India’s renewable energy deployments crossed 110 GW in June 2022, an impressive doubling of capacity from 58 GW in June 2017. This is the result of several factors including a supportive policy regime, a transparent competitive bidding process, an enthusiastic private sector and, most importantly, the increasing cost competitiveness of renewable energy, especially solar power and wind power.

Solar power tariffs in India witnessed a steep decline, from Rs 3 per kWh in February 2017 to record low tariffs of Rs 1.99 per kWh in December 2020, and are now at sub-Rs 2.50 per unit levels. Meanwhile, wind power tariffs have dropped to sub-Rs 3 per unit levels. On a global scale as well, renewable energy tariffs have declined significantly. A report from July 2022 titled “Renewable Power Generation Costs in 2021” by the International Renewable Energy Agency (IRENA) estimates that between 2010 and 2021, the global weighted average levellised cost of energy fell by 88 per cent for newly commissioned utility-scale solar PV projects and 68 per cent for onshore wind projects.

However, the global supply chain disruptions, which were triggered by the pandemic, have now escalated owing to the Russia-Ukraine conflict and threaten to derail the progress of the sector. The prices of essential raw materials such as polysilicon, steel, copper and aluminium have increased due to the supply shortage. There is a dearth of oil and gas in many countries while fuel prices are rising. Meanwhile, logistics costs have increased sharply. As these developments are unfolding on a global scale, no industry and no country is immune to this. The Indian renewable energy sector is also facing the impact of these disturbances with delays in project implementation and rise in tariffs.

Will these disruptions slow down India’s energy transition? Or will these be short-term hiccups and the country’s renewable energy sector come out unaffected through this storm? In this article, we aim to answer these questions by assessing the global supply chain and price disruptions in essential raw materials and oil and gas, dependency of the Indian industry on these supply routes and expected impact on the country’s renewable energy deployments…

Disruptions in supplies and prices

Rewind to early 2020 when the entire world went into lockdown mode as the Covid-19 pandemic wreaked havoc across nations. Factories stopped operations, import-export and movement of manpower and cargo were restricted, and project development across all sectors including renewables virtually came to a standstill. While the government categorised renewable energy as essential activity permitting construction work in this space, equipment and manpower shortage, and logistical concerns made this a challenging task. The successive waves of the pandemic further complicated the situation, especially as the production of raw materials and other critical equipment remains concentrated in a few countries and is limited to a few players.

As governments contemplated a green recovery from the pandemic with a greater role for clean energy, the Russia-Ukraine conflict began in February 2022. Russia, a major exporter of oil and gas as well as other important metals and minerals, is now under heavy sanctions. Meanwhile, the supply of other essential commodities from Ukraine has been impacted. The oil and gas markets are in turmoil, and energy and fuel prices have spiked, affecting the metal industry output and shipping costs. The conflict has been raging for five months, adding to the logistical and commodity market disruptions.

The cost of raw materials is also fluctuating, thus impacting future project price visibility. According to IRENA, the prices of various important commodities have increased significantly between January 2019 and May 2022. For instance, steel is used in the construction of towers, nacelles and various mechanical equipment in wind power projects and in foundations and mounting systems in solar PV plants. Iron ore, which is essential for steel production, witnessed a surge of 187 per cent between January 2019 and June 2021. Although the prices have dropped since then, they were still 87 per cent higher in May 2022 when compared to January 2019. Another important metal used for wiring and cabling in power plants is copper, which has witnessed a price increase of 55 per cent between January 2019 and May 2022. Aluminium, mainly used in solar PV plants and wind turbines, witnessed an increase of 50 per cent between January 2019 and May 2022. However, the price was 84 per cent higher in March 2022.

Apart from these metals, polysilicon supplies have been hit hard. It is one of the major raw materials in the solar PV space, used for making solar cells and modules. There was an oversupply of polysilicon pre-pandemic, which led manufacturers to slow down production during the pandemic. With the reopening of markets, and developers and solar cell and module manufacturers rapidly trying to make up for lost time, the demand for polysilicon suddenly surged. This led to supply shortages and a hike in polysilicon prices. For instance, according to IRENA, polysilicon prices were around $9 per kg in early 2020, whereas the average cost increased to around $33 per kg between January 2022 and May 2022. Even after accounting for module efficiency and manufacturing improvements, there has been an overall increase of $0.043 per watt in the cost of polysilicon for solar PV cells between 2019 and 2022.

