As the country’s energy sector moves towards surplus capacity and the share of renewable energy grows, there is a need to redesign the energy market to optimise power procurement costs. The majority (about 90 per cent) of the power procurement in the country is through inflexible long-duration power purchase agreements (PPAs) as well as self-scheduling, which creates system inefficiencies and leads to suboptimal capacity utilisation. To facilitate energy transition and ensure optimum capacity utilisation, deepening of the short-term power market as well as the introduction of a capacity market are imperative.

Recently, a group constituted by the Ministry of Power (MoP) for “Development of Electricity Market in India” proposed comprehensive solutions to address the key issues in the country’s electricity market design, such as the dominance of inflexible long-term contracts, the lack of resource adequacy planning at the centre and in the states, and the high reliance on self-scheduling by states. It proposed solutions to encourage market participation for renewables, ensure a well-developed ancillary services market, and reduce system inefficiencies through low reliance on self-scheduling. The solutions are aimed at creating an efficient, optimal and reliable market framework to enable the energy transition and integration of renewable energy into the grid.

Renewable Watch examines the key issues and challenges outlined in the report as well as the solutions proposed for an electricity market redesign…

Need for redesigning electricity markets

The Indian electricity market is dominated by inflexible and long-duration (about 25 years) PPAs. Although market-based mechanisms, power exchanges and bilateral trading came into existence in 2008, these have typically reflected about 5-6 per cent of the day-ahead electricity procurement over the past five years. The discoms depend on self-scheduling for almost 90 per cent of their power requirements. The lack of a uniform framework/nationally coordinated approach for power procurement leads to suboptimal despatch, with cheaper plants in the national merit order not being scheduled to their full available capacity.

Although renewable energy is establishing itself as a significant source of power generation, it continues to be procured primarily through longer-duration and inflexible contracts. International experience indicates that renewables and the associated balancing energy sources are best integrated through market-linked mechanisms. An increase in renewable energy in the overall energy mix will require a robust market-based platform to encourage new investments and to enable balancing of variability in the grid by harnessing the diversity that the market offers.

India has diversity in demand patterns and resource availability. The seasonal variation in demand provides scope for implementing a capacity market in the country, which is not supported by the current market framework and operating procedures. Further, although India has integrated all its regions into a synchronous grid, the current wholesale power market continues to operate in silos, leaving significant untapp-ed opportunities for optimisation and achieving a national merit order.

Resource adequacy (RA) planning has been absent from the country’s electricity market operations. RA, which requires maintaining sufficient reserve margins to absorb demand and supply fluctuations, has become all the more important with larger volumes of renewable energy being integrated into the grid. Coordinated national- and discom-level RA planning is needed to maintain optimal generation capacity while minimising the costs. Introducing capacity markets and ushering in larger reforms such as market-based economic despatch (MBED) and contracting of renewables through the market are needed for RA planning. The RA assessment at a discom level needs to take granular time block-wise probabilistic estimates of generation availability and despatch to arrive at the need for additional contracts, sans which discoms are likely to either over- or under-contract, leading to reliability iss-ues or higher costs to consumers.

Resource adequacy (RA) planning has been absent from the country’s electricity market operations. RA, which requires maintaining sufficient reserve margins to absorb demand and supply fluctuations, has become all the more important with larger volumes of renewable energy being integrated into the grid. Coordinated national- and discom-level RA planning is needed to maintain optimal generation capacity while minimising the costs. Introducing capacity markets and ushering in larger reforms such as market-based economic despatch (MBED) and contracting of renewables through the market are needed for RA planning. The RA assessment at a discom level needs to take granular time block-wise probabilistic estimates of generation availability and despatch to arrive at the need for additional contracts, sans which discoms are likely to either over- or under-contract, leading to reliability iss-ues or higher costs to consumers.

