The installed wind power capacity reached 39.99 GW as of October 31, 2021, around 20 GW short of the 60 GW target for 2022. The leading states for installed wind capacity are Tamil Nadu (9,846.69 MW), Gujarat (8,952.92 MW), Karnataka (5,039.4 MW), Maharashtra (5,012.83 MW), Rajasthan (4,326.82 MW), Andhra Pradesh (4,096.65 MW), Madhya Pradesh (2,519.89 MW), Telangana (128.1 MW) and Kerala (62.5 MW).

Despite slowly growing numbers on paper, the wind power sector does not seem to have recovered from the government’s decision to introduce competitive bidding to ensure transparent discovery of tariff, although criticised for not being done in a phased manner. The knee-jerk decision left wind turbine manufacturers with big inventories and dependence mostly only on centralised power procurement for independent power producers (IPPs). In the market, unviable tariffs started emerging, with players trying to tap the small market pie to use their inventories. Given the low tariffs, an equitable development of wind projects also did not take place, as greater focus was laid only on Gujarat and Tamil Nadu. Land availability concerns in the past, especially in Gujarat, added to the woes of the sector. On top of these concerns are the chronic pain points revolving around payment delays and power curtailment that put a major stress on the sector. The progress in upcoming opportunities in the sector such as offshore wind, repowering and green hydrogen remains quite slow.

The wind power sector does not seem to have recovered from the government’s decision to introduce competitive bidding to ensure transparent discovery of tariff, although criticised for not being done in a phased manner

Renewable Watch presents the key developments in this space in the past year – policy initiatives, auctions, financing deals and turbine orders, as well as the future outlook…

Policy initiatives

There were no major policy initiatives in the past year to promote the wind power sector. During the year, the Ministry of Power announced an extension of the waiver of interstate transmission system (ISTS) charges on the transmission of electricity generated from solar and wind sources. Earlier, the waiver was available to solar and wind projects commissioned up to June 30, 2023. The date has now been extended till June 30, 2025.

On the state side, Maharashtra issued its Unconventional Energy Generation Policy, to promote non-conventional source-based energy generation in January 2021. The state aims to implement 17,360 MW of transmission system-connected renewable power projects by 2025. This includes 2,500 MW of wind energy projects. The policy also aims to set up 50 MW of solar, and wind-based energy storage projects and 50 MW of solar-wind hybrid projects for transmission. In October 2021, Karnataka Renewable Energy Development Limited reissued the Draft Karnataka Renewable Energy Policy, 2021-26 to develop 10 GW of renewable energy projects with and without energy storage. The policy focuses on different markets including stand-alone wind and wind-solar hybrid projects. Offshore wind projects will also be promoted. In the policy, wind projects are allowed 4 acres of land per wind turbine generator.

The progress in upcoming opportunities in the sector such as offshore wind, repowering and green hydrogen remains quite slow

With respect to repowering of onshore wind turbines, a key policy development was the order released by the Tamil Nadu Electricity Regulatory Commission on the procedure to be adopted by Tamil Nadu Generation and Distribution Corporation Limited, for repowering the existing wind electricity generators and the tariff for the same.

The offshore wind space has not witnessed any major breakthrough since the notification of the National Offshore Wind Energy Policy, 2015. In a written reply to a Lok Sabha question in July 2021, the power and new and renewable energy minister stated that post notification of the policy, the National Institute of Wind Energy (NIWE) issued “Guidelines for Offshore Wind Power Assessment Studies and Surveys” to enable private investors to carry out offshore wind resource assessment. The minister further added that the government is carrying out offshore wind resource assessments and related studies through the NIWE, to validate the offshore wind resource potential in identified locations, off the coast of Gujarat and Tamil Nadu. He also mentioned that the ministry has formulated a committee to finalise a roadmap for offshore wind development in the country, including upcoming offshore projects and that the government has permitted foreign direct investment of up to 100 per cent under the automatic route for renewable energy projects, including offshore wind energy projects.