The surging fossil fuel prices and freight costs have also contributed to the high metal prices. According to the International Energy Agency (IEA), freight costs have increased almost fivefold as of March 2022 as compared to early 2021. All these costs are ultimately being passed on by manufacturers as higher equipment costs and therefore project costs are also increasing. The IEA estimates a 15-25 per cent increase in the overall investment costs of new utility-scale wind and solar PV power plants across the world in 2022 as compared to 2020.

Impact on India’s renewable energy sector

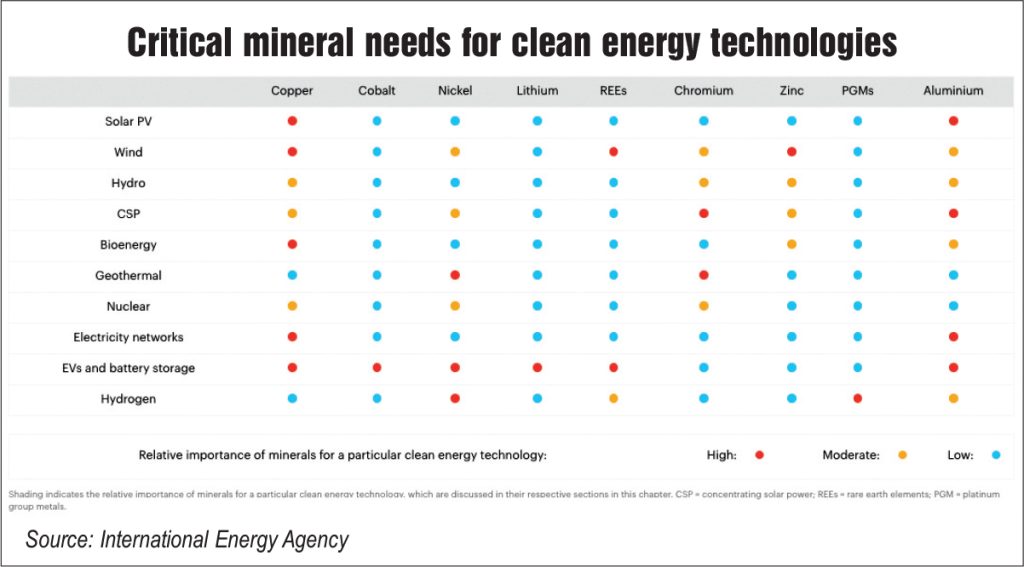

The high dependency of the renewable energy sector on imports for essential materials is likely to impact the planned renewable energy deployments. The domestic wind manufacturing capabilities are well developed and most of the wind turbines deployed in India are produced here. However, wind turbines require various metals like copper, steel, nickel and rare earth elements, and India imports a sizeable volume of these raw materials. Thus, India’s domestic wind industry is not immune to the global geopolitical and supply chain disruptions, and the price volatility of these commodities and the overall currency.

In the solar PV space, there is a direct dependence on imported goods as domestic solar cell and module manufacturing capabilities are insufficient to cater to the massive demand. Traditionally, the Indian solar industry has depended on China and a few other countries for the bulk of its solar cell requirement. The government has been making efforts to reduce the reliance on solar imports in the form of domestic content requirement in tenders, various safeguard and customs duties as well as the production-linked incentive scheme. However, domestic production facilities will take a few years to be set up and reach the required scale. Further, the country will need to build sizeable capacity for polysilicon production to be truly free from import reliance. Till then, the country’s solar import dependence is expected to be significant.

India witnessed the impact of the pandemic first in 2020 and then in 2021, when supply chain disruptions hit the country’s renewable energy industry hard. Due to lockdowns, transport restrictions and manpower unavailability, under-construction projects across the country were delayed. Meanwhile, approvals and permits took longer. The unavailability of spares in many cases made operations and maintenance work difficult.

