By Debmalya Sen, Lead – Advanced Energy Solutions, World Economic Forum

By Debmalya Sen, Lead – Advanced Energy Solutions, World Economic Forum

India has set for itself the ambitious targets of meeting 50 per cent of its energy demand using renewable sources and achieving 500 GW of non-fossil fuel capacity by 2030. Under India’s current energy mix, 75 per cent of the country’s energy requirement is met by coal, while only 13 per cent is met by renewables, which increases to 21 per cent when hydro is included. As per the Central Electricity Agency’s National Electricity Plan, the share of renewables is expected to reach 44 per cent (hydro included) by 2031-32, and that of coal to fall to 50 per cent. However, renewables alone will not be able to sustain such a grid. There is a need to integrate 47 GW of battery storage capacity and 26 GW of pumped hydro capacity with the grid to help renewables emerge as a reliable resource.

India’s efforts to bolster renewable energy deployment through a series of policy and regulatory enablers have shown results. The deployment of renewables, specifically solar, has been noteworthy. But the journey from here to 2030 will be much more demanding. If India is to achieve its 2030 targets, it will require 292 GW of solar and 100 GW of wind capacity, up from the present capacities of 90 GW and 47 GW respectively (as of August 2024). This will require a minimum installation of 42 GW every year till 2030. In order to make this happen, renewables need to be made despatchable and more accountable as a resource. To this end, the government introduced the concept of round-the-clock (RTC) renewables in 2018 and subsequently released pertinent competitive bidding guidelines. Since then, the concept of RTC has gone through a series of refinements, each making the definition more stringent.

India’s efforts to bolster renewable energy deployment through a series of policy and regulatory enablers have shown results. The deployment of renewables, specifically solar, has been noteworthy. But the journey from here to 2030 will be much more demanding. If India is to achieve its 2030 targets, it will require 292 GW of solar and 100 GW of wind capacity, up from the present capacities of 90 GW and 47 GW respectively (as of August 2024). This will require a minimum installation of 42 GW every year till 2030. In order to make this happen, renewables need to be made despatchable and more accountable as a resource. To this end, the government introduced the concept of round-the-clock (RTC) renewables in 2018 and subsequently released pertinent competitive bidding guidelines. Since then, the concept of RTC has gone through a series of refinements, each making the definition more stringent.