Roadmap for electricity market reforms

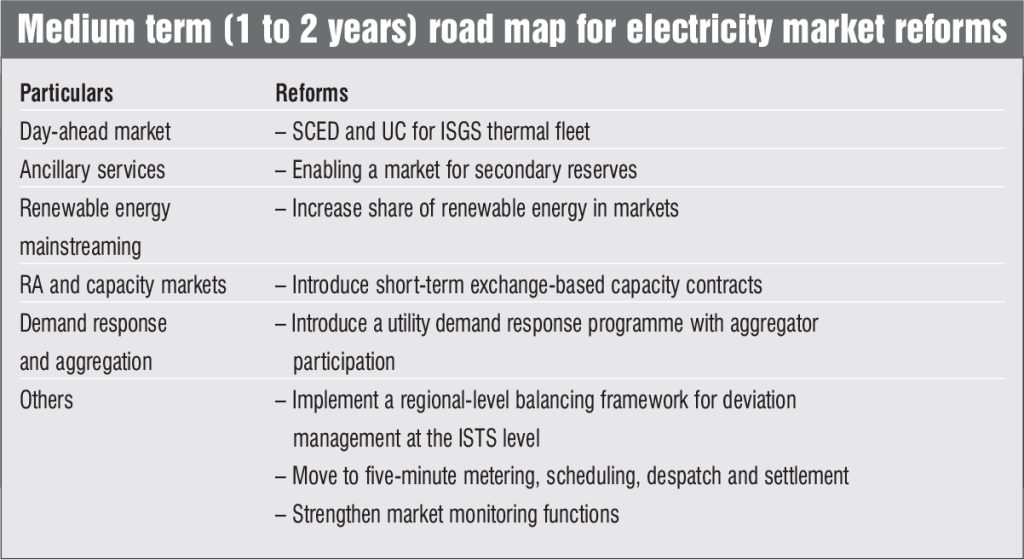

RA and capacity contracting: In order to address the concerns regarding RA planning as the Central Electricity Authority (CEA) RA framework gets rolled out in 2023, there is a need to introduce a framework for capacity markets. Since the requirements of the states vary on a temporal and pan-Indian basis, standardised seasonal/monthly contracts and custom bilateral contracts could be introduced.

For the short-term capacity market, to begin with, the group recommends introducing a capacity market through an e-bidding portal, which would facilitate two-part tariff-based bidding (fixed charges and variable charges). Under this, discoms could also put up their surplus capacity for sale. Subsequently, standardised exchange-based contracts for trading of capacity, where discoms can participate as sellers of surplus capacity and buyers for deficit, could be introduced.

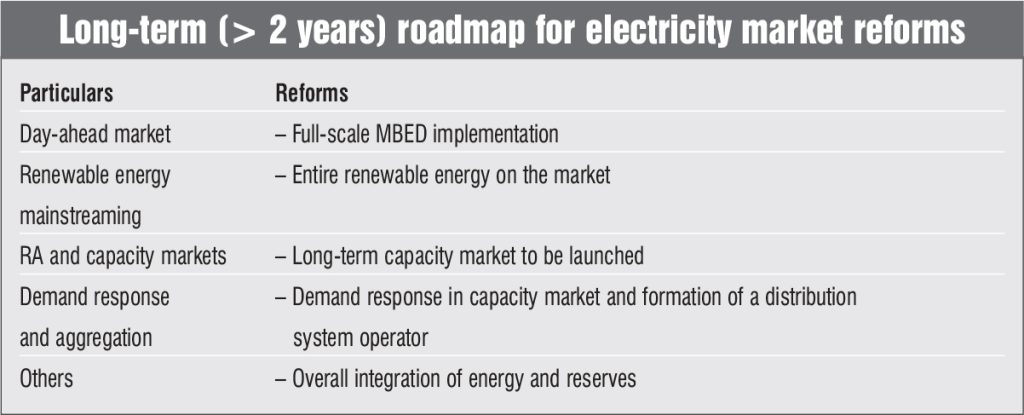

For a long-term capacity market, until MBED is implemented, discoms could, auction bilateral contracts of 12-15 years duration by inviting a capacity bid and an energy bid (with a bilateral contract settlement [BCS] mechanism). Meanwhile, with the implementation of MBED, new bilateral auctions will have energy price discovery on the exchange, without BCS.

