• This price rise has been mainly driven by a sharp increase in the price of polysilicon, a key input for cell & module manufacturers

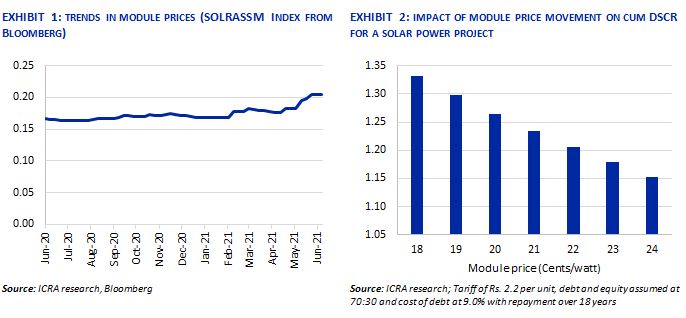

• As PV module component comprises about 50-55% of the overall project cost, such increase in the module price level if sustained, may moderate the debt service coverage metrics for developers by about 12-14 bps

The increase in imported photovoltaic (PV) solar module price level by about 15-20% over the last 4-5 months, to around 22-23 cents/watt as on date, is likely to impact returns of solar power project developers. This price rise has been mainly driven by a sharp increase in the price of polysilicon, a key input for cell & module manufacturers. As per an ICRA note, given the import dependency for PV modules for a majority of the solar power installations in India, such hardening in the price of PV modules, if sustained, remains a near-term headwind. This risk is especially significant for the capacity won by developers through the bidding route over the last six to nine months (amounting to 4-GW ) at tariffs ranging largely between Rs. 2.00 per unit and 2.25 per unit; and scheduled to be commissioned over the next 12-15-month period. This apart, the recent surge in metal prices is also leading to upward pressure on the overall capital cost for solar power projects.

Commenting further, Mr. Girishkumar Kadam, Senior Vice President & Co-Group Head- Corporate ratings, ICRA, said, “Given that the PV module component comprises about 50-55% of the overall project cost, such increase in the module price level by about 4-5 cents/watt if sustained, is likely to moderate the debt service coverage metrics for the project developers by about 12-14 basis points. Alternatively, the tariff increase required to offset such a module price increase is estimated at about 20-22 paise/unit. This, along with the impact of the basic customs duty (BCD) on imported PV modules, is likely to result in the overall bid tariff to increase by about 55-60 paise/unit for the forthcoming auctions. Nonetheless, the solar bid tariff, after factoring in this dual impact, is still likely to remain below Rs. 3/unit.”

As the BCD notification for cells and modules is effective from April 2022 onwards, there remains a possibility for a surge in demand for imported modules, particularly in the fourth quarter of the current fiscal in turn, supporting the elevated price levels for PV modules. In this context, both the module price behaviour and honouring of supply contracts by module OEMs from China in the near term continue to remain key monitorables for the solar power developers.

Further, the registration of module manufactures outside India, in the Approved List of Models and Manufacturers (ALMM) issued by the Ministry of New and Renewable Energy (MNRE), Government of India in March 2021, remained affected due to the lockdown restrictions and procedural requirements so far based on industry sources. As per the notification issued by the MNRE, the projects bid out under the standard-bidding guidelines, post April 10, 2021, are required to procure modules from the approved list. This in turn may pose near-term challenges for the Indian developers for planning the procurement of imported PV modules, especially given the capacity constraints for domestic manufacturers.

Mr. Vikram V, Vice President & Sector Head – Corporate Ratings, ICRA, adds, “As a result, the uncertainty on the timelines for inclusion of module suppliers from China in the ALMM list may affect the incremental bidding activity in the solar power sector. Nonetheless, cumulative solar project awards as on date remains strong at ~28 GW (excluding the capacity pending for signing of PSA/PPAs and including hybrid projects), which provides a healthy visibility on the capacity addition over the medium term.”

Not with standing the near-term headwind related to module price levels, the credit outlook on the solar energy sector remains stable, given the improved tariff competitiveness, supportive regulatory framework through must-run status for these plants, leading to satisfactory operating track record, as well as availability of liquidity buffer (which is mix of debt service reserve account and access to working capital limits) for the issuers rated.

For further information, please contact:

© Copyright, 2021 ICRA Limited. All Rights Reserved.

All information contained herein has been obtained by ICRA from sources believed by it to be accurate and reliable. Although reasonable care has been taken to ensure that the information herein is true, such information is provided ‘as is’ without any warranty of any kind, and ICRA in particular, makes no representation or warranty, express or implied, as to the accuracy, timeliness or completeness of any such information. Also, ICRA or any of its group companies, while publishing or otherwise disseminating other reports may have presented data, analyses and/or opinions that may be inconsistent with the data, analyses and/or opinions presented in this publication. All information contained herein must be construed solely as statements of opinion, and ICRA shall not be liable for any losses incurred by users from any use of this publication or its contents.

Disclaimer:

This Press Release is being transmitted to you for the sole purpose of dissemination through your newspaper/magazine/agency. The Press Release may be used by you in full or in part without changing the meaning or context thereof, but with due credit to ICRA Limited. However, ICRA Limited alone has the sole right of distribution of its Press Releases for consideration or otherwise through any media including, but not limited to, websites and portals.

About ICRA Limited:

ICRA Limited was set up in 1991 by leading financial/investment institutions, commercial banks and financial services companies as an independent and professional investment Information and Credit Rating Agency.Today, ICRA and its subsidiaries together form the ICRA Group of Companies (Group ICRA). ICRA is a Public Limited Company, with its shares listed on the Bombay Stock Exchange and the National Stock Exchange. The international Credit Rating Agency Moody’s Investors Service is ICRA’s largest shareholder.

Click on the icon to visit our social media profiles.