As of September 2022, India had installed 41 GW of onshore wind energy, significantly short of its 60 GW target to be achieved by this year. Over the past few years, it has been observed that the wind energy segment has received lesser policy and investor attention vis-à-vis the solar power space, which has expanded at an impressive pace. Emerging areas such as e-mobility, green hydrogen and battery storage are also increasingly taking centre stage with respect to capital inflow, policy orientation and investor interest. Nonetheless, utilising wind energy effectively is integral to achieving India’s ambitious clean energy goals and the year 2022 has seen significant progress in this regard with the commencement and completion of several auctions and deals. The offshore wind segment is also set to take off with the much-awaited draft tender released for a 4 GW project in Tamil Nadu. Moreover, the policy side also witnessed greater activity this year, with the announcement of the renewable purchase obligation (RPO) trajectory for the wind and the draft wind repowering policy.

Renewable Watch presents key developments in this space in the past year – projects and tenders, financing deals, policy initiatives, tariffs as well as the future outlook…

Projects and tenders

According to the Global Wind Energy Council India, between 2017 and 2021, the Solar Energy Corporation of India (SECI) tendered 3.5 GW of yearly wind capacity on an average (excluding hybrid bids). Moreover, 1.6 GW of the annual wind-solar hybrid/round-the-clock (RTC) capacity was auctioned on an average between 2018 and 2021. However, to meet the 70 GW onshore wind target by 2030, 8-10 GW of yearly tender capacity will be needed between 2022 and 2029. Moving along this direction, the wind energy segment has seen the emergence of several key projects and auctions in the past one year. These include:

- In December 2021, Ayana Renewable Power Six awarded a contract to Siemens Gamesa to deliver turbines for a 302 MW wind farm project in Karnataka. Under the agreement, Siemens Gamesa will supply and install 84 units of its SG 3.6-145 wind turbines. The project is planned to be built in Karnataka’s Gadag district.

- In the same month, Honda Motorcycle & Scooter India (HMSI) announced the commissioning of second wind turbine system in Bhanvad, Gujarat, while Maharashtra State Electricity Distribution Company Limited (MSEDCL) also floated separate tenders to procure 342 MW of energy from grid-connected intra-state wind projects and 300 MW from interstate and intra-state wind projects.

- In January 2022, SECI floated a tender for the development of 1,200 MW of interstate transmission system (ISTS)-connected wind generation plants in India (Tranche XIII). NTPC Renewable Energy, a wholly owned subsidiary of NTPC Limited, also issued a request for proposal (RfP) for the development package (balance of system with land) of ISTS-connected wind energy projects with a capacity of up to 720 MW to be implemented throughout the country.

- In February 2022, Tata Power announced a partnership with RWE Renewable GmbH of Germany to explore the potential for joint development of offshore wind projects in India.

- NTPC Renewable Energy Limited, in March 2022, invited expressions of interest for shortlisting eligible land banks and parcels in Rajasthan, Maharashtra, Gujarat, Tamil Nadu, Karnataka, Andhra Pradesh and Madhya Pradesh to set up wind energy projects.

- In April 2022, Envision Energy, a Chinese provider of wind turbines and energy management software, received a 2 GW wind turbine order in India. As per the company’s statement, all 596 wind turbines will be manufactured in Envision’s India factory and will be delivered by the end of 2023.

- In May 2022, the winners of SECI’s auction (Tranche XII) for the 1.2 GW ISTS-connected wind power projects were announced. These included NTPC Renewable Energy Limited, Halvad Renewables (EDF Renewables), JSW Neo Energy and Torrent Power.

- In the same month, MSEDCL also issued an RFP for 325 MW of power from intra-state wind projects. MSEDCL set a ceiling tariff of Rs 2.65 per kWh for the tender.

- In June 2022, Siemens Gamesa received an order from Vena Energy to deliver wind turbines for a 133 MW wind project in Karnataka. The turbines would be manufactured at Siemens Gamesa’s facilities in India and installation work at the site is slated to begin in 2023.

- ReNew Power also signed definitive agreements to acquire more than 500 MW of operating wind and solar assets. The acquisition would reportedly comprise operating wind assets totalling 471.65 MW.

- In June 2022, the Gujarat State Electricity Corporation Limited (GSECL) also issued RfP for engineering, supply, procurement, installation and commissioning of 100 MW of wind power at two locations on a turnkey basis.

