India is well endowed with solar and wind energy sources. But standalone, plain vanilla solar and wind projects are not enough to meet the round-the-clock (RTC) power requirements of consumers given the intermittency issues. However, when coupled, hybrid or integrated renewable energy projects can offset the intermittency challenge, especially when combined with energy storage solutions such as battery energy or pumped hydro.

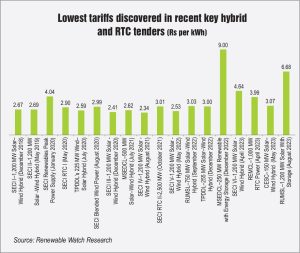

Moreover, recent tariffs discovered under hybrid project auctions have been highly competitive with standalone renewable energy tariffs. This has attracted the interest of investors and the government to this space. Over the past few years, the number of hybrid or RTC project tenders and auctions has been increasing. This year, the lowest hybrid tariff discovered was Rs 3.07 per kWh in CESC’s 150 MW solar-wind hybrid auction in May 2023.

Several recent policy developments are also giving a helping hand. The Ministry of Power (MoP) has announced amendments to the July 2020 guidelines for tariff-based competitive bidding for procuring RTC power from grid-connected renewable energy projects. Earlier, the Ministry of New and Renewable Energy’s National Wind-Solar Hybrid Policy and several such state policies had initiated a policy push for this segment.

Role of energy storage systems

For renewable energy to become despatchable and available 24×7, energy storage systems (ESSs) need to play a key role. ESSs maintain the dynamic system of balancing energy supply and demand, and enable a more flexible and reliable grid system. They can help improve power quality, reduce peak demand, increase the capacity of distribution and transmission grids, avoid deviation penalties, and increase the overall flexibility of the system. Renewable energy developers and utilities are currently the key adopters of energy storage and are announcing many projects in this space.

Recently, the MoP announced the National Framework for Promoting Energy Storage Systems. The initiative aligns with the country’s commitment to employ renewable energy sources and reduce greenhouse gas emissions. The main goals of this framework are to encourage the deployment of ESSs while reducing the reliance on fossil fuel power plants, ensure a steady supply of RTC renewable energy, reduce emissions, and minimise energy costs. Additionally, it aims to promote innovation in energy storage technologies, enable fair access to energy storage for all segments of the population, and improve grid stability and dependability through the deployment of ESSs. Furthermore, its objective is to use policy and regulatory measures, financial and fiscal incentives, and performance-based incentives to assist in the development and installation of ESSs.

The framework provides several policy measures and incentives, such as estimated requirements for energy storage, a waiver of interstate transmission system fees for ESS use, rules for BESS power procurement, and the inclusion of ESS in the infrastructure harmonised master list. It intends to offer stakeholders a resource to help them comprehend the government’s strategy for energy storage and its importance in India’s energy transformation.

There have been other key government interventions in this space in recent months. In Union Budget 2023-24, there were provisions for viability gap funding (VGF) support for BESS. The VGF could be up to 40 per cent of the capital cost of the project, with the condition that the project must be commissioned within 18-24 months.

In addition, India has announced energy storage obligations (ESOs). The prescribed ESO is 1 per cent in 2023-24, which will go up to 4 per cent by 2029-30. The MoP has also notified guidelines for the utilisation of BESSs as a part of generation, transmission and distribution assets, along with ancillary services. Bidding guidelines have also been notified.

In addition, India has announced energy storage obligations (ESOs). The prescribed ESO is 1 per cent in 2023-24, which will go up to 4 per cent by 2029-30. The MoP has also notified guidelines for the utilisation of BESSs as a part of generation, transmission and distribution assets, along with ancillary services. Bidding guidelines have also been notified.

With regard to the legal status of ESSs, the Electricity (Amendment) Rules, 2022 notified that an ESS can be used independently or in combination with generation, transmission and distribution infrastructure, and an ESS has to be considered a part of the power system.

The guidelines for competitive bidding of renewable energy with energy storage have also been announced. The aim of the guidelines is to ensure a consistent and predictable supply of renewable energy to distribution firms while addressing the intermittent nature of renewable energy and transmission system underutilisation.

Within the energy storage space, the focus has shifted to pumped storage projects (PSPs) given the significant industry and government interest in this area. Inter-state transmission charges have been waived for hydro pumped storage projects and BESS projects. The complete waiver of ISTS charges for PSP projects is now linked to the date of award rather than the date of commissioning. This will be applicable to projects where construction work is granted on or before June 30, 2025.

The central government is also providing budgetary support for construction of roads and bridges by hydropower project developers, including PSPs, of up to Rs 15 million per MW for projects up to 200 MW and up to Rs 10 million per MW for projects above 200 MW.

In April 2023, the MoP issued guidelines for overseeing and fostering the growth of PSPs. The ministry has additionally envisioned tax exemptions and involvement of the power markets to enhance the financial viability and appeal of these projects for both developers and investors. Furthermore, several state-level initiatives, such as by Madhya Pradesh and Andhra Pradesh, are expected to give a fillip to the PSP segment.

The Central Electricity Authority (CEA) has notified that the total installed PSP capacity in India is 4,745.6 MW. According to the CEA, it is estimated that India will require at least 26.7 GW of pumped storage hydropower capacity to support the projected integration of wind and solar into the grid by 2032. The CEA estimates that India has the potential to deploy 114 PSPs with a total capacity of 123.95 GW across different parts of the country.

