Renewable energy sources such as solar and wind are crucial for India’s shift to cleaner power. However, their intermittency presents new challenges for grid operators. One solution for grid operators to address this issue is to transfer the risk of managing this variability to renewable energy producers themselves. This has resulted in the development of round-the-clock (RTC), hybrid and firm and dispatchable renewable energy (FDRE) projects. The agreements for these projects require renewable energy providers to deliver power in a way that closely matches demand patterns, significantly increasing the complexity and challenges of renewable energy projects. This article provides an overview of the recent developments in the RTC space, challenges faced by the developers and the future outlook…

Renewable energy sources such as solar and wind are crucial for India’s shift to cleaner power. However, their intermittency presents new challenges for grid operators. One solution for grid operators to address this issue is to transfer the risk of managing this variability to renewable energy producers themselves. This has resulted in the development of round-the-clock (RTC), hybrid and firm and dispatchable renewable energy (FDRE) projects. The agreements for these projects require renewable energy providers to deliver power in a way that closely matches demand patterns, significantly increasing the complexity and challenges of renewable energy projects. This article provides an overview of the recent developments in the RTC space, challenges faced by the developers and the future outlook…

Recent policy and industry developments

Recognising the importance of RTC renewables, the Indian government has implemented several policies to promote their adoption. For the procurement of RTC power from grid-connected renewable projects, the guidelines were issued in July 2020 and later amended in November 2020, February 2021 and February 2022. In June 2023, the Ministry of Power also issued guidelines for the procurement of firm and dispatchable power from grid-connected renewable energy projects with energy storage systems. These guidelines aim to enable discoms to procure FDE, coupled with energy storage, through tariff-based competitive bidding. They provide a framework for power purchase agreements for RTC supply, creating a structured approach for project development and implementation.

The government has also set renewable purchase obligations (RPOs) targets for discoms to fulfil their RPOs not just by procuring standalone renewable energy, but also by using a mix of sources, including hybrid or RTC renewable options. This not only promotes the adoption of renewable energy but also creates a demand for RTC power, driving investment in the sector. To further encourage the development of RTC projects, the government has waived inter-state transmission system charges for renewable energy projects, including those with storage components. This reduces the overall cost of RTC power, making it more competitive with conventional sources.

Several companies in India are also taking the lead in developing and implementing RTC renewable, FDRE and hybrid projects, demonstrating growing interest and investment in the sector. Many tender developments have occurred at both central and state levels in this space.

In May 2020, the Solar Energy Corporation of India Limited (SECI) conducted its 400 MW RTC-1 tender, which discovered the lowest tariff of Rs 2.90 per kWh, with a 3 per cent annual escalation for the first 15 years of the 25-year PPA, leading to an effective tariff of Rs 3.59 per kWh. ReNew Solar Power Private Limited secured the entire capacity. As per the bid conditions, the developer was mandated to fulfil an annual and monthly minimum capacity utilisation factor (CUF) requirement of 80 per cent and 70 per cent respectively.

RTC-2 auction took place in October 2021 for 2,500 MW of renewable-plus-thermal capacity, with Hindustan Thermal Projects winning 250 MW by quoting the lowest (L1) tariff of Rs 3.01 per kWh. Under this tender, the tariff structure was partially fixed and partially variable. The annual CUF requirement was set at 85 per cent, with a peak hour duration of four hours. The penalty provision was 400 per cent of the applicable tariff.

Before the RTC-1 and RTC-2 auctions, SECI had issued a 1.2 GW tender for renewable-plus-storage projects with guaranteed peak power supply. The auction, held in January 2020, saw Greenko and ReNew Power secure 900 MW and 300 MW with peak tariffs of Rs 6.12 per kWh and Rs 6.85 per kWh respectively, and an off-peak tariff of Rs 2.88 per kWh.

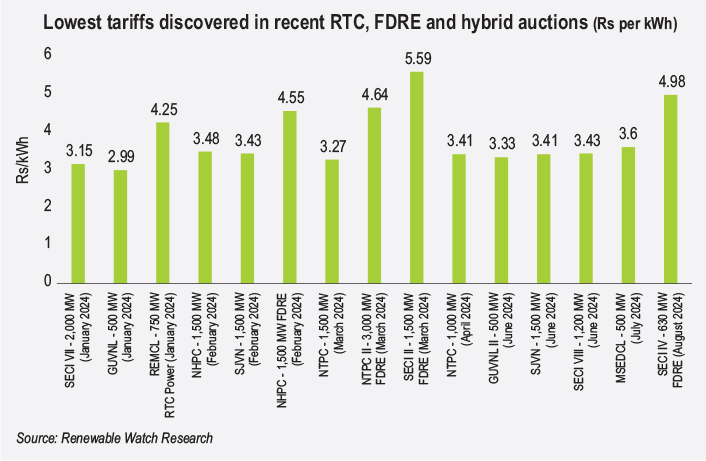

SECI released another tender with assured peak power supply in April 2023 for 1,200 MW of solar-wind hybrid with energy storage, under Tranche VI, where the discovered tariffs ranged from Rs 4.64Rs 4.73 per kWh. In April 2023, Railway Energy Management Company Limited (REMCL) issued a tender for 1 GW of RTC renewables, with or without storage, revealing an L1 tariff of Rs 3.99 per kWh. In January 2024, REMCL also auctioned 750 MW of RTC renewable projects achieving an L1 tariff of Rs 4.25 per kWh.