- Gujarat Urja Vikas Nigam Limited’s (GUVNL’s) auction to purchase power from 500 MW of grid-connected wind power projects (Phase III) was completed in July 2022. The declared winners were GSECL, Rajpur Renewables (EDF Renewables), Juniper Green Energy, Solarcraft Power India 3 (BluPine Energy), TEQ Green Power XII (O2 Power), ACME Pokhran Solar and Project Twelve Renewable Power (Ayana Renewable Power). The tender was issued in May 2022.

- In July 2022, SECI also issued a letter of award to Torrent Power for the development of a 300 MW wind energy project in Karnataka at a tariff of Rs 2.94 per kWh.

- In August 2022, Siemens Gamesa Renewable Power won a contract from Azure Power Global to supply onshore wind turbines for a 346 MW wind power project. In accordance with the agreement, Siemens Gamesa will provide 96 of its onshore SG 3.6-145 wind turbines to Azure Power for use in Karnataka.

- Inox Wind also secured an order from NTPC Renewable Energy Limited for setting up a 200 MW wind power project. The project will be completed on a turnkey basis at the Dayapar site in Gujarat’s Kutch district and is expected to be operational by January 2024.

- In September 2022, Inox Wind’s 3.3 MW wind project was successfully commissioned in Ranparda village, Rajkot district. In the same month, Adani Green Energy Limited commissioned a 325 MW wind energy plant in Madhya Pradesh’s Dhar district. The plant will be supervised by the Adani Group’s Energy Network Operation Centre that will help in providing technological assistance.

- The Aditya Birla Group awarded KP Energy a Rs 2.22 billion contract to develop wind energy projects. The projects will be established at the Bhungar and Fulsar sites in Mahuva, Bhavnagar, Gujarat.

- In October 2022, GUVNL floated bids for 300 MW of grid-connected wind power projects (Phase IV) with an additional 300 MW greenshoe option. The minimum bid capacity under the tender for intra-state projects and interstate projects will be 25 MW and 50 MW respectively.

- In the same month, INKEL, a public-private partnership venture promoted by the Kerala government, floated an empanelment tender to develop 14 MW of wind power projects in Palakkad district of Kerala.

- Recently, in November 2022, Adani New Industries Limited reported the installation of India’s largest wind turbine generator in Mundra, Gujarat. The wind turbine stands 200 metres tall and can generate about 5.2 MW of electricity and can be used to power approximately 4,000 homes.

Tariff trends

The switch from the feed-in tariff regime to the reverse auction system in India has lowered the tariffs for wind projects. However, these tariffs continue to be relatively higher than those discovered in solar and wind-solar hybrid auctions. In July 2022, among the winners of GUVNL’s auction for 500 MW of grid-connected wind power projects (Phase III), GSECL offered the lowest tariff at Rs 2.84 per kWh followed by EDF Renewables at Rs 2.98 per kWh. In May 2022, NTPC renewables, Halvad Renewables, JSW Neo Energy and Torrent Power won SECI’s auction for the 1.2 GW ISTS-connected wind power projects (Tranche XII). NTPC Renewables quoted a tariff of Rs 2.89 per kWh, while the rest quoted Rs 2.94 per kWh.

The lowest tariff of 2021 was discovered in SECI’s auction for 1,200 MW of ISTS-connected wind power projects (Tranche XI) in September 2021. ReNew Power, Green Infra Wind Energy and Anupavan Renewables won capacities of 300 MW, 180 MW and 150 MW, respectively at a quoted tariff of Rs 2.69 per kWh. The tariff was roughly 2.9 per cent lower than the lowest tariff discovered in SECI’s previous auction of 1,200 MW of ISTS-connected wind projects (Tranche X), held in March 2021, in which Adani Renewable Energy, which won 300 MW of capacity, had quoted a tariff of Rs 2.77 per kWh. The highest bid over the past one year was quoted by Ayana, which secured 140 MW of the 200 MW bid capacity at Rs 3.27 per kWh in GUVNL’s 500 MW auction completed in July 2022.

Key financings

Unlike the solar segment and other emerging segments such as green hydrogen, the wind energy segment witnessed limited number of financing developments over the past year. The year primarily saw two key financing deals in the wind energy segment. In August 2022, Inox Wind’s board approved to raise up to Rs 8 billion by issuing 0.01 per cent non-convertible non-cumulative participating redeemable preference shares of a face value of Rs 10 each of the company. The funds raised through the issuance will be used inter-alia for repayment of debt.

