Indian Solar Industry: A bright future beckons

Indian Solar Industry: A bright future beckons

The heavily import-dependent Indian solar industry now sees new dawn: self-reliance. The Hon. Prime Minister’s clarion call for “Atmanirbhar Bharat” has seen a great response in the shape of fresh capacity announcements by leading developers/manufacturers of capacity additions of 10 GW annually. The approach is now widening on the development of an integrated solar eco-system as compared to the previous model of focusing on installed generation capacity for market creation.

With a projected investment of US$ 120 Billion in 300GW of solar projects by 2030, India is presenting a great opportunity to gain self-reliance by thinking beyond manufacturing just cells/modules and focus instead on creating the entire eco-system by manufacturing all components like solar glass, EVA, junction boxes, etc.

Growth of Indian Solar Market and a huge dependence on imports:

With Solar tariffs reaching below Rs. 2/ kWh, solar energy is now the cheapest source of energy. The installed solar generation capacity has reached 38 GW in India and Government has ambitious plans of reaching 100 GW by 2022 and 300 GW by 2030. Despite the challenge in achieving the target of 100 GW by 2022, it does offer a huge growth opportunity for all the stakeholders across the value chain including developers, financial institutions, EPC contractors, module, and component manufacturers.

India currently has around 11 GW of solar module manufacturing capacity, which is seeing a low capacity utilization of about 40%, by virtue of about 50% of all solar installations being done using fully made solar modules imported from China.

Based on the policy announcement by the Hon. Prime Minister, nearly 12 GW of fresh module manufacturing capacity has been announced. With installed manufacturing capacity rising to 23 GW in near future, module manufacturing is likely to rise to 17-18 GW annually by FY25. However, there is a huge dependence on imports for the critical components that are required to manufacture the modules i.e. solar cells, back sheets, solar glass. E.g. The present domestic manufacturing capacity for solar cells is only 3 GW, for solar glass is only 2.5 GW. Nearly 40-45% of back sheet requirement is met through imports from China despite the extant 8-9 GW of domestic manufacturing capacity for backsheet. For the past four financial years (FY17, FY18, FY19, and FY20) the total value of the country’s solar imports was $3.2 Bn, $3.8 Bn, $2.2 Bn, and $1.67 Bn respectively. The creation of a robust domestic solar manufacturing ecosystem in India would not only reduce the dependence on an undependable supplier but also save a large chunk of valuable foreign exchange.

From the perspective of solar glass manufacturing, If the Government’s solar capacity addition target is to be met with a vision of self-reliance, solar glass capacity will need to rise to 17.5 GW annually by 2025. To achieve this volume of production, an additional investment of around USD 500 Mn (Rs 3,750 crores) will be required. This will help India achieve import substitution of around US$ 340 Mn annually by FY25.

Creation of a robust solar manufacturing ecosystem in India:

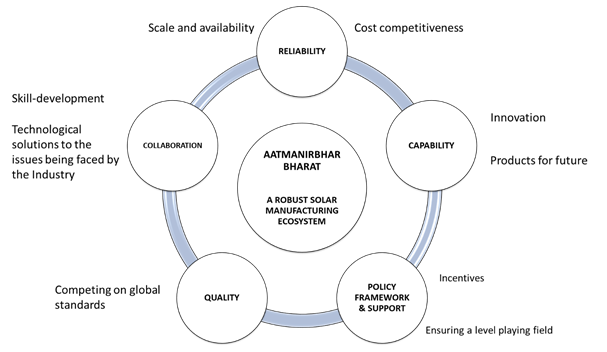

In order to create a robust solar manufacturing ecosystem in India, it is necessary for the government to acknowledge the reality of a heavily subsidized and incentivized solar components and module industry in China. A larger collaboration between the stakeholders and the government negating this unfair advantage available to Chinese manufacturers will be essential for a robust Indian manufacturing program to take root and flourish. We believe that reliability, quality, and innovation are the basic pillars of this ecosystem and Indian manufacturers are more than ready to strive in order to compete globally. The stakeholders need to focus on seeking modules made with modern and efficient technologies, which will greatly drive skill development. Finally, a stable policy framework announced by the government will provide the foundation of bedrock on which a globally competitive domestic industry will rise.

Necessary structural changes to ensure a level playing field:

Initiatives like domestic manufacturing-linked tenders ensure a sustainable demand igniting the interest of strategic players. However, in order to counter and negate the market-distorting subsidies given by few countries to their manufacturers, the Government needs to levy fair and adequate tariff barriers like BCD, ADD, CVD, etc. to provide a level playing field to domestic manufacturers. China, which is the world’s largest manufacturer of solar glass and other components, has imposed an impossibly high entry barrier by levying an import duty of 21% on imports of solar glass. India has no import duty on solar glass in India. A basic duty of at least 20% would provide a level playing field to the domestic production to counter huge subsidization in these other nations.

Import duties of at least 30% must be imposed on imports of solar modules.

