This 2016 article from our archives captures the landmark decision of the government to switch from feed-in-tariffs to competitive bidding for wind power projects.

For a quarter-century of its existence, the Indian wind energy segment has been selling power at fixed feed-in tariffs (FiTs), earlier determined by the state governments and now by the state electricity regulatory commissions (SERCs). Price discovery through competitive bidding has been proposed several times by various state governments but never actually implemented, largely due to resistance from wind power project developers.

However, after witnessing the advantages of competitive bidding in the solar power segment, the case for introducing this method of project allocation in the wind power segment has become stronger. Price discovery through competitive bidding has brought down the cost of solar power significantly, from Rs 17 per kWh in 2010 to Rs 4.34 per kWh in 2016. While there were various other reasons that were also responsible for driving down the cost of solar power, such as a decline in equipment prices and a glut in the solar module industry, the key role that competitive pressures have played in achieving such low price levels cannot be denied.

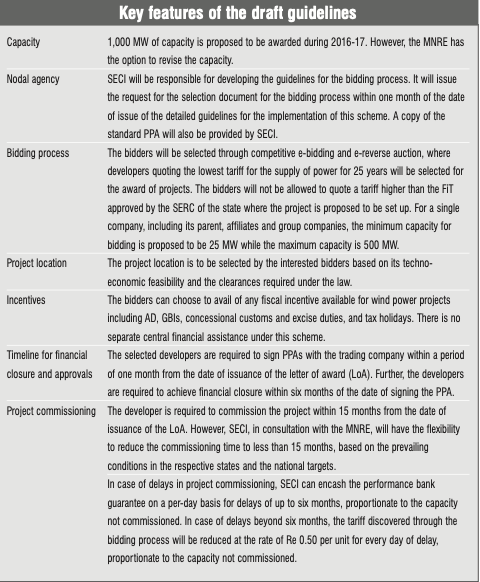

Against this backdrop, the Ministry of New and Renewable Energy (MNRE), on June 14, 2016, issued a scheme for the award of 1,000 MW of wind power projects connected to the transmission network of the central transmission utility (CTU). The key objectives of this scheme are to facilitate the supply of wind-based power from high- wind-potential states to those with relatively lower potential, and encourage competitiveness by scaling up project sizes and introducing competitive bidding.

Clearly, this is a positive step from a capacity addition point of view, given that the key wind power states have revised their wind power tariffs downward for 2016-17. Maharashtra has reduced its tariffs by 2-3 per cent, from Rs 3.92-Rs 5.70 per kWh to Rs 3.82-Rs 5.56 per kWh. Meanwhile, Madhya Pradesh has revised its wind tariff from Rs 5.96 per unit for 2015-16 to Rs 4.78 per unit for the three- year control period till the end of 2018-19.

Low tariffs coupled with a slowdown in the signing of fresh power purchase agreements (PPAs) in the past six to eight months and reported delays in payments by the state-owned utility of Maharashtra are likely to further impact fresh wind capacity addition in the country in the near to medium term. This is given the fact that Maharashtra and Madhya Pradesh together account for 35-40 per cent of the total wind capacity addition in the country during the past two years.

The decision to phase out accelerated depreciation (AD) benefits with effect from April 2017 may further impact annual capacity additions negatively, though marginally. In this context, the decision to allocate 1 GW of wind power capacity through competitive bidding is definitely a welcome move. According to a recent ICRA report, this move will encourage capacity addition and facilitate the purchase of wind-based generation by dis- coms of states that have limited wind energy resources. As a result, these discoms will be able to honour their non- solar renewable purchase obligation (RPO) to some extent. Although the option of renewable energy certificates (RECs) is available to such utilities to meet the RPO norms, ICRA observes that the REC route is not exercised by distribution utilities in many cases. Further, the introduction of tariff-based bidding for the allocation of wind projects under this scheme is expected to lead to efficient price discovery, which will be favourable for the discoms.

