")

The solar power sector in India is transitioning from multicrystalline module technology to monocrystalline module technology. While the latter is more efficient and less sensitive to high temperatures, it is also more expensive. India traditionally being a highly price-sensitive market, developers have so far preferred to use multicrystalline modules due to their lower costs. But now, with the cost of monocrystalline module technology falling, it is finding greater uptake. Renewable Watch takes a look at the key trends in the monocrystalline technology space in India…

ReNew Power’s 300 MW solar park in Pavagada, Karnataka

In April 2019, ReNew Power, a leading independent power producer, commissioned a 300 MW solar plant at the Pavagada Solar Park in the Tumkur district of Karnataka. This became the first utility-scale solar plant in India to use mono-passivated emitter and rear cell (PERC) solar modules, but not the only one. Many utility-scale project developers, such as Mahindra and Amplus Solar, have deployed monocrystalline modules, according to BRIDGE TO INDIA.

Central Electronics Limited

In January 2020, Central Electronics Limited (CEL), a public sector undertaking (PSU), invited bids for the supply of 100,000 monocrystalline solar cells. CEL has also floated large tenders for the supply of multicrystalline solar cells. In April 2020, it announced a tender for 1,000,000 multicrystalline solar cells. In October 2020, it again invited bids for the supply of 1.5 million multicrystalline PERC solar cells.

Kerala State Electronics Development Corporation Limited

In December 2019, Kerala State Electronics Development Corporation Limited (KELTRON) floated a tender for the supply of 282 monocrystalline PERC solar modules of 360 W. In January 2020, the company floated a tender for 196,000 monocrystalline and 196,000 polycrystalline solar modules on a per-watt basis. In September 2020, KELTRON invited bids from Indian solar PV module manufacturers for the supply of 6,500 monocrystalline solar modules for a 2 MW solar power project.

Indian Oil Corporation Limited

In September 2020, Indian Oil Corporation Limited (IOCL) invited bids for setting up a 2.75 MW grid-connected ground-mounted solar power project at the Indian Oil LPG bottling plant in Trichy, Tamil Nadu. IOCL has specified that it will use both polycrystalline and monocrystalline silicon modules with at least 17 per cent efficiency for the project.

National Institute of Wind Energy

In June 2020, the National Institute of Wind Energy (NIWE) floated a tender inviting bids from engineering, procurement and construction companies for setting up a 1 MW solar power project at Madurai Kamraj University in Tamil Nadu, using only monocrystalline modules.

Sabar Dairy, Gujarat

In October 2020, Sabar Dairy, a cooperative society in Gujarat, reportedly floated a tender for two projects of 1 MW each to be set up at its chilling centres in Idar and Dhansura. As per the tender document, monocrystalline PERC modules with an efficiency of at least 19 per cent will be used in the project.

Bharat Electronics Limited

In September 2019, PSU Bharat Electronics Limited (BEL) issued a request for quotation for the procurement of 798,430 domestically manufactured monocrystalline silicon solar cells.

Chinese module manufacturers

The market share for monocrystalline modules from Chinese module manufacturers such as LONGi Solar, Jinko Solar, JA Solar and Trina Solar has been slowly increasing in India. Chinese manufacturers have transitioned well from multicrystalline to monocrystalline technology, and see India as a promising market. They have started signing contracts for the supply of mono PERC modules with leading Indian developers and EPC companies. According to a spokesperson from LONGi, the market size for monocrystalline technology was expected to be 7-8 GW in 2020 (considering 10 GW of solar capacity deployed in India). In fact, Chinese manufactures also want the Indian solar market to shift to bifacial technology on a large scale, going forward. A few Indian manufacturers, such as Vikram Solar, Waaree, RenewSys and Goldi Solar, are also producing monocrystalline modules and are competing with Chinese manufacturers.

Domestic manufacturing opportunities

India has set up large-scale solar power capacities, but the growth of domestic manufacturing for solar PV cells and modules has been dismal. China still accounts for the majority of India’s solar PV imports. The Indian government has introduced certain measures such as the imposition of safeguard duties and the launch of large manufacturing-linked tenders to support domestic manufacturing. The push towards domestic manufacturing has become even stronger in the bid to promote self-reliance with the Atmanirbhar Bharat Abhiyan. Domestic manufacturing is also being promoted in a bid to enhance India’s energy security.

According to The Energy and Resources Institute’s (TERI) policy paper, “Solar PV Manufacturing in India: Silicon Ingot & Wafer, PV Cell, PV Module”, a key argument for domestic manufacturing is the low quality of the modules imported from China. The paper argues that it is generally believed that while Chinese manufacturers export Grade-1 and Grade-2 PV panels to the US, EU and Japan, low-cost Grade-3 and Grade-4 panels are exported to India. It adds that a recent study of many Indian PV projects has shown higher than expected annual degradation, indicating that projects using Chinese modules are at greater risk. Thus, securing the supply chain for solar modules eliminates the risk of poor quality products being dumped in India by China.

The Indian solar market is expected to grow at 10-20 GW per year, which would be a huge opportunity for domestic manufacturers – potentially creating nearly 100,000 jobs in solar manufacturing and saving $2.5 billion-$5 billion of annual forex outgo, according to TERI. However, currently, 80 per cent of the requirement is met through imports.

