India has set an ambitious target of achieving 500 GW of non-fossil fuel capacity by 2030 as part of its commitment to a cleaner and more sustainable future. To reduce carbon emissions and meet international climate obligations, achieving this target is key. With over 200 GW of renewable energy (including large hydro) capacity already installed, the country is well on its way to achieving this target.

Although there are several factors responsible for this growth trajectory, a key factor behind this has been India’s auction regime, which prioritises competitive tariff-based bidding. One could argue that the shift has fundamentally transformed the renewable energy market, driving down tariffs, encouraging private sector participation, and ensuring cost optimisation across projects. Auctions create an environment of healthy competition, allowing developers to bid transparently and competitively, thereby improving price discovery. The impact of this shift is visible not only in falling tariffs but also in enhanced investor confidence and an accelerated pace of project installations. By ensuring a fair and open process, the system fosters trust among all stakeholders in the renewable energy landscape. India’s transparent bidding system is central to the entire process. The result is a robust ecosystem where investors see long-term viability, and renewable energy projects are able to achieve scale and cost efficiency.

For instance, as per CareEdge Ratings Research, renewable energy tariffs have already become competitive against their thermal counterparts. Over the years, solar has seen a decline in bid tariffs while in the case of wind, bid tariffs have gradually risen. As a result, these tariffs remain highly competitive against the marginal variable cost of generation in the bottom 25 per cent of the merit order dispatch of the state distribution utilities.

For instance, as per CareEdge Ratings Research, renewable energy tariffs have already become competitive against their thermal counterparts. Over the years, solar has seen a decline in bid tariffs while in the case of wind, bid tariffs have gradually risen. As a result, these tariffs remain highly competitive against the marginal variable cost of generation in the bottom 25 per cent of the merit order dispatch of the state distribution utilities.

The argument is reinforced further through the paper “Analysing the falling solar and wind tariffs: evidence from India” by Kanika Chawla, Manu Aggarwal and Arjun Dutt in the Journal of Sustainable Finance & Investment. Here, the authors have highlighted the significant decline in solar and wind tariffs over the past few years. The authors argue that the primary drivers of this trend are the falling unit equipment costs that have contributed directly to reduced unit project costs while bringing down renewable energy tariffs.

Consequently, according to the paper, the renewable energy tariffs in India started to see a decline in 2017, with record-low tariffs of Rs 2.44 per kWh for utility-scale solar and Rs 2.43 per kWh for wind energy projects. These price reductions were largely driven by declining equipment costs and the introduction of competitive auctions, which have played a pivotal role in enabling efficient price discovery and making renewable energy more affordable.

As the year 2024 comes to a close, Renewable Watch examines the key auctions and trends across the solar, wind and hybrid segments, highlighting tariff discoveries and the performance of major central agencies, to shed light on the evolving renewable energy landscape.

Solar

Renewable Watch Research tracked a total of 17 solar auctions over the past year (November 2023-December 2024), with an aggregate capacity of 22,375 MW awarded during the period. In terms of the largest single capacity awarded, National Hydroelectric Power Corporation’s (NHPC) 3,000 MW auction in November 2023 leads the way followed by several 1,500 MW capacities being awarded. In terms of tariff trends, the lowest tariff discovered was Rs 2.15 per kWh under Rewa Ultra Mega Solar Limited’s (RUMSL) 170 MW auction in December 2024, showcasing continued cost competitiveness in the sector. Meanwhile, the highest tariff recorded was Rs 2.68 per kWh during NTPC Limited’s Tranche-III 1,500 MW auction in May 2024. A closer look at central-level and state-level auctions reveals that central agencies such as Solar Energy Corporation of India Limited (SECI), NTPC Limited and Power Finance Corporation (PFC) awarded a combined capacity of 19,050 MW at an average tariff of Rs 2.56 per kWh, while state-level agencies such as Gujarat Urja Vikas Nigam Limited (GUVNL) and RUMSL awarded 3,395 MW. Based on this, one could argue that the marginal difference demonstrated in these tariffs reflects the cost efficiency of central-level auctions because they benefit from better economies of scale and lower risk perceptions compared to projects awarded at the state level.