Enhancing the efficiency of the day-ahead market: The inflexibility aspect of self-scheduling within state control areas restricts the sharing of reserves across states as well as the extent to which variable renewable energy can be deployed within the state’s boundaries. Market-based scheduling and despatch will enlarge the balancing area from the state’s boundaries to regional/national boundaries and bring in the desired flexibility to deploy higher volumes of renewable energy with greater reliability.

Enhancing the efficiency of the day-ahead market: The inflexibility aspect of self-scheduling within state control areas restricts the sharing of reserves across states as well as the extent to which variable renewable energy can be deployed within the state’s boundaries. Market-based scheduling and despatch will enlarge the balancing area from the state’s boundaries to regional/national boundaries and bring in the desired flexibility to deploy higher volumes of renewable energy with greater reliability.

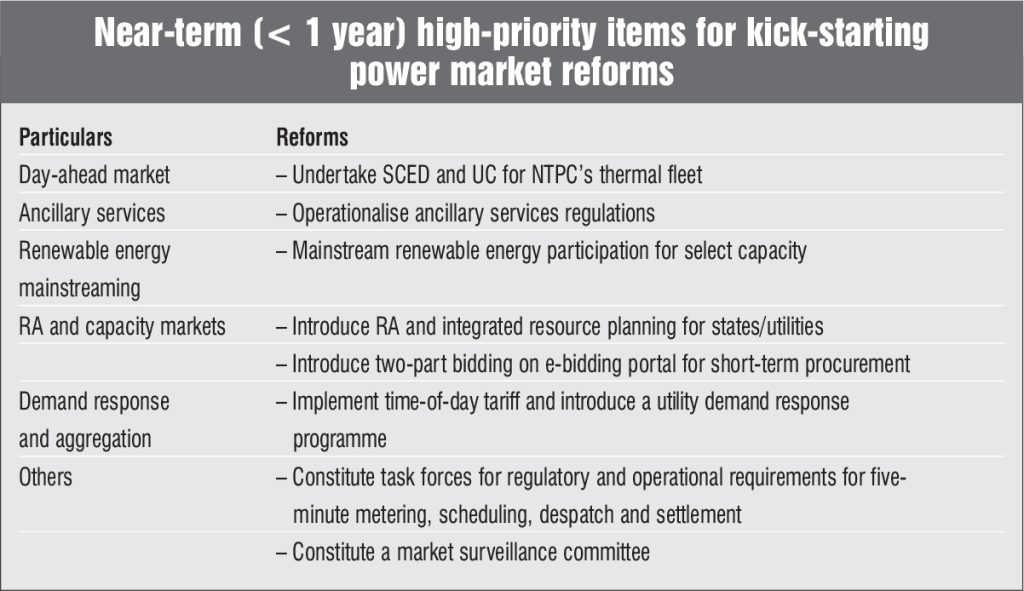

In order to enhance the efficiency of the day-ahead market, the group recommends that the Grid Controller of India should initiate security constrained economic despatch (SCED) with unit commitment (UC) on a D-1/D-3 basis for various categories of thermal stations. This could be taken up first for the thermal fleet of NTPC and then gradually expanded to the interstate generating station (ISGS) thermal fleet. Later, the entire ISGS fleet as well as merchant capacities would be mandated to participate in the day-ahead market.

Renewable energy participation in the day-ahead market: In order to promote renewable energy participation in the day-ahead market, the group recommends introducing a single strike price option for a 15-year PPA initially, to gain investor confidence and ensure bankability. Other variants could be introduced subsequently. Apart from this, the group recommends that 20 per cent of the required renewable energy capacity be procured through market-based BCS mechanisms, while the remaining 80 per cent could be procured by discoms. While for established renewable energy technologies, the BCS model with adequate funding support could be adopted, for new renewable energy technologies (such as offshore wind), adequate revenue protection is needed.