Currently, Maharashtra, Andhra Pradesh and Rajasthan are the states with the largest pipeline of PSPs. The southern belt contributes a significant portion of the project pipeline, followed by the western region. According to Renewable Watch Research, projects of over 70 GW capacity have been announced, around 36 GW of capacity is under permitting, 7 GW is under construction and 4 GW is under bidding.

Integrated renewable energy and storage projects

With the growing interest in ESS and specifically PSPs, the concept of integrated renewable energy storage projects (IRESPs), that is, co-location of different renewable energy projects such as solar and wind along with PSPs, is emerging. Such projects provide RTC power based on customer requirements; solve intermittency challenges; provide grid stability, demand management and ancillary services; and reduce renewable curtailment.

With the growing interest in ESS and specifically PSPs, the concept of integrated renewable energy storage projects (IRESPs), that is, co-location of different renewable energy projects such as solar and wind along with PSPs, is emerging. Such projects provide RTC power based on customer requirements; solve intermittency challenges; provide grid stability, demand management and ancillary services; and reduce renewable curtailment.

According to Greenko’s estimates, the weighted average cost of energy from storage and directly from generation for an IRESP is Rs 4-Rs 4.50 per unit. While the perunit range of cost for IRESPs is lower than that for coal, gas and large hydro, it is higher than that for standalone renewables currently. Meanwhile, the capex of Greenko’s 1,200 MW Pinnapuram IRESP in Andhra Pradesh and Saundatti IRESP in Karnataka is Rs 55 billion and Rs 55.35 billion respectively.

Future outlook

With respect to storage requirements, the CEA has estimated that by 2026-27, 16.13 GW of ESS capacity will be needed to integrate additional renewable energy capacity, with significant expansion expected in the coming years. The government’s dedication to advancing energy storage technology is demonstrated by the considerable funding demand for PSPs and BESSs for the period 2022-27, standing at Rs 542.03 billion and Rs 566.47 billion respectively. By 2047, the need for energy storage is anticipated to rise to 320 GW, which includes 90 GW of PSP and 230 GW of BESS capacity, with a storage capacity of 2,380 GWh.

As per the CEA’s latest Optimal Mix Report for 2029-30, the energy storage capacity required in India in 2029-30 is likely to be 60.63 GW (18.98 GW PSP and 41.65 GW BESS), with a storage capacity of 336.4 GWh (128.15 GWh from PSP and 208.25 GWh from BESS).

Location-specific hydro and PSP projects totalling 638 MW and 11,460 MW respectively, which have been either concurred by the CEA or are at the survey and investigation stage, are likely to yield benefits by 2029-30. In addition to the 1,580 MW of PSP capacity that is currently under construction, a PSP capacity of 11,460 MW is required till 2030 to meet the electricity storage requirements of the country. The total funding requirement for PSPs from 2022-23 to 2030-31 is Rs 1,294.43 billion.

According to a recent report by Goldman Sachs titled “India Clean Energy: Balancing Growth with Decarbonisation”, the country’s levellised cost of RTC renewable power is 27 per cent lower than that of China. Furthermore, a higher return profile for PSP-backed RTC renewable energy, that is, 20-25 per cent equity internal rate of return vis-à-vis 13-15 per cent for solar and coal, can structurally improve the business model of utilities. The report estimates that PSP-backed RTC renewable power costs only 15-17 per cent more than new pithead coal plants. The cost premium will, however, be negligible after factoring in the transmission cost waiver and the expected inflation in coal and coal logistics costs. Despite the high initial cost premium, pumped hydro-backed RTC renewable power supply earns 1.5-2 times returns compared to plain vanilla solar and cost-plus coal plants.

Moreover, given that grid tariffs for commercial and industrial customers are higher than RTC renewable costs across most states, there is economic sense for the segment to purchase RTC renewables. There is a potential of around 300 GW for corporates to shift to net zero compliance and economically viable RTC renewable energy supply, according to the report. This presents a unique opportunity for India compared to other large economies. For instance, the report estimates RTC renewable energy viability in China only closer to 2030 despite the country being self-sufficient in renewable energy components and batteries. In addition, according to the report’s estimates, there will be a demand for approximately 600 GWh of storage by financial year 2032, but India will meet only around 80 per cent of it even in an optimistic scenario. Therefore, India may need to add approximately 23 GW of coal capacity – 50 per cent higher than the government’s target.

While the policy push to promote RTC power is impressive, some issues and concerns have been highlighted by several sector stakeholders. One, the high cost of energy storage implies that its use will be minimal and the focus will primarily be on renewables and thermal power in RTC tenders. Two, supply chain disruptions, duties and taxes applicable on solar components, and an increase in input costs may hike the cost of solar and renewable energy projects. This puts a question mark on whether the discoms will be willing to buy it. Three, there are concerns regarding the complicated nature of rules and provisions for RTC tenders, making the task of the developer tedious and prone to stringent penalties. Four, forecasting and scheduling become a cumbersome tasks for such projects.

These issues notwithstanding, RTC projects clubbed with ESS are the future of India’s clean energy landscape. In fact, corporates have started demanding RTC power from developers, and the latter have initiated plans to deliver it through different business models. Going forward, one can expect investor focus to align further with the government’s push towards hybrid and RTC green energy projects to meet India’s commitment for reducing carbon emissions and greening the grid.

By Sarthak Takyar