tenders have been auctioned. This article provides an overview of tenders that have been auctioned since January 2025…

Recent standalone BESS auctions

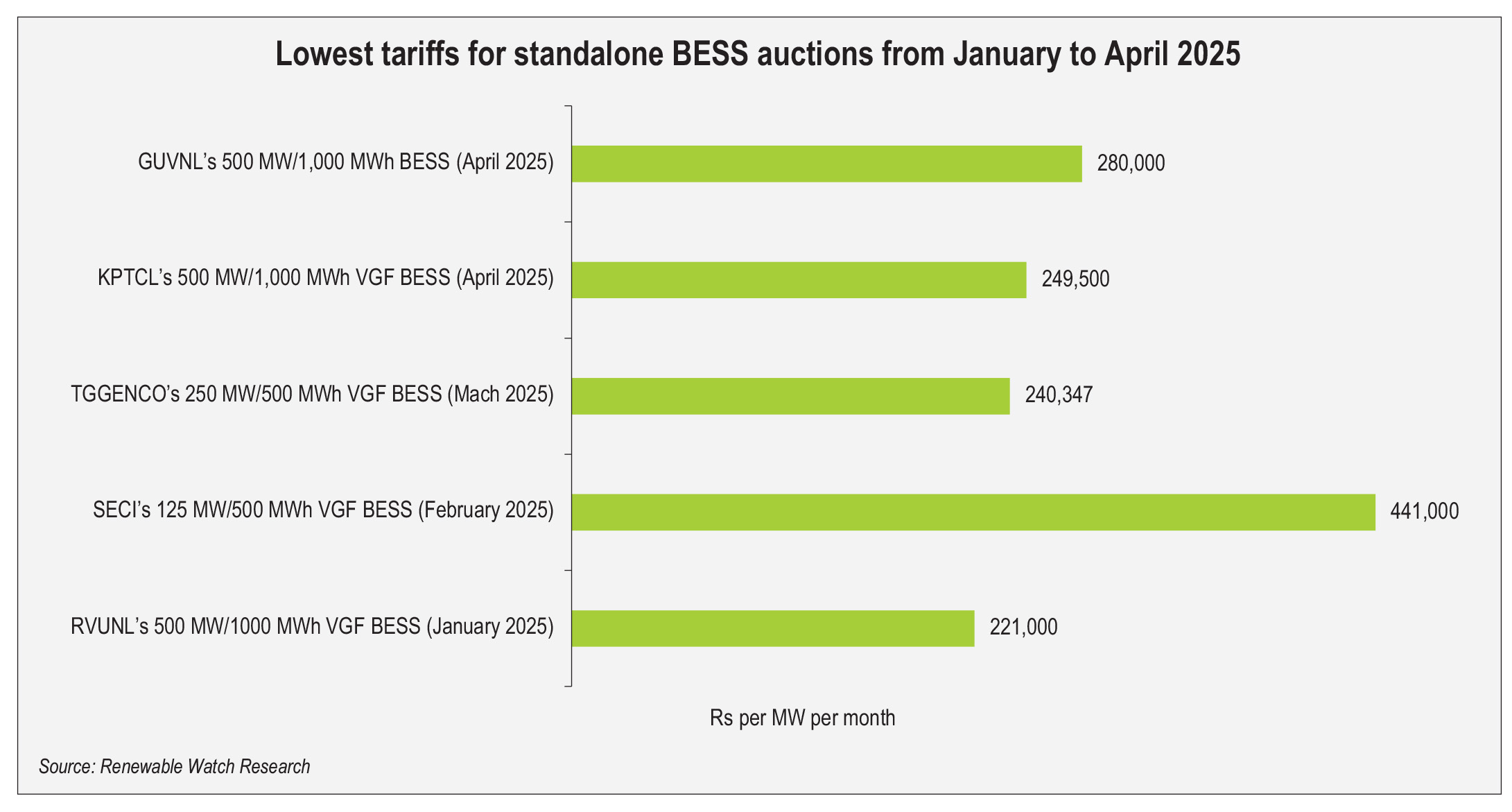

The year began with Rajasthan Rajya Vidyut Utpadan Nigam Limited’s (RVUNL) VGF auction in January 2025, in which four companies secured capacity totalling 500 MW/1,000 MWh for standalone BESS. SolarWorld Energy Solutions won with the lowest bid of Rs 221,000 per MW per month for 125 MW/250 MWh capacity, followed by Oriana Power at Rs 222,000 per MW per month for 50 MW/100 MWh, Rays Power Experts at Rs 223,000 per MW per month for 75 MW/150 MWh, and JSW Neo Energy secured 250 MW/500 MWh at a tariff of Rs 224,000 per MW per month.