The second key deal in the said period was Torrent Power’s acquisition of a 100 per cent stake in Wind Two Renergy Private Limited (WTRPL) from Inox Green Energy Services for Rs 325.1 million. The company purchased 32,510,000 equity shares of WTRPL at a face value of Rs 10 each. This acquisition is part of Torrent’s strategy to attain sustainable growth through renewable energy. All in all, the wind segment demands much greater investment than it has received over the past few years. Amid the government’s rising policy push with the recent wind RPO trajectory and the draft policy for offshore wind leasing, one can expect greater capital inflow, domestic and international, in India’s wind segment over the coming year.

Policy developments

The year has seen substantial initiatives from the government to revive the wind energy segment. In October 2022, the Ministry of New and Renewable Energy (MNRE) released a draft for the National Repowering Policy for Wind Power Projects, 2022. A “Policy for Repowering of Wind Power Projects” was issued by the ministry in August 2016 in order to create a participatory framework for repowering. A revised policy has now been drafted, taking into account feedback from various stakeholders and subsequent discussions. The objectives of this new policy include optimum utilisation of wind energy resources by maximising energy yield per square km of the project area and utilising the latest state-of-the-art onshore wind turbine technologies. The policy also lays out conditions for developers to opt for repowering of their old wind turbines. A monitoring and advisory committee by the name of Wind Repowering Committee will be appointed by the ministry, in accordance with the provisions of this policy, to assist the MNRE in the implementation of the Repowering Policy.

No significant progress was made in the offshore wind segment until 2021. However, earlier this year, the Union Minister for Power and New and Renewable Energy announced at a meeting on transmission planning for offshore wind energy projects in India that bids for offshore wind energy blocks of 4 GW would be issued every year for the next three years. The reports suggested that bids for development off the coasts of Tamil Nadu and Gujarat for power sale through open access/captive/bilateral third-party sale/ merchant sale over a period of three years will begin with the current financial year (2022–23). Following that, 5 GW of capacity will be bid out every year for the next five years, up to and including financial year 2029-30. Consequently, in November 2022, the MNRE issued a draft tender to select wind power developers for leasing seabed areas to develop 4 GW of offshore wind power projects off the coast of Tamil Nadu. The scope of the tender includes grid connectivity, long-term open access and access to the grid under the general network access framework.

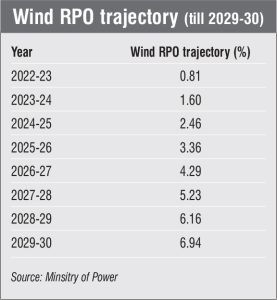

In July 2022, the Power Ministry released the RPO and energy storage obligation trajectory till 2029-30. According to this order, the total prescribed RPO will progressively increase from 24.61 per cent in 2022-23 to 43.33 per cent by 2029-30. This includes wind RPO, which will increase from 0.81 per cent to 6.94 per cent during the period under consideration. The success of the scheme will depend on how effectively the wind RPO is implemented by states.

In March 2022, the MNRE granted an additional three-month time extension in the scheduled commissioning date of wind power projects, accounting for delays due to supply chain disruptions caused post Covid as well as monsoon-related disruptions. Moreover, to promote clean and renewable energy, the Union Minister of Power and New and Renewable Energy recently launched the Green Energy Open Access portal, which allows any consumer with a connected load of 100 kW or above to be eligible for renewable energy through open access from any renewable energy generating plant set up by self or by any developer. The government has also indicated a possible reversal in the procurement policy from e-reverse auctions to feed-in tariffs or closed bidding. Closed bidding is planned in four to five wind states, with an annual bid size of 8 GW. The discovered tariff will be bundled and sold to distribution companies. However, there is no formal order or notification issued from the ministry on these lines.

Outlook

At present, the wind segment faces many challenges in terms of cost escalation, delays in completing power purchase and power sale agreements and competition from cheaper alternatives such as solar power. Moreover, issues pertaining to land acquisition and allocation, long project timelines and other supply chain bottlenecks are also prominent. However, with recent developments in terms of the repowering policy, wind RPOs and draft offshore leasing tender, it seems the segment is finally receiving the policy attention that it warrants.

By Kasvi Singh