Market-based mechanism for secondary reserves: In Phase I, the group recommends operationalising the Central Electricity Regulatory Commission (CERC) ancillary services regulation for administered procurement of secondary reserves. Meanwhile, in Phase II, market-based procurement of secondary reserves could be introduced. In terms of the implementation framework, the group recommends introducing a uniform product for secondary frequency regulation. A participation factor, based on ramping capability, cost and available headroom, could be considered for despatching the available stack of resources. Such a factor would inherently give preference to fast responding sources since they can provide better regulation performance than traditional sources. Further, resources should be paid availability charges as they reserve some of their capacity for ancillary services instead of participating in energy markets. To begin with, ancillary and energy can be independent markets as co-optimisation requires a single bidding framework for energy and ancillary. Going forward, co-optimisation of energy and ancillary services can bring optimisation in system costs.

Market-based mechanism for secondary reserves: In Phase I, the group recommends operationalising the Central Electricity Regulatory Commission (CERC) ancillary services regulation for administered procurement of secondary reserves. Meanwhile, in Phase II, market-based procurement of secondary reserves could be introduced. In terms of the implementation framework, the group recommends introducing a uniform product for secondary frequency regulation. A participation factor, based on ramping capability, cost and available headroom, could be considered for despatching the available stack of resources. Such a factor would inherently give preference to fast responding sources since they can provide better regulation performance than traditional sources. Further, resources should be paid availability charges as they reserve some of their capacity for ancillary services instead of participating in energy markets. To begin with, ancillary and energy can be independent markets as co-optimisation requires a single bidding framework for energy and ancillary. Going forward, co-optimisation of energy and ancillary services can bring optimisation in system costs.

Financial instruments for electricity markets

At present, the Indian electricity market does not have financial instruments through which market participants can hedge against price risks. While this is largely attributable to the dominance of long-term PPAs for power procurement, as the volumes on the power exchanges increase, financial instruments for electricity will be imperative. In one of its reports, the IEEFA notes that the spot market on the power exchanges and the derivatives market will feed into each other. It will be a virtuous cycle wherein the derivatives market will establish forward prices, more participants will shift from PPAs to exchanges, thereby increasing liquidity in derivatives and subsequently increasing liquidity in the spot market on the power exchanges and vice versa.

At present, the Indian electricity market does not have financial instruments through which market participants can hedge against price risks. While this is largely attributable to the dominance of long-term PPAs for power procurement, as the volumes on the power exchanges increase, financial instruments for electricity will be imperative. In one of its reports, the IEEFA notes that the spot market on the power exchanges and the derivatives market will feed into each other. It will be a virtuous cycle wherein the derivatives market will establish forward prices, more participants will shift from PPAs to exchanges, thereby increasing liquidity in derivatives and subsequently increasing liquidity in the spot market on the power exchanges and vice versa.

In order to operationalise financial instruments in the electricity market, the Securities and Exchange Board of India (SEBI) and the CERC have reached an understanding to allow futures trading in electricity. It has been agreed that the former will oversee the functioning of all financially traded electricity forwards while the latter will regulate physically settled forward/ futures where electricity is delivered at a future date at the contracted price. With regard to the future roadmap for the introduction of financial instruments in the electricity market, the report on electricity market development notes that there is a need for coordination between the electricity and the financial regulator to formulate market rules for the monitoring and surveillance of derivatives transactions. The financial regulator needs to assess when to introduce such products. Events such as increasing liquidity and price volatility could be the signals to watch.

Conclusion

The MoP’s efforts to redesign the electricity market are well timed and are much needed to meet the emerging requirements of the power sector. Once implemented, the various recommendations of the MoP group will go a long way in making the country’s energy market more dynamic in nature, while catalysing the energy transition and optimising power procurement costs.

By Priyanka Kwatra