Since January 2024, several FDRE auctions have been conducted by NTPC Limited, SECI and NHPC Limited, where the L1 tariff ranged from Rs 4.55-Rs 5.59 per kWh. The tender name and lowest tariffs have been mentioned in the graph.

Challenges

Despite the promising potential of RTC renewables, the sector faces several significant challenges. The most pressing issue is the higher cost of RTC projects compared to standalone solar or wind projects due to the inclusion of storage systems. Recent RTC, FDRE and hybrid auctions from January 2024 to August 2024 have seen tariffs in the range of Rs 4.25-Rs 5.5 per kWh (details in the graph), compared to Rs 2.5-Rs 2.7 per kWh for standalone solar projects and Rs 3.42-Rs 3.6 per kWh for standalone wind tariffs in the same period. This price difference highlights the additional costs associated with providing consistent, RTC renewable energy. The issue of expensive RTC power raises questions about the willingness of discoms to buy RTC power to meet their peak power demand, especially as they are obligated to pay fixed costs for thermal power. This reluctance could potentially slow down the adoption of RTC renewables.

At Renewable Watch’s Solar Power in India conference, R.P. Gupta, chairman and managing director, SECI, shared his perspective on the cost viability of RTC renewables. He highlighted that currently, the cost of thermal power from new plants is nearly on par with the prices in the RTC and FDRE tenders. However, while these renewable energy tariffs are fixed for 25-30 years, the cost of thermal electricity from the same plants is expected to rise over time. He added that SECI has not been able to convince states that if they compare RTC and FDRE tariffs with those of new thermal power plants, they will find that integrating renewable energy is more cost-effective.

Although the cost of hybrid or RTC power might appear high at present, standard solar and wind generation face significant fluctuations and variability in energy production. Moreover, when transmission charges are added on a per kWh basis for standalone solar or wind, the overall cost becomes too high. Therefore, RTC renewable energy is the way forward. In fact, RTC power, with a tariff of Rs 4.50 per kWh — which includes the battery component — is certainly feasible when compared to wind, solar or even conventional power sources.

A key concern has been that in the past, the cost of storage has not reduced as was anticipated due to several reasons, including supply chain disruptions caused by the Covid-19 pandemic, which resulted in expensive RTC power. This trend is expected to change, given that storage prices are now showing a downward trajectory. However, several challenges persist regarding integrating storage solutions with renewable projects, including technology selection and project location. Furthermore, to meet RTC demands, developers are building oversized renewable energy plants which also leads to potential energy curtailment during peak production periods and increases overall project costs.

Transmission and connectivity is another challenge. As RTC plants are often set up at multiple locations to harness different renewable sources, ensuring transmission connectivity becomes a significant hurdle. This dispersed nature of projects adds to the complexity and cost of grid integration. Furthermore, financing RTC projects can be difficult due to the higher costs and perceived risks associated with newer technologies.

Future outlook

Going forward, the uptake of green hydrogen in India has the potential to be a significant driver for the adoption of RTC renewable energy solutions. Green hydrogen itself serves as a form of energy storage. It is emerging as a viable storage option to avoid the curtailment of excess renewables. Industries that adopt green hydrogen as a feedstock or fuel will require a stable, RTC supply of renewable energy to ensure consistent hydrogen production. This demand naturally drives the development of RTC renewable energy solutions.

Earlier this year, the Central Electricity Authority (CEA) released a report titled “Techno-Economic Analysis of Renewable Energy-Round the Clock (RE-RTC) Supply for Achieving India’s 500 GW Non-Fossil Fuel-Based Capacity Target by 2030”, which highlighted that the decreasing cost of energy storage is making renewable RTC power increasingly cost-effective and has the potential to attract more developers to bidding processes and lower tariffs. It suggested that research and development for the rapid adoption of storage technology should be prioritised, with the government offering viability gap funding for green hydrogen storage projects in the initial phase to support renewable RTC projects. Further, a policy and regulatory framework for the broad implementation of renewable RTC should be developed.

In conclusion, while challenges remain, particularly in terms of costs and technological integration, the combination of supportive government policies, private sector initiatives and synergies with emerging sectors such as green hydrogen is creating a favourable environment for the growth of RTC renewables in India. As these projects become more prevalent, they have the potential to transform India’s energy landscape, reducing carbon emissions and enhancing energy security.

By Preeti Wadhwa