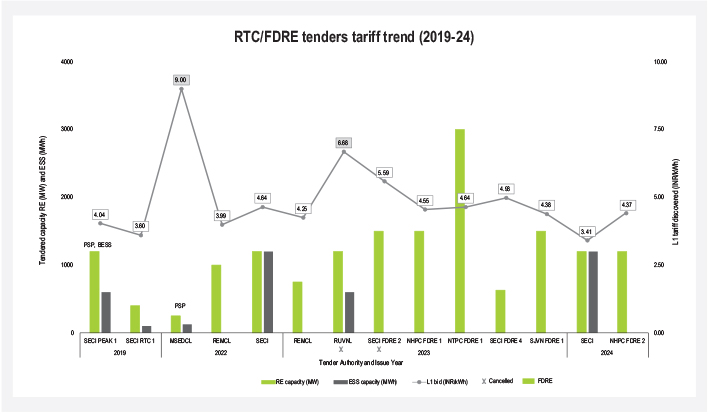

The first competitive bid tender for the RTC concept was released by Solar Energy Corporation of India Limited (SECI) in 2018, where the requirement was to supply 400 MW of renewable power at an 80 per cent annual capacity utilisation factor (CUF) while also meeting a monthly CUF of 70 per cent, with penalties in place for not doing so. ReNew won that tender at a first-year tariff of Rs 2.9 per kWh. The project is being readied for commissioning at the time of writing. Since then, under the aegis of RTC, various tender nodal agencies have issued 24 such tenders, of which 11 are in various stages of execution, five are in the open tendering stage and eight stand cancelled. Through the years, a lot of combinations have been tried in this domain, including thermal plus renewables, which unfortunately did not find traction amongst developers. The initial tenders, apart from three that were modelled on renewable plus thermal, majorly focused on peak availability – initially with a two-part tariff (peak and off-peak) structure, which was eventually replaced with a single tariff requirement. The tariffs discovered in these tenders hovered around Rs 4.5 per kWh. Finally, in 2023, the concept of RTC was amended to the more holistic and well-defined one of firm and despatchable renewables (FDRE). As of August 2024, 13 (16.4 GW), FDRE tenders have been issued by various nodal agencies, of which five (3.8 GW) are at the open tendering stage, four (4.8 GW) have been awarded, one (1.2 GW) is under execution and three (4.6 GW) have

The first competitive bid tender for the RTC concept was released by Solar Energy Corporation of India Limited (SECI) in 2018, where the requirement was to supply 400 MW of renewable power at an 80 per cent annual capacity utilisation factor (CUF) while also meeting a monthly CUF of 70 per cent, with penalties in place for not doing so. ReNew won that tender at a first-year tariff of Rs 2.9 per kWh. The project is being readied for commissioning at the time of writing. Since then, under the aegis of RTC, various tender nodal agencies have issued 24 such tenders, of which 11 are in various stages of execution, five are in the open tendering stage and eight stand cancelled. Through the years, a lot of combinations have been tried in this domain, including thermal plus renewables, which unfortunately did not find traction amongst developers. The initial tenders, apart from three that were modelled on renewable plus thermal, majorly focused on peak availability – initially with a two-part tariff (peak and off-peak) structure, which was eventually replaced with a single tariff requirement. The tariffs discovered in these tenders hovered around Rs 4.5 per kWh. Finally, in 2023, the concept of RTC was amended to the more holistic and well-defined one of firm and despatchable renewables (FDRE). As of August 2024, 13 (16.4 GW), FDRE tenders have been issued by various nodal agencies, of which five (3.8 GW) are at the open tendering stage, four (4.8 GW) have been awarded, one (1.2 GW) is under execution and three (4.6 GW) have

been cancelled.

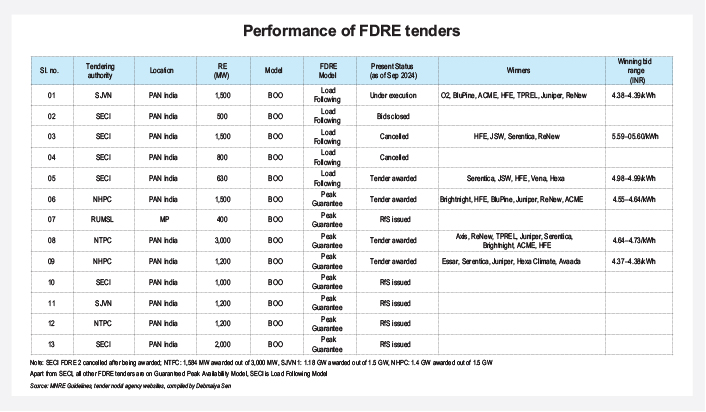

FDRE, as a concept, promotes two major subcategories of tenders. The first is the assured peak availability model, which resembles the RTC concept of meeting peak requirements for two to four hours daily at a higher availability metric (80 per cent), with this metric being increased to 90-95 per cent for FDRE. The second is the load following model – a new addition to the erstwhile RTC concept, which initially required developers to meet a defined load profile throughout the day on a 15-minute interval basis at a high adherence metric of 90 per cent. Till date, this model has come the closest to attaining 100 per cent RTC renewable energy. As it had a stricter adherence requirement, it also came with a premium. SECI has been the only tendering body to promote this model, through five tenders with a cumulative capacity of 4.4 GW as of August 2024. While a great concept, besides pre-identified procurers, it has not been able to find much success, with only one tender (FDRE 4, 630 MW) being successfully awarded till date, one (FDRE 2, 1,500 MW) being cancelled after being awarded, and one (FDRE 3, 800 MW) being cancelled before bidding. The failure to secure a buyer for FDRE 2, which saw a price discovery of Rs 5.59 per kWh, necessitated the relaxation of certain criteria. The adherence metric was reduced from 90 per cent to 75 per cent and the frequency of accounting was relaxed from 15-minute blocks to hourly matching. These amendments helped to facilitate a lower price discovery of Rs 4.98 per kWh in FDRE 4. While 100 per cent RTC renewable energy remains the goal, it needs to be achieved in a phased manner.