To ease some difficulties for the industry, the government, in February 2020, announced that the pandemic will be treated as a force majeure event. In August 2020, after various modifications, the Ministry of New and Renewable Energy (MNRE) granted a five-month extension to renewable energy projects under development. The extension was granted for the period from March 25, 2020 to August 24, 2020. This was a blanket extension with no requirement of case-by-case examination and documents of evidence. It applied to developers, original equipment manufacturers, and engineering, procurement and construction companies. However, the MNRE received requests for further extension and in February 2021, it decided that extension beyond these five months can be granted by implementing agencies only in exceptional cases after due diligence and careful consideration of the specific circumstances.

Soon, the second wave of the pandemic started, which was devastating for India. The MNRE announced a timeline extension of about two and a half months for renewable energy projects in light of the second wave of the Covid-19 pandemic. The period of disruption was identified as April 1, 2021 to June 15, 2021. For wind power projects, which face logistical and construction challenges in the movement and erection of heavy machinery during the monsoon months, an additional three-month time extension had to be provided on a case-by-case basis.

The Indian renewable energy sector had already been suffering on account of delays in approvals and transmission and land unavailability, and the pandemic-related disruptions further slowed down capacity additions. Owing to the global restrictions in the last quarter of 2019-20, capacity installations stayed at 9,386 MW and further declined to 7,046 MW in 2020-21 as industries struggled in the new global and economic landscape. The sector surely performed better in 2021-22 as developers rushed to complete their projects and make up for lost time. Consequently, capacity additions went up to 15,452 MW.

This year, 4,179 MW has been installed in the April-June 2022 quarter and if the trend continues, then only 16 GW will be installed by March 2023. As per IEA estimates, India will add about 17 GW each in calendar years 2022 and 2023. These estimates are optimistic as they take into account a large chunk of the capacity that has been delayed due to the pandemic and other reasons and developers for these projects would have placed their equipment supply orders earlier. However, capacity additions would decline if supply chain disruptions and price fluctuations continue, and developers hesitate to buy costlier equipment. Another issue in India is that of price sensitivity. Even if developers are ready to buy expensive equipment, the discoms might not be willing to procure costlier renewable power. As it is, solar and wind power tariffs have increased recently on account of the price volatility in global markets.

Solar tariffs have increased significantly since the record low bid of Rs 1.99 per unit in December 2020 in the Gujarat solar auction. The last solar auction by the Solar Energy Corporation of India (SECI) in February 2022 witnessed a lowest tariff of Rs 2.35 per unit. Meanwhile, Gujarat’s solar auction in March 2022 witnessed lowest bid of Rs 2.29. Tariffs may increase further in the coming months on account of basic customs duty and increasing freight, polysilicon and other commodity prices.

In the wind power space, the lowest tariffs have increased from Rs 2.69 per unit in SECI’s September 2021 auction to Rs 2.89 per unit in its May 2022 auction. In the solar-wind hybrid space as well, the lowest bid price has increased from Rs 2.34 per unit in the August 2021 auction to Rs 2.53 per unit in the latest May 2022 auction. These tariffs may hike further if the global price uncertainties continue.

Outlook

As the Indian renewable energy sector comes to terms with these uncertainties in the global commodity markets and increasing fuel and shipping costs, there are bound to be some challenges in new installations and tariffs. Further, the deteriorating value of the rupee against the dollar is impacting the value of imported goods. Green energy transition is the way forward for the country to be self-reliant and secure in terms of its energy needs. Even though these supply chain disruptions are expected to continue for some time owing to the current global geopolitics and the soaring cost of fossil fuels, which are used in all industries, the renewable energy sector will ride through these short-term challenges and there is likely to be no long-term impact.

To ensure that such issues do not hamper the country’s green energy growth, it is essential to diversify its supply chain routes instead of relying on just a few players and markets. Further, expanding the local manufacturing capabilities is paramount to safeguard the renewable energy industry from any such future events.

By Khushboo Goyal