Key auctions and projects

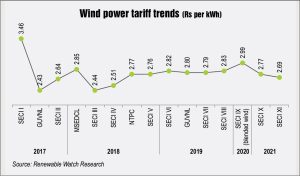

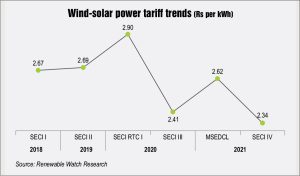

In 2021, the auction activity for stand-alone wind power projects picked up compared to the previous year (a damped year) but was still limited compared to the auction activity in 2018 and 2019. The tariff of stand-alone wind projects has still not crossed the record low of Rs 2.43 per kWh discovered in 2017 (GUVNL). Since 2019, tariffs have been hovering in the range of Rs 2.69-2.83 per kWh, reaching Rs 2.99 per kWh for SECI IX blended wind power auction. The focus seems to have shifted to promoting wind via the solar-wind hybrid and round-the-clock route. For hybrids, 2021 was a highlight with the discovery of record low tariff of Rs 2.34 per kWh for the SECI IV tender. The commercial and industrial segment too seems to be attracted to this, with CleanMax entering the wind-solar hybrid market in the past year, with plans to build about 300 MW of wind-solar hybrid capacity over the next three years.

The SECI auction for 1,200 MW ISTS-connected wind power projects (Tranche XI) took place in September 2021. In the auction, ReNew Power, Green Infra Wind Energy (Sembcorp) and Anupavan Renewables (EverGreen) won a capacity of 300 MW, 180 MW and 150 MW, respectively, at a tariff of Rs 2.69 per kWh. Adani Renewable Energy and Azure Power won 450 MW and 120 MW respectively, at a tariff of Rs 2.70 per kWh.

Earlier, in March 2021, SECI’s auction for developing 1.2 GW of ISTS-connected wind projects (Tranche X) in India took place, in which Adani Renewable Energy won 300 MW of wind projects at the L1 tariff of Rs 2.77 per kWh. Further, Ayana Renewable Power won 300 MW, Evergreen Power won 150 MW and JSW Future Energy won 450 MW, at a tariff of Rs 2.78 per kWh each. JSW had placed bids for 600 MW, but was awarded only 450 MW under the bucket filling method. The auction had received bids for a total of 3.15 GW of projects from 11 developers with tariffs as high as Rs 3.39 per kWh.

The year witnessed a few projects being commissioned. For instance, ReNew Power commissioned a 300 MW wind power project (SECI) in Kutch, Gujarat, and Adani Green Energy Limited (AGEL) commissioned a 100 MW wind power plant in the same region.

Key financing deals

The wind financing market was active with some big asset acquisition and stake sales taking place.

During the year, Japanese financial services company Orix Corporation completed the acquisition of a 21.8 per cent stake in Greenko Energy Holdings for about $961 million. As per the agreement, Orix will also add 873 MW of its wind energy portfolio in India into Greenko’s portfolio in exchange for the shares. The company has also integrated its entire wind power generation business in India into Greenko to acquire additional shares.

Later, in October 2021, one of the biggest financing deals in the sector took place when AGEL completed the acquisition of a 100 per cent stake in SB Energy India from the SoftBank Group and the Bharti Group. SB Energy India’s portfolio consists of operational and under-construction renewable energy assets with a combined capacity of over 4.9 GW, located across four states. About 4.1 GW of capacity comes from utility-scale solar assets, while 450 MW comes from hybrid wind-solar parks and 324 MW from wind farms. In another major development during the year, Actis started the sale process of Sp-rng Energy, a leading developer of solar and wind power projects and finalised Bank of America as the banker to find a prospective buyer.

In March 2021, AGEL raised a $1.35 billion debt package for its under-construction renewable asset portfolio. The revolving project finance facility would initially finance the 1.69 GW portfolio of solar and wind projects to be set up in Rajasthan. Vector Green Energy, a Mumbai-based IPP focused on solar and wind energy, received a Rs 11 billion loan from the Indian Renewable Energy Development Agency.

Wind turbine orders

In the wind turbine space, the most active companies during the past year were GE Renewable Energy, Inox Wind, Vestas, Suzlon and Siemens Gamesa.

