The Indian solar power industry has grown rapidly over the past two years. This has increased investor confidence in the segment, leading to greater capacity additions and new solar power applications. The growth is also reflected in associated markets such as mounting structures. These are structures that provide vertical angle and support to solar panels. Typically made of stainless steel that is either pre-galvanised cold rolled or hot-dipped galvanised (HDG), these structures are high enough to avoid flood risk and strong enough to withstand high-speed winds. Further improvisations are made to the structures depending on the geographical and climatic conditions at the solar plant site.

Mounting structures provide all the essential elements to drive solar power generation. They help tilt the panels at a specific angle, ensuring maximum irradiation per unit area. Over the years, mounting structures have found applications beyond the traditional ground-mounted solar power plants and are now used at rooftops, carports and other sites irrespective of the surface. Technological innovation in the mounting structure segment has brought in tracker-based mounting structures, with better material at reduced costs and increased strength, thus driving solar power generation.

Material trends

There are two types of mounting structures, categorised by the tilt of the panels. The fixed tilt structures are used for solar panels typically facing the south direction, while the seasonal tilt structure allows the south-facing panels to be adjusted seasonally. These structures are composed of a mix of HDG and pre-galvanised steel, or galvalume. The majority of the projects are based on these technologies. Developers are also increasingly deploying solar tracker technology, where modules are mounted facing east-west and the tracker follows the sun’s path to maximise generation. Such structures use only HDG steel. Even though fixed-tilt systems cost less than tracker-based mounting structures, many developers are now shifting to tracker-based systems, citing increased energy generation. This energy gain varies across locations. For instance, an increase of over 21 per cent has been observed in Tamil Nadu and Andhra Pradesh.

The selection of material for mounting structures is based on two key considerations – the location of the plant and its life cycle of almost 25 years. Over time, various materials from wood to polymer have been used to create durable mounting structures, but stainless steel has proven to be the most cost-effective of all. Of late, developers and structure manufacturers have also been using aluminium as one of the materials.

Polymers provide an effective alternative to traditional solar mounting structure material as these are robust, lightweight, weather and corrosion resistant, and easily mouldable. However, the process of producing polymer-based mounting structures is cost-intensive, making these more expensive than steel structures. With a decline in the cost of material and increased demand, the cost of these mounting structures is expected to reduce in the next few years.

Galvalume, an alloy of 55 per cent aluminium, 43.5 per cent zinc and 1.5 per cent silicon has emerged as another popular raw material for mounting structures. The technology has found many takers across the world, with JSW Steel being one of the first licensees in India. It is durable, sustainable, cost-effective and low maintenance.

Steel demand

To produce mounting structures, 40-60 tonne of steel is required for 1 MW of solar power capacity. Over the next five years about 85 GW of solar power capacity has been planned. Thus, about 4.25 million tonnes of steel will be needed to realise the government’s solar target.