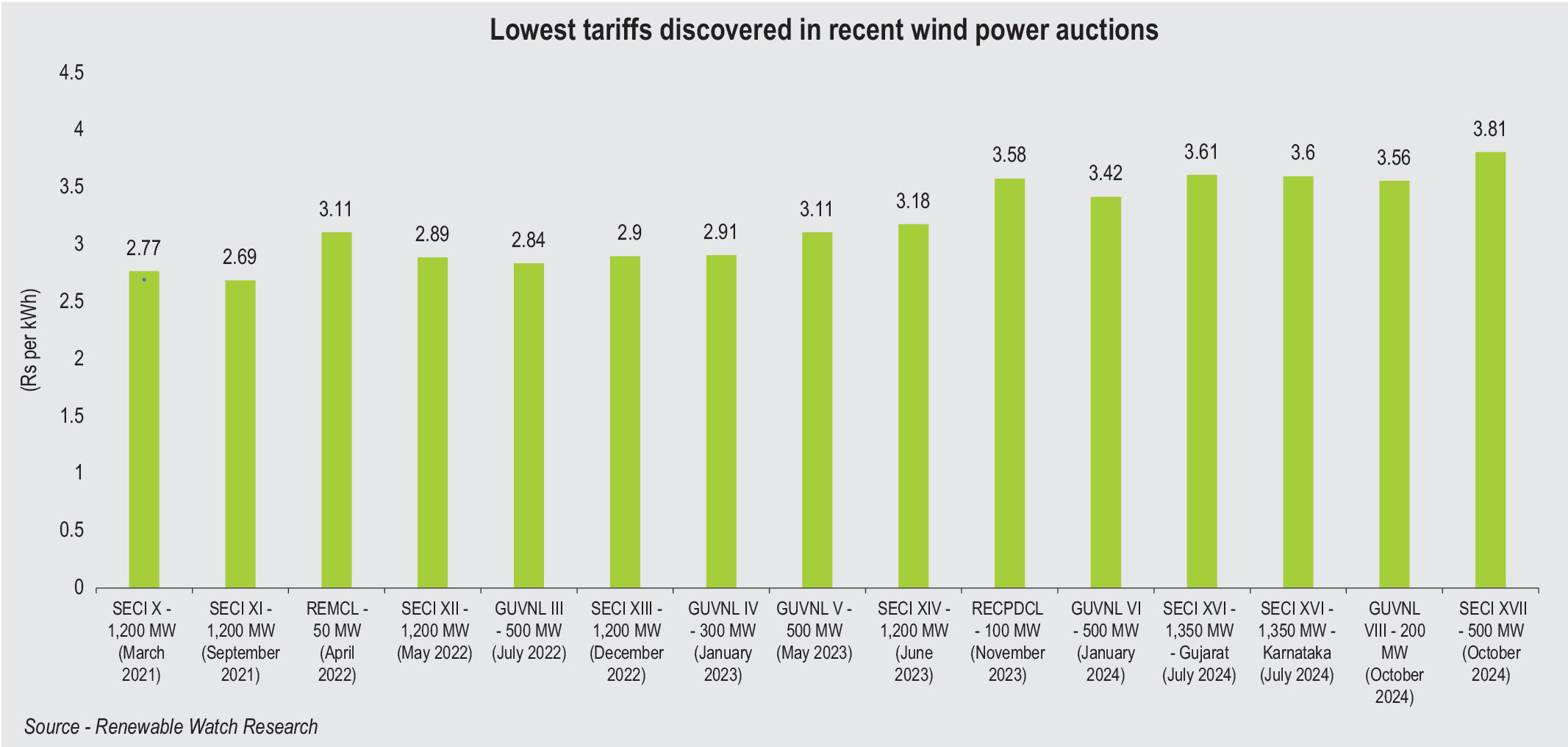

Wind

Renewable Watch Research has tracked five wind energy auctions (November 2023-December 2024), providing crucial insights into tariff movements and the tendering process. The lowest tariff discovered for the year was Rs 3.42 per kWh under GUVNL’s Tranche-VI 500 MW auction in January 2024, marking a notable increase compared to Rs 2.91 per kWh, the lowest tariff in 2023, and Rs 2.84 per kWh, the lowest tariff in 2022. This represents a 17 per cent rise in tariffs from 2022 to 2024, signalling an upward trend in wind energy tariffs. The overall highest tariff recorded in the past two years is Rs 3.81 per kWh witnessed in SECI’s Tranche-XVII 500 MW auction in October 2024.

The wind energy segment in India saw the highest capacity being awarded under SECI’s Tranche-XVI 1,350 MW auction in July 2024 (covering Gujarat and Karnataka). Despite the scale, tariffs for this auction remained elevated at Rs 3.6 per kWh-Rs 3.61 per kWh, reflecting cost pressures and site-specific challenges.

While it is difficult to lay a finger on a particular factor causing an increase in tariffs, one of the most prominent reasons could be attributed to challenges such as rising input costs and land acquisition hurdles, which have put upward pressure on pricing in the wind energy segment. These trends indicate that wind tariffs are departing from the record-low tariffs seen in previous years and highlight the wind energy segment’s current high costs and implementation hurdles.

Hybrid, RTC and FDRE

Hybrid, round-the-clock (RTC), and firm and dispatchable renewable energy (FDRE) projects have shown a wide range of tariff trends over the past year, due to their inherent complexity and additional requirements. Renewable Watch Research has tracked over 25 auctions covering both state and central agencies throughout the year. Central-level agencies, including SECI, NTPC and NHPC, conducted the majority of auctions, collectively accounting for 20 out of 25 tenders. SECI led the effort with the highest number of auctions, particularly for its FDRE projects. The