GE Renewable Energy made a deal to supply 42 onshore wind turbines for three of CleanMax’s wind hybrid projects. The three projects will have a total capacity of 110 MW and will supply electricity to meet the demands of various industrial companies in the states of Karnataka and Gujarat. The company will supply GE 2.7-132 variety of onshore wind turbines for the projects under a 10-year long-term full service agreement. GE Renewable Energy was also selected by Continuum Green Energy to supply, install and commission a 148.5 MW wind power project in Gujarat. The wind farm in Morjar, Bhuj, will have 55 sets of GE Renewable Energy’s 2.7-132 onshore wind turbines. This wind farm was awarded to Continuum Green Energy by SECI in the Tranche VI auction. During the year, GE Renewable Energy also received an order from JSW Energy to supply 810 MW of onshore wind turbines for their upcoming wind farms in Tamil Nadu, India.

Inox Wind received new orders for the supply and installation of wind turbine generators of 62 MW from IPPs and retail customers. The projects are spread over Gujarat and Karnataka. The company also signed an agreement with Integrum Energy Infrastructure for 92 MW of wind power projects comprising 2 MW turbines. It also won an order for a 150 MW wind power project from NTPC Renewable Energy. As part of the order, the company will supply and install DF 113/92-2.0 MW capacity wind turbine generators.

Vestas too secured a 101 MW order from ReNew Power. The order is an extension of ReNew’s existing project in Kutch, Gujarat, where Vestas had previously supplied turbines totalling 250 MW. Vestas also supplied turbines of 100 MW to another one of ReNew’s projects in Taralkatti, Karnataka, and another 101 MW order from ReNew Power for projects in Gujarat. The company also received a new order from MSPL Limited for its 17 MW Hospet project in Karnataka.

The Suzlon Group secured a new order for the development of a 252 MW wind power project from CLP India (now Apraava Energy). Under this order, it will install 120 units of its S120-140 metre wind turbines. The project is being set up in Sidhpur, Gujarat, and is expected to be commissioned in 2022. The group also announced its new order win for the development of a 252 MW wind power project from CLP India. Suzlon would install 120 units of S120-140m wind turbine generators with a rated capacity of 2.1 MW each. The project is located in Sidhpur, Gujarat, and is expected to be commissioned in 2022.

With tendering activity still being meagre compared to the manufacturing capacity of wind turbine manufacturers (10 GW per annum, which can also be ramped up), manufacturers will continue to look at export markets

Siemens Gamesa launched its SG 3.4-145 wind turbine in the country. The company also signed a second major contract with ReNew Power to supply its turbines to a 322 MW wind project in Tondehal. This follows the release of a 301 MW contract with ReNew for a wind project near Hombal.

Future outlook

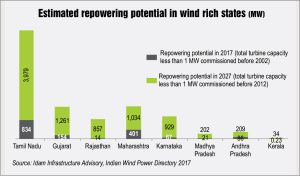

No major headway has been made in the offshore wind power sector. For the 1 GW offshore wind project in the Gulf of Khambat, Gujarat, the ministry had stated that the environmental impact assessment is under way. Still, the 5 GW target for this sector for 2022 seems to be a pipe dream. The focus will now shift to the 30 GW target for 2030. Similarly, no major development took place in the repowering space with different stakeholders only discussing business models, tariffs and turbine technology currently. This is the low-hanging fruit to generate more wind power from the same area of land, leading to lower cost of production and higher utilisation rate. With the use of modern turbines, better grid integration is also possible. Also, modern turbines have a better aesthetic value vis-à-vis fast rotating old turbines. Despite these benefits, the key challenges that are hampering its uptake relate to turbine and landownership, modifications to PPAs, feasibility of evacuation infrastructure, disposal of old turbines and regulatory treatment of additional expenditure.

With tendering activity still being meagre compared to the manufacturing capacity of wind turbine manufacturers (10 GW per annum, which can also be ramped up), manufacturers will continue to look at export markets.

Overall, the wind power segment seems to have suffered neglect. Given India’s climate commitments, it is important that its issues are revisited and the challenges addressed.

By Sarthak Takyar