By Lavkesh Balchandani

India’s hydropower sector stands at the forefront of the country’s energy transition. With the increasing uptake of intermittent renewable energy sources, such as wind and solar, hydropower’s role in the energy mix has evolved from that of a traditional baseload generator to a critical grid balancing asset. With pumped storage emerging as the country’s preferred large-scale energy storage solution, the importance of hydropower has extended far beyond conventional power generation. From providing crucial grid services such as frequency regulation and voltage support to offering black start capability during outages, hydropower has become indispensable in India’s journey towards a sustainable energy future.

In this article, Renewable Watch presents an update of the current status, key developments, and emerging trends in the hydro sector over the previous year…

Current status and growth trends

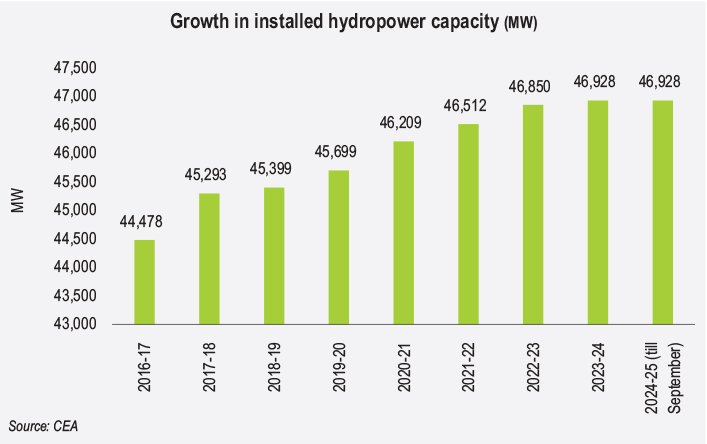

According to the Central Electricity Authority (CEA), as of November 2024, large hydropower installations stand at 46,928 MW, accounting for approximately 10.4 per cent of the country’s total installed power generation capacity. The capacity additions in the sector have been relatively conservative, with only 1,229 MW added between 2019 and 2024. During 2023-24, 2,880 MW was programmed to be added; however, due to slow progress and calamities affecting certain projects, only 60 MW could be added.

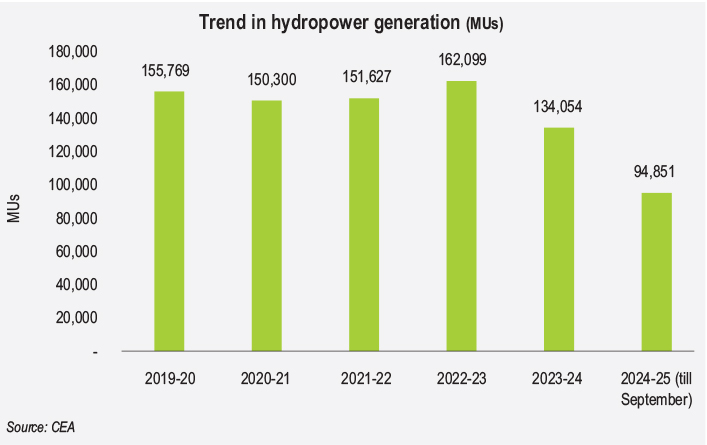

Furthermore, erratic rainfall and natural disasters led to a 17.76 per cent drop in hydropower generation, reducing its contribution in the energy mix from 11 per cent to 9 per cent. However, in 2024-25 (as of September 2024), the contribution of hydropower in the total power generation has increased to 11.6 per cent, as per CEA data.

This year, 3,950 MW of hydropower capacity is programmed to be added, out of this only 40 MW has been achieved so far. As of November 2024, 28 large hydropower projects totalling 14 GW are under construction, with over 10 GW located in states such as Jammu & Kashmir, Arunachal Pradesh, Himachal Pradesh and Assam.

Additionally, five pumped storage projects (PSPs) with a combined capacity of 6 GW are under construction. With the Tehri and Pinnapuram PSPs nearing completion, 2.2 GW of this capacity is expected to be added to the grid in 2024-25. Currently, the operational PSP capacity in India stands at 3.3 GW, with over 60 GW of projects at various stages of survey and investigation, according to Renewable Watch Research.

While large hydropower continues to play a key role in India’s renewable energy mix, the total installed capacity of small hydropower (SHP) projects (below 25 MW) remains at 5.07 GW, as of September 30, 2024. With an estimated potential of around 20,000 MW, SHP remains largely untapped. The majority of these installations are located in hilly states such as Arunachal Pradesh, Himachal Pradesh, Jammu & Kashmir, and Uttarakhand, which together account for nearly half of the total potential.