lowest tariff was recorded at Rs 2.99 per kWh in GUVNL’s 500 MW wind-solar hybrid auction which was conducted in January 2024. Meanwhile, the highest tariff of Rs 5.59 per kWh was observed in SECI’s Tranche-II 1,500 MW FDRE auction (March 2024). Overall, hybrid projects with storage or FDRE commitments have demonstrated a variance between Rs 3.5 per kWh and Rs 5.6 per kWh, indicating that reliable and uninterrupted power supply comes with a premium charge. This price variation is primarily driven by the complexity of integration, as hybrid systems must optimise solar and wind energy generation while incorporating energy storage and dispatchable energy management. Overall, while central-level agencies may have dominated in terms of auction volume and awarded capacity, state-level agencies achieved more competitive tariffs, particularly in non-FDRE tenders.

Conclusion and future outlook

Based on the above analysis, solar energy has retained its leadership position and achieved the lowest tariffs. Despite the upward tariff trends, wind energy remains crucial to meeting the country’s renewable energy targets. Although hybrid projects are priced at a premium, they are gaining traction as a reliable solution for delivering firm and dispatchable power, and addressing the challenges of intermittency in renewable energy generation.

Going forward, as per CareEdge Research, the renewables sector can expect marginal tariff hikes in the medium term. Hence, scaling up renewable energy and storage capacities at lower costs will be key. The introduction of new accounting norms will also play an important role, creating short-term challenges but proving beneficial in the long run by encouraging transparency.

Despite these bottlenecks, India’s transparent bidding regime and competitive auction processes remain its biggest strengths, ensuring fair price discovery and attracting investment. However, to maintain cost competitiveness globally, it will be essential to address input costs, streamline project execution, and improve grid infrastructure to capture the surging power demand.