Past attempts

In the past, several states including Rajasthan, Karnataka, Madhya Pradesh and Maharashtra have announced plans to award wind projects via competitive bidding. However, on each occasion, strong industry opposition has led these states to shelve their plans. Among these, the last to have attempted this route for project allocation was Rajasthan, which released its wind power policy in July 2012 and issued the draft request for proposal for competitive bidding in January 2013.

As was the case with the other states, Rajasthan’s move to award wind projects via competitive bidding was criticised by industry stakeholders and opposed by project developers as well as wind turbine manufacturers. Hence, the state government had to withdraw its tender.

While the industry agreed that, in principle, the reverse bidding mechanism was logical, it believed that it was premature to introduce it due to inadequate data and infrastructure availability. Moreover, the wind segment needed some time to recover from the negative developments of 2012, such as the withdrawal of AD and generation-based incentives (GBIs).

Some developers also believed that awarding wind projects via reverse bidding would mean indirectly favouring the existing developers in the state. Unlike the solar segment, where insolation levels within a state do not vary considerably, wind speeds can vary by large margins within a district itself. Therefore, a detailed resource assessment of a site, which typically requires two to three years, is crucial before any investment decision is taken. In such a scenario, competitive bidding may unjustly favour existing developers who had already carried out resource assessment studies of potential sites. They would be able to submit bids with reasonable estimations about future revenue streams while the new developers would refrain from participating in the process owing to uncertainty about project viability. An uncertain future revenue stream would result in difficulties in achieving financial closure for the projects.

Change in sentiment

The market scenario, and therefore the rationale, for competitive bidding has changed considerably since the last attempt was made to introduce competitive bidding.

One argument in favour of competitive bidding is that if the wind power industry does not bring down costs, it faces the risk of pricing itself out. In contrast, the cost of solar power is quite low, with some industry experts predicting that it could reach Rs 3 per kWh by 2020. Further, there is talk of bringing the hydropower segment under the purview of the MNRE from the Ministry of Power. This would give the state governments the option to buy hydropower to meet their RPOs. Therefore, there is increased pressure on the wind power segment from all sides to bring down prices.

Second, a large segment of the industry now believes that the FiT route of project allocation has several disadvantages and prevents many state discoms from signing fresh PPAs. One of the disadvantages is that state-level tariffs are determined on a cost-plus basis, which may result in inefficient generation costs owing to asymmetric information on market and technology conditions. This may lead to difficulty in realistically benchmarking input assumptions such as capacity utilisation factor, thus resulting in higher prices for consumers and inefficient utilisation of the finite resource.

It is sometimes argued that the benefits from technology improvements, such as from installing taller turbines with larger rotor diameters, are not captured in the actual performance or indexing parameters that are used to calculate the costs.

Further, it must be noted that elsewhere in the world where fixed tariffs are adopted, the tariffs decline over the term of the PPA. However, in India, the tariffs remain fixed for the entire period of the PPA, even if generation is higher than thatassumed while determining the FiT. While this can generate windfall profits for developers if tariffs are set too high, it can negatively impact discom finances. On the other hand, if tariffs are set too low, it may limit the entry of players in the market. This is a regular scenario in the Indian context where a reduction in wind power tariffs for a particular period leads to limited greenfield project development during that period.

Ensuring success through reverse auctions

According to a 2015 report by the Centre for Study of Science, Technology and Policy, the success of competitive bidding depends on several factors, including the availability of investment-grade wind resource assessment; pre-identified land zones for development of projects; transmission layout planning for evacuation, with proposed interconnections in the interstate transmission system to ensure power supply by resource-rich to resource-deficit states; clearances and approvals for pre-identified zones; and necessary conditions in PPAs such as payment guarantees.

Past attempts by the state governments to introduce reverse auctions for wind project allocation have not taken most of these factors into consideration. However, in the upcoming 1,000 MW tender which the Solar Energy Corporation of India (SECI) will be responsible for developing the guidelines for the bidding process and a suitable mechanism for monitoring the performance of projects – at least three of the aforementioned factors have been taken care of.