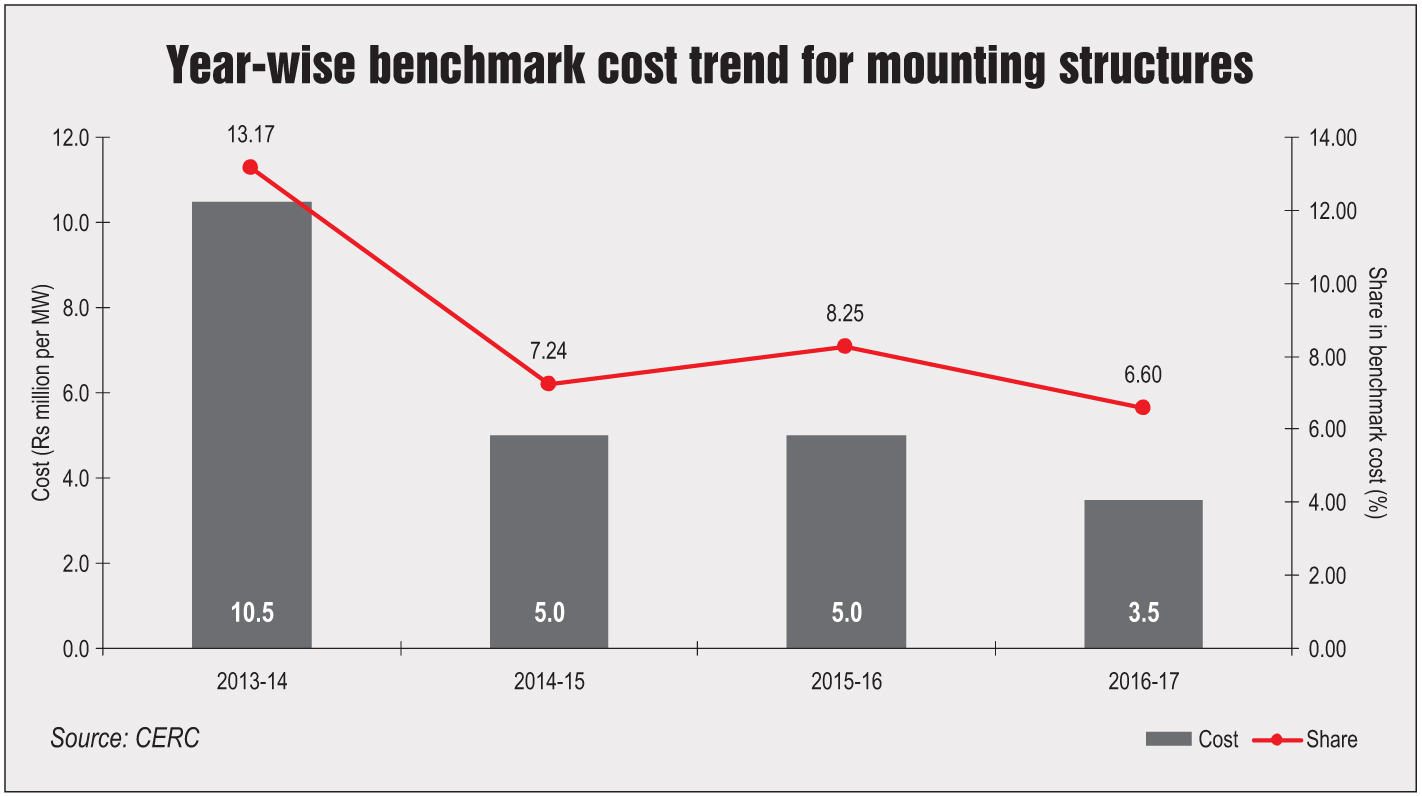

Cost trends

The benchmark costs of mounting structures have been decreasing in line with other capital costs. The cost of mounting structures, as determined by the Central Electricity Regulatory Commission (CERC), has decreased to Rs 3.5 million per MW in 2016-17 from Rs 10.5 million in 2013-14.

A primary reason for this is the competitive bidding process, which compels developers to adopt cost-effective technology solutions. The CERC has not provided benchmark costs for 2017-18 as costs are now determined on a project basis given the variability in project sites.

Challenges

In recent years, the market has flooded with mounting structure designs that are cost-competitive and easy to install, but are not strong enough to support the panels throughout the project life cycle. Moreover, the cost of raw material such as steel and aluminium has been fluctuating, affecting the mounting structures market. Manufacturing issues and an influx of low-grade raw material from China are leading to quality issues across the industry. Further, mounting structures need to be customised as per the project requirements and site conditions, thereby incurring additional costs. Since all projects are quite different from one another, a one-size-fits-all solution may be detrimental to the quality of mounting structures. Research and development in the raw material industry is also not in sync with the rapid pace of developments in the solar power market.

Emerging applications

With growing solar power applications, the market for mounting structures is also expanding. There has been a considerable increase in rooftop solar capacity in the country, which calls for design and technology innovation in mounting structures. For example, the installation of solar panels on the dome of the National Institute of Solar Energy headquarters, located in Gwalpahari, Haryana, required customised mounting structures. This proved to be a particularly challenging project as the mounting structure had to be fitted into the hollow space of the mesh-like structure of the building’s rooftop.

With solar power deployment in Indian Railways, especially on train coaches, the market for mounting structures has found yet another unusual application. These coaches require specially designed mounting structures to endure the strong winds and maintain their stability despite the rattling motion of the train.

Floating solar and canal-top solar plants are also emerging as applications of mounting structures. In the case of canal-top projects, constructing large structures without damaging the canal and its function becomes a challenging task. Such mounting structures must be lightweight, or else they could adversely impact the structural integrity of the canal. Galvanisation of structures used for these plants is another major challenge. However, a number of mounting structure manufacturers have devised designs for such projects, which are coming up in states like Punjab and Haryana.

Outlook

The mounting structures market is expected to grow significantly in the near future with increasing solar power installations. According to media reports, steel prices are expected to increase to Rs 6,000 per tonne due to high demand from the automotive sector. Therefore, the steel market for mounting structures in the solar power industry could be worth Rs 25.5 billion over the next five years, if the country meets its 100 GW solar power target.

Steel-based structures are expected to dominate the market unless galvalume or other polymer-based materials become cost-competitive. Further, the industry needs to invest in research and development to bring down the cost of mounting structures in line with the module prices and other capital costs.