Policy updates

Policy updates

The Indian hydropower sector witnessed significant progress in August 2023, when 12 stalled hydropower projects with a cumulative capacity of over 11.5 GW were handed over to central PSUs. These projects, located in Arunachal Pradesh, are of high strategic importance to India as China is also reportedly constructing dams on its side of the Brahmaputra, posing a threat of flash floods and water scarcity for India.

In October 2023, the Ministry of Power implemented a uniform renewable energy tariff, creating a source-wise standardised pricing system for renewable energy procurement, in an effort to make it simpler for distribution companies and open access consumers to purchase power through a centralised pool system. In the same month, the CEA introduced comprehensive Slope Stability Guidelines for hydropower projects. These technical specifications outline mandatory requirements for geological surveys, construction methodologies, and monitoring systems in hilly terrains, directly addressing safety concerns that have historically plagued hydropower projects.

For pumped storage, the government announced plans for a comprehensive PSP policy in the union budget of July 2024, aimed at facilitating the smooth integration of renewable energy. This builds on the policy framework introduced in April 2023, which includes measures such as no upfront premium for project allocation, simplified approval processes, monetary benefits such as reimbursement of state goods and services tax and stamp duty, no obligation to supply free power to the home state, and eligibility to participate in the hydropower purchase obligation market.

In August 2024, the central government announced Rs 41 billion in equity support to the north-eastern states for hydropower development. To be implemented from FY 2024-25 to FY 2031-32, the scheme would support the addition of a cumulative hydropower capacity of 15 GW. In another development, the month of September 2024 marked a major financial milestone when the union cabinet approved a

In August 2024, the central government announced Rs 41 billion in equity support to the north-eastern states for hydropower development. To be implemented from FY 2024-25 to FY 2031-32, the scheme would support the addition of a cumulative hydropower capacity of 15 GW. In another development, the month of September 2024 marked a major financial milestone when the union cabinet approved a

Rs 125 billion budgetary support scheme for developing hydropower projects totalling 31,350 MW in capacity. A cumulative PSP capacity of 15,000 MW will also be supported under the scheme. Rather than funding the power plants themselves, the money will be allocated for essential components such as access roads, bridges, transmission lines, and communication systems. Additionally, the government extended the interstate transmission system charges waiver for hydropower plants, in turn, reducing the operational costs for project developers and making hydropower investments more financially attractive and viable in the long term.

While there is no central government policy for the SHP segment, different states have developed their own policies to encourage such projects. For instance, Himachal Pradesh, Uttarakhand, Madhya Pradesh, Karnataka, Sikkim, Assam, and Jammu & Kashmir all offer financial incentives, streamlined approval processes, and measures to encourage local participation. Tamil Nadu also released its small hydro projects policy earlier in August 2024.

Challenges and future outlook

The sector faces a number of challenges. Many projects are experiencing significant delays due to land acquisition and resettlement issues. The Dikhu hydro electric project (HEP) remains stalled at the land acquisition stage, while Luhri HEP Stage-I faces local opposition over rehabilitation matters. Cost overruns pose another major challenge, exemplified by the Subansiri Lower 2,000 MW HEP, where costs have more than tripled since initiation. Natural calamities have increased insurance premiums by 20-50 per cent, further straining project economics. Environmental concerns and complex geological uncertainties continue to delay several projects, including the 1,200 MW Yerravaram PSP and the 2,100 MW Patgaon PSP. Furthermore, over six projects with over 600 MW cumulative capacity are held up due to sub judice matters and fund constraints.

Going forward, India has set ambitious growth targets for the sector. The National Electricity Plan, 2023, for instance, envisions adding 10,814 MW of conventional hydro and 2,700 MW of PSPs by 2027, followed by an additional 9,982 MW of hydro and 19,240 MW of PSPs by 2032. The country’s pumped storage requirements are projected to reach 7 GW by 2027, expanding to 27 GW by 2032, and ultimately reaching 90 GW by 2047. These expansions will require substantial investments, estimated at Rs 542 billion for 2022-27 and Rs 752 billion for 2027-32.

Success in achieving these targets will depend on effectively addressing the sector’s challenges while maintaining the current momentum in policy support and investment. The focus must remain on streamlining clearance processes, enhancing project viability, and strengthening risk mitigation measures. As India pursues its clean energy goals, the hydropower sector’s development remains crucial for ensuring grid stability and energy security in a renewable-rich future.