In February 2025, the Solar Energy Corporation of India (SECI) conducted a 125 MW/500 MWh standalone VGF BESS auction for Kerala, where JSW Energy emerged as the sole winner, taking the entire capacity at a tariff of Rs 441,000 per MW per month.

In March 2025, Telangana Power Generation Corporation’s (TGGENCO) VGF tender for 250 MW/500 MWh standalone BESS was auctioned, with Bondada Engineering securing 50 MW/100 MWh at Rs 240,347 per MW per month, while Oriana Power and Pace Digitek won 50 MW/100 MWh and 125 MW/250 MWh at nearly same tariffs of Rs 245,152 per MW per month and Rs 245,153 per MW per month respectively.

April 2025 concluded with two major auctions. Karnataka Power Transmission Corporation Limited’s (KPTCL) VGF tender for 500 MW/1,000 MWh of standalone BESS was awarded to three winners. Sarala Project Works secured 50 MW/100 MWh at Rs 249,500 per MW per month, while both Pace Digitek and Oriana Power secured 250 MW/500 MWh and 50 MW/100 MWh respectively at Rs 254,490 per MW per month. Then, Gujarat Urja Vikas Nigam Limited’s (GUVNL) 500 MW/1,000 MWh standalone BESS tender concluded with Solarworld Energy Solutions winning 200 MW/400 MWh at Rs 280,000 per MW per month and H.G. Infra Engineering securing 300 MW/600 MWh at Rs 285,600 per MW per month.

These auctions have revealed pricing trends, highlighting the impact of VGF and project specifications on tariff outcomes. The lowest discovered tariff emerged from the RVUNL auction, supported by VGF, at Rs 221,000 per MW per month. This was closely followed by TGGENCO’s VGF-backed auction at Rs 240,347 per MW per month, and KPTCL’s tender at Rs 249,500 per MW per month. Interestingly, even in the absence of VGF support, GUVNL secured a competitive tariff of Rs 280,000 per MW per month, reflecting growing market maturity and cost efficiencies. In contrast, SECI’s Kerala auction yielded a higher tariff of Rs 441,000 per MW per month. However, this is attributable to its unique requirement of four-hour storage duration (125 MW/500 MWh), unlike the two-hour configurations in other tenders, effectively doubling the storage requirement and, consequently, the tariff.

The clustering of VGF-supported tariffs between Rs 221,000-Rs 249,500 per MW per month indicates market stabilisation, while the non-VGF tariff at Rs 280,000 per MW per month signals growing commercial viability. Looking ahead, it is possible that significant VGF may no longer be necessary, given the fall in battery prices. Another notable trend is the repeated participation of certain developers across multiple auctions. Oriana Power secured capacity in three different tenders, while SolarWorld Energy Solutions and Pace Digitek each won in two auctions.

Future outlook

The year 2025 has been quite eventful, witnessing successful auctions and the discovery of competitive tariffs. According to Renewable Watch Research, around 6 GW of standalone BESS tenders were floated in early 2025. This uptick in activity is encouraging for the market. Going forward, the activity in the storage market is expected to grow with the decline in battery prices and initiatives such as production-linked incentives, VGF and evolving regulatory instruments such as energy storage obligations, which are providing the necessary fillip.

A major challenge is the sourcing of battery cells, as highlighted by Debmalya Sen, President, India Energy Storage Alliance. Almost all winning developers continue to import battery packs, primarily from China, given India’s limited domestic manufacturing capacity. For this, Sen shared that the government should explore mechanisms such as the Approved List of Battery Manufacturers, akin to the Approved List of Models and Manufacturers for solar modules.

Going forward, the outlook for the BESS market remains optimistic, especially as the economics of storage continue to improve and grid flexibility becomes non-negotiable in a renewables-dominated future. With India’s BESS auction pipeline rapidly expanding, it will be interesting to see whether this momentum can be sustained in the coming years.