But promoting domestic module manufacturing is not that easy, as the sector suffers from two key problems – higher pricing and underutilisation of capacity. According to CEEW’s report, “Scaling Up Solar Manufacturing”, Indian-made solar modules are nearly 33 per cent more expensive than their Chinese counterparts (assuming 50 per cent and 100 per cent capacity utilisation for Indian and Chinese manufacturers, respectively). Apart from these issues, past trends show that manufacturers have faced issues owing to lack of clarity regarding BIS certification and the Ministry of New and Renewable Energy’s Approved List of Models and Manufacturers.

While formulating policy for domestic manufacturing, it is important that the production of monocrystalline modules is given priority. This will not only improve the quality of solar assets in India going forward, but also make Indian modules globally competitive. A major transition towards monocrystalline technology (and later bifacial) is crucial. So far, the availability of mostly multicrystalline modules has led to its deployment under tenders that had a domestic content requirement.

Moreover, the removal of price ceilings from tenders will help monocrystalline module manufacturers as developers will have greater bandwidth to bid for higher tariffs and use monocrystalline modules for projects to be set up in the future.

The way forward

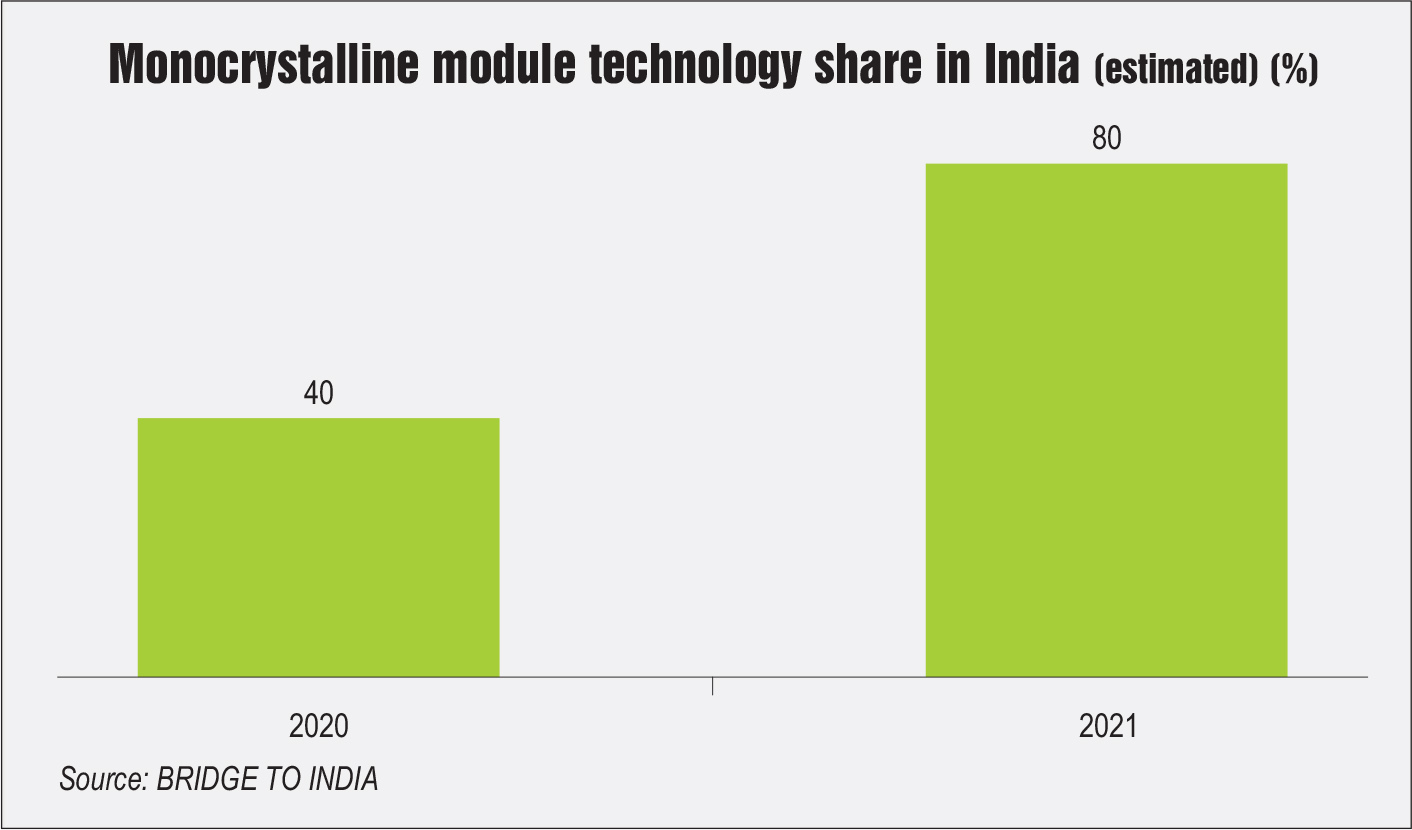

Going forward, the interest in multicrystalline modules is expected to wane and these are expected to phase out in the coming few years. According to BRIDGE TO INDIA estimates, monocrystalline modules had a significant price premium of 15-20 per cent over multicrystalline modules. Further, according to their estimates, the price gap needed to reduce to 1 per cent in order to offset the efficiency gains that arise by using monocrystalline modules. In a bid to improve the efficiency of solar assets, developers in India have started to shift from multicrystalline to monocrystalline technology. This trend is expected to continue as the price differential between the two technologies has reduced considerably. BRIDGE TO INDIA had estimated the share of the monocrystalline module market in the country to reach 40 per cent in 2020 and 80 per cent in 2021. Summing up, it will be interesting to see how the market transitions to monocrystalline technology, especially given that it will slowly start facing competition from bifacial module technology.