According to the draft guidelines, the selected projects are to be designed for interconnection with the central transmission network at the 220 kV or above level. The developer will be responsible for connecting and transmitting power from the project to the interconnection point of the CTU at its expense. The CTU may provide details of substation-wise transformation capacity available for injection in the tender document to facilitate the selection of project sites by the developers. The developers are also responsible for the scheduling and deviation settlement as per the regulations approved by the Central Electricity Regulatory Commission (CERC)/SERCs.

Notably, wind power projects that are under construction, or those that are not commissioned, or are being commissioned without any PPA in place will be considered under this scheme. As such, project developers can participate in this scheme at any stage of project development.

As far as payment guarantee is concerned, SECI, through a pre-selected trading company, will be responsible for tying up back-to-back power sale agreements (PSAs) with discoms of low-wind-potential states at the pooled price of the selected bids. The duration of the PPAs and PSAs will be 25 years from the date of commercial operation of the project. According to the draft guidelines, SECI will complete the process of selecting the trading company before inviting bids for wind power projects so that bidders have clarity on the counter-party before signing the PPA. The selected trading company will be entitled to charge a trading margin as agreed mutually between the parties or as decided by the CERC for long-term power purchases. The trading company is required to share at least 25 per cent of the trading margin with SECI without any liability to SECI.

Points of contention

Points of contention

While time will tell whether the MNRE’s decision to introduce competitive bidding will benefit the wind power industry, some experts point out that the 1,000 MW tender scheme is fraught with problems. Some developers too have raised concerns that need to be addressed in the final set of guidelines.

A key point of contention is the selection criteria clause, which suggests that a bidder will not be allowed to quote more than the FiT set by the concerned SERC. According to Sunil Jain, chief executive officer and executive director, Hero Future Energies, “This clause could be eliminated as the procurer has the last right to accept or reject the prices in a tender.” According to him, since the procurer is a central agency, the government can adopt the CERC tariff as the base price against which bidding can take place.

Some experts also argue that with reverse auctions there may be a possibility of irresponsible players negatively impacting the industry by making overaggressive bids. However, the size of the tender is bigenough to accommodate a large number of serious players. As M.R. Sreenivasa Murthy, former chairman, Karnataka State Electricity Regulatory Commission, notes in a media statement, “Even if there is a maverick bidder who quotes suicidal tariffs, it can be only a part of the capacity offered, say, 200 MW out of 1,000 MW; the quotes for the rest of the capacity will surely be sensible.”

According to the ICRA report, from an independent power producer’s (IPP) perspective, the project economics will be critically dependent on the plant load factor and the competitively bid tariff as well as vendors’ ability to bring down the project cost, particularly the cost of equipment purchased from wind turbine generator manufacturers. Given the competitive bidding involved for the award of projects, IPPs’ ability to ensure a superior operating performance by deploying efficient and superior wind turbines at a location with high wind speeds will also be critical for deriving the expected returns. Further, the identification of land banks with high wind power potential will remain a key challenge for IPPs.

Another concern that the scheme fails to address relates to the availability of past site data. Unlike a solar project, which can be set up wherever there is sunlight, windprojects require careful wind resource assessments. Data needs to be gathered for at least three years for the developer to arrive at a good estimate of electricity generation. The absence of data is a big risk that will need to be factored in and may lead to very conservative tariff bids, thus defeating the entire purpose of introducing reverse bidding. While initially for developers that have land banks with sizeable past data records will be able to bid effectively, for the long-term success of such schemes the government will need to procure land and undertake resource assessments for several years before inviting bids for projects on that land.

The final guidelines also need to provide clarity on transmission charges. Currently, the state governments levy charges for using their transmission infrastructure if the power is sold outside their state. These charges work out to Re 0.40-Re 1 per kWh. This could prevent developers from quoting competitive bids.

In sum, while the MNRE’s attempt to give a fillip to wind power capacity addition is definitely a step in the right direction, it needs to undertake extensive preparatory work and address ground challenges before finalising the guidelines and releasing the tender.