FDRE, as a concept, promotes two major subcategories of tenders. The first is the assured peak availability model, which resembles the RTC concept of meeting peak requirements for two to four hours daily at a higher availability metric (80 per cent), with this metric being increased to 90-95 per cent for FDRE. The second is the load following model – a new addition to the erstwhile RTC concept, which initially required developers to meet a defined load profile throughout the day on a 15-minute interval basis at a high adherence metric of 90 per cent. Till date, this model has come the closest to attaining 100 per cent RTC renewable energy. As it had a stricter adherence requirement, it also came with a premium. SECI has been the only tendering body to promote this model, through five tenders with a cumulative capacity of 4.4 GW as of August 2024. While a great concept, besides pre-identified procurers, it has not been able to find much success, with only one tender (FDRE 4, 630 MW) being successfully awarded till date, one (FDRE 2, 1,500 MW) being cancelled after being awarded, and one (FDRE 3, 800 MW) being cancelled before bidding. The failure to secure a buyer for FDRE 2, which saw a price discovery of Rs 5.59 per kWh, necessitated the relaxation of certain criteria. The adherence metric was reduced from 90 per cent to 75 per cent and the frequency of accounting was relaxed from 15-minute blocks to hourly matching. These amendments helped to facilitate a lower price discovery of Rs 4.98 per kWh in FDRE 4. While 100 per cent RTC renewable energy remains the goal, it needs to be achieved in a phased manner.

The assured peak availability model, however, has a strike rate of 100 per cent till date, across all relevant tenders issued by various nodal agencies. Since June 2023, when the FDRE concept was introduced, eight of the 13 FDRE tenders have been for this model. The tariffs discovered in these tenders were in the range of

Rs 4.37–Rs 4.72 per kWh.

It is expected that, the load following model will, over time, gain more importance and viability, with storage costs expected to fall, thus improving the business case for such tenders. There has also been a growing interest in solar plus storage tenders. Globally, storage integration projects have always been more inclined towards solar photovoltaics than renewable hybrids. India took a different route – in the initial years, storage-linked tenders relied completely on the renewable hybrid plus energy storage system (ESS) combination. Solar plus battery ESS (BESS) saw greater uptake among EPC projects with smaller capacities. The first large-scale solar plus BESS project (100 MW solar with 120 MWh BESS), located in Chhattisgarh, was awarded by SECI in 2020 on an EPC basis and commissioned earlier this year. The first build, own, operate tender for solar plus ESS came in 2024, with a head-turning tariff discovery of Rs 3.41 per kWh.

Since then, in a period of three months, two more tenders have been shared promoting solar plus storage. The first was from SECI for a 2 GW solar plus 4 GWh ESS project, followed by SJVN’s 1.2 GW solar plus 2.4 GWh ESS capacity. It should be kept in mind that this cannot be compared with the FDRE concept, as it does not address RTC power. The sector has been seeing a lot of innovation, necessitating that the guidelines made for promoting renewables be amended on a regular basis. What seemed appropriate two years ago may not be optimal today, with technology parameters improving over time. The prime example of this is batteries, which have been going through their own innovation journey resulting not only in reduced costs but also significant improvements in technology parameters. Overall, with an ambitious target ahead of us, the pace of deployment of renewables plus storage needs to be ramped up further in the coming years. With technological improvements and better price discoveries, the sector demands all our attention. In the days ahead, we will keep witnessing innovations in tenders and new concepts being floated by various tendering agencies.