Countries like Taiwan, Vietnam, and Malaysia have offered attractive subsidies to several manufacturers backed by investors, to set up large manufacturing facilities. Such enterprises have found ready investors prepared to sink large funds into these enterprises. To lend credence to India’s claim to be the new manufacturing destination, necessary policy support with financial incentives and capital subsidies is essential.

The government has already recognized that high energy costs are the bane of the competitive manufacturing industry in India. Electricity must be made available at a competitive price of about Rs. 3.50 per kWh. This could be achieved by allowing the manufacturers to set up solar farms of sufficient capacity to obtain the entire power requirements on a net-metering basis. Most solar components are made in industrial enterprises which are highly energy-intensive.

While Malaysia subsidizes supplies of natural gas to its solar glass factories, India imposes a high rate of taxation on the natural gas supplied to its solar glass factories. A first step could be to bring natural gas under the GST regime, thus taking the first step to provide a level playing field to the Indian industry.

In order to incentivize investment into solar manufacturing, a capital subsidy of 25% will ensure the attraction of investment.

A huge potential for employment creation and skill development:

Recent studies show that solar energy creates more jobs (3.5 jobs/MW/year) as compared to other energy technologies and would create nearly 4 Lakh new jobs by 2030. Roof-top and Distributed solar have the potential to bring inclusive structural social change by creating employment and wealth for urban and rural India beyond the boundaries of gender, religion, caste, etc. providing many skilling and re-skilling opportunities.

In a scenario where the solar glass requirement is largely met domestically by FY25, an additional 6,000 jobs comprising highly-skilled and skilled manpower including graduate and diploma engineers, as well as ITI holders will be created with the achievement of this capacity. Engineering graduates with specialization in the fields of mechanical, glass, electrical, electronics and instrumentation, will all be required, considering the high level of process control and automation essential for its production. Students graduating from a large number of educational institutions imparting specialized technical knowledge on glass and ceramics will find ready jobs in the industrial growth envisaged. The indirect employment potential is around 8 times that of the above-mentioned figure considering the job creation in various other activities like mining, construction, In/outbound transportation, etc. Thus, the overall employment to be generated will be over 50,000 jobs in glass manufacturing and industries and services directly related to it.

Innovation: A key to succeed in a highly competitive global solar market

In order to excel in a highly competitive global solar industry, all the stakeholders in the Indian solar industry need to keep innovating and keep themselves constantly upgrading. There is a need for increased collaboration between academia and industry. The industry would also get benefitted from a collaboration between the companies to provide technological solutions to the key issues being faced by the industry like the impact of soiling, Performance degradation of solar modules, Use of technology and data for quality improvement during manufacturing and better O&M. Creation of mechanism/ program by the government (like Front Runner Program in China or development HJT/ IBC in Europe) could also provide a boost to accelerate the development of new products with higher efficiency. This will help meet the ultimate objective of making renewable power available at the lowest possible cost.

Growth of domestic manufacturing in India:

The following table indicates the potential growth of installed solar capacity in India in the near future and its impact on domestic solar module manufacturing. The thrust on self-reliance would also help to attract investment in the critical components like a solar cell, solar glass, back sheet, etc. We have illustrated this with an example of potential growth in critical components like solar glass.

Source: Estimates by Borosil Renewables Ltd.

Source: Estimates by Borosil Renewables Ltd.

The Indian Solar Industry is at an inflection point and we are confident that with the necessary policy support, it would realize its enormous potential and achieve global recognition. India has already achieved this distinction in the automotive industry, and this shall certainly happen in solar manufacturing.

About Borosil Renewables Ltd.

Borosil Renewables Ltd. is a part of the Borosil family which is well-known for the brand “BOROSIL®” which manufactures and sells a range of labware, scientific ware, and consumer ware products. Borosil group has pioneered specialty glass manufacturing in India since 1962. Borosil Renewables Limited is the largest non-Chinese-owned solar glass manufacturer in the world, with an annual manufacturing capacity equivalent to 2.5 GW. Having doubled its previous capacity only last year, Borosil is now working on an expansion plan to further double its current annual capacity to reach a 5GW equivalent by FY22.

The company has a strong focus on innovation and is known for its pioneering achievements like the development of the World’s

- First fully tempered 2 mm thick solar glass,

- Lowest iron solar glass,

- Highest efficiency solar glass,

- First and only Antimony-free solar glass

The Company has very recently launched

- ‘Selene’ – an Anti-glare solar glass – suitable for PV installations near airports,

- Shakti: a very high-efficiency solar glass in matt-matt finish.

- An Anti-soiling coated solar glass.

The company is able to save 22% energy in comparison with the default score for glass manufacturing in Life Cycle Assessment by M/s. Solstyce, a government accredited French institute, which according to them is one of the best values so far for glass manufacturing.

The company has been expanding its export footprints across geographies. The export business has grown at a CAGR of 33% in the last 3 financial years. The European market is a major customer base for the company where it has now successfully started supplies of its newly developed products, i.e. 2.0 mm and 2.5 mm fully tempered glass. With additional production now available, it has plans to substantially increase exports by tapping more customers in Europe as also increasing its presence in the Russia, Turkey, Americas, and MENA regions.