By Preeti Wadhwa

Green hydrogen is emerging as a catalyst in India’s transition to a low-carbon economy. Its potential to cut industrial emissions, reduce reliance on imported fossil fuels and enhance long-term energy security has positioned it as a strategic pillar in the country’s decarbonisation efforts. This momentum is being driven by India’s rapidly growing renewable energy capacity, which is essential for large-scale green hydrogen production. Meanwhile, declining renewable energy prices, advances in electrolyser technology and rising global demand for low-carbon hydrogen and its derivatives are further reinforcing the sector’s growth prospects.

The National Green Hydrogen Mission is the backbone of this transition, providing a clear road map for domestic uptake as well as export-oriented growth. Measures such as waivers on interstate transmission system (ISTS) charges, targeted incentives for hydrogen and electrolyser production and a phased implementation approach have created a strong policy foundation. As a result, industry participation has accelerated, with both public and private developers announcing ambitious projects across green hydrogen, green ammonia and electrolyser manufacturing.

The past year marked a decisive shift for the sector as policy interventions, incentives and mission-driven programmes began to translate into on-ground activity. The market moved beyond broad planning to visible early-stage implementation, signalling the beginning of a more mature phase of green hydrogen deployment in India.

Regulatory updates

Regulatory activity in the sector gained momentum over the past year. A major regulatory milestone was the launch of the Green Hydrogen Certification Scheme of India in April 2025. The scheme established a national framework to measure and verify the greenhouse gas intensity of domestically produced hydrogen. It creates the traceability needed for international exports and links green hydrogen to India’s carbon credit market.

The momentum continued in June 2025 with the  release of revised guidelines for hydrogen valley innovation clusters and green hydrogen hubs. Four clusters were approved shortly thereafter, receiving the first tranche of central financial assistance in July 2025. These hubs aim to act as test beds and living laboratories that foster innovation, build regional value chains and create anchors for long-term hydrogen utilisation. Parallel efforts began to identify potential sites for large hydrogen hubs with planned capacities of 100,000 tonnes per annum (tpa).

release of revised guidelines for hydrogen valley innovation clusters and green hydrogen hubs. Four clusters were approved shortly thereafter, receiving the first tranche of central financial assistance in July 2025. These hubs aim to act as test beds and living laboratories that foster innovation, build regional value chains and create anchors for long-term hydrogen utilisation. Parallel efforts began to identify potential sites for large hydrogen hubs with planned capacities of 100,000 tonnes per annum (tpa).

A further regulatory intervention came in August 2025, with the revision of guidelines for pilot projects in residential, commercial and decentralised applications. The updated framework prioritises modular and community-level production models such as rooftop solar integrated with small electrolysers, floating solar systems, micro hydro and biomass. The scheme provides dedicated allocations for technology pilots and start-up-led initiatives, offering financial assistance of up to Rs 250 million for pilot projects and Rs 50 million for start-up demonstrations.

Auctions and tender activity

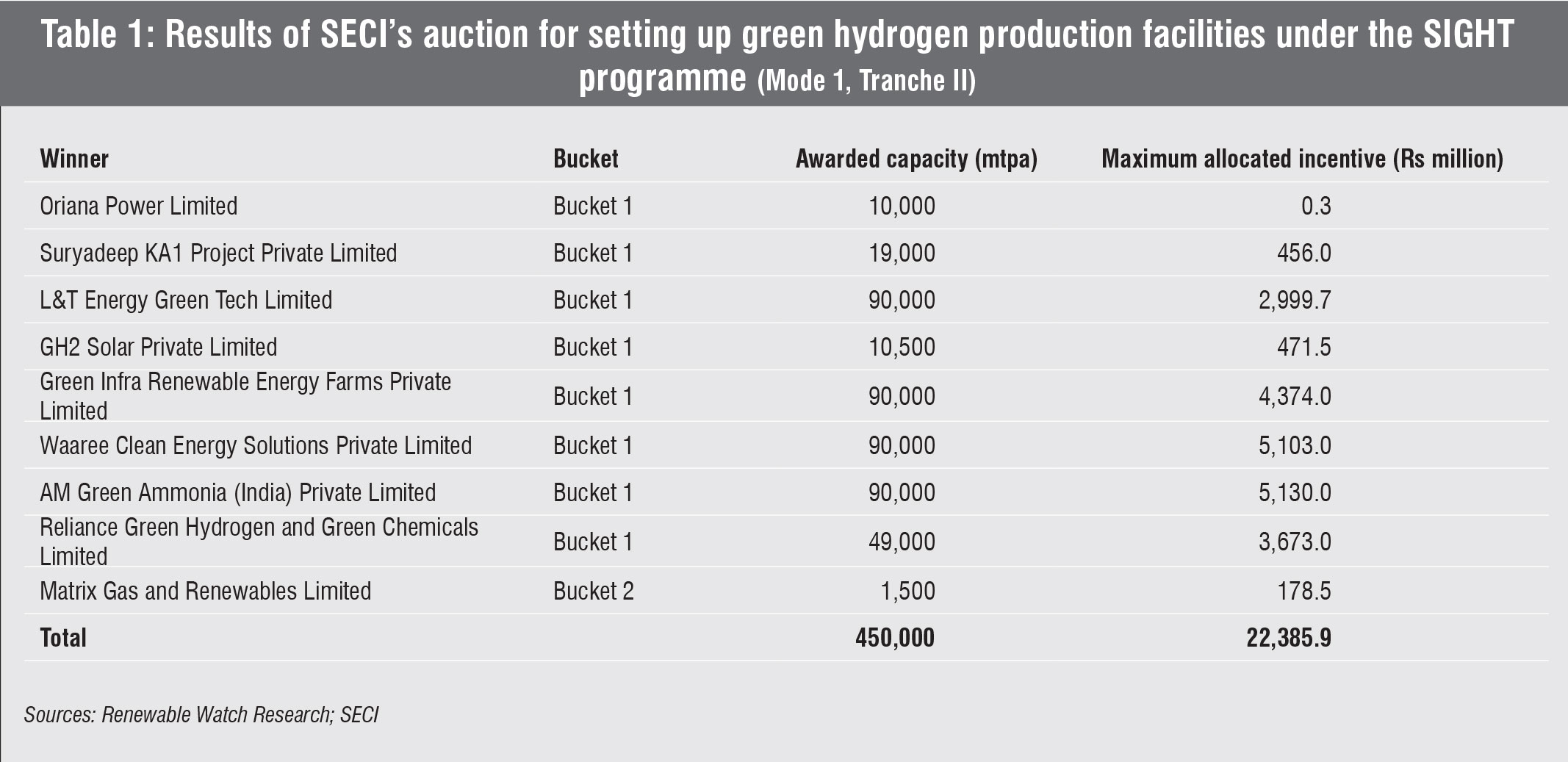

The year witnessed strong bidding activity, particularly for green hydrogen and green ammonia under the Strategic Interventions for Green Hydrogen Transition (SIGHT) programme. In March 2025, the Solar Energy Corporation of India (SECI) announced the results of its auction under the SIGHT programme (Mode -1, Tranche II) to select producers for setting up green hydrogen production facilities in India. The programme aims to promote large-scale green hydrogen production, improve cost competitiveness and facilitate rapid expansion. A total annual production capacity of 450,000 metric tonnes was awarded, as shown in Table 1. The competitive bids demonstrated growing developer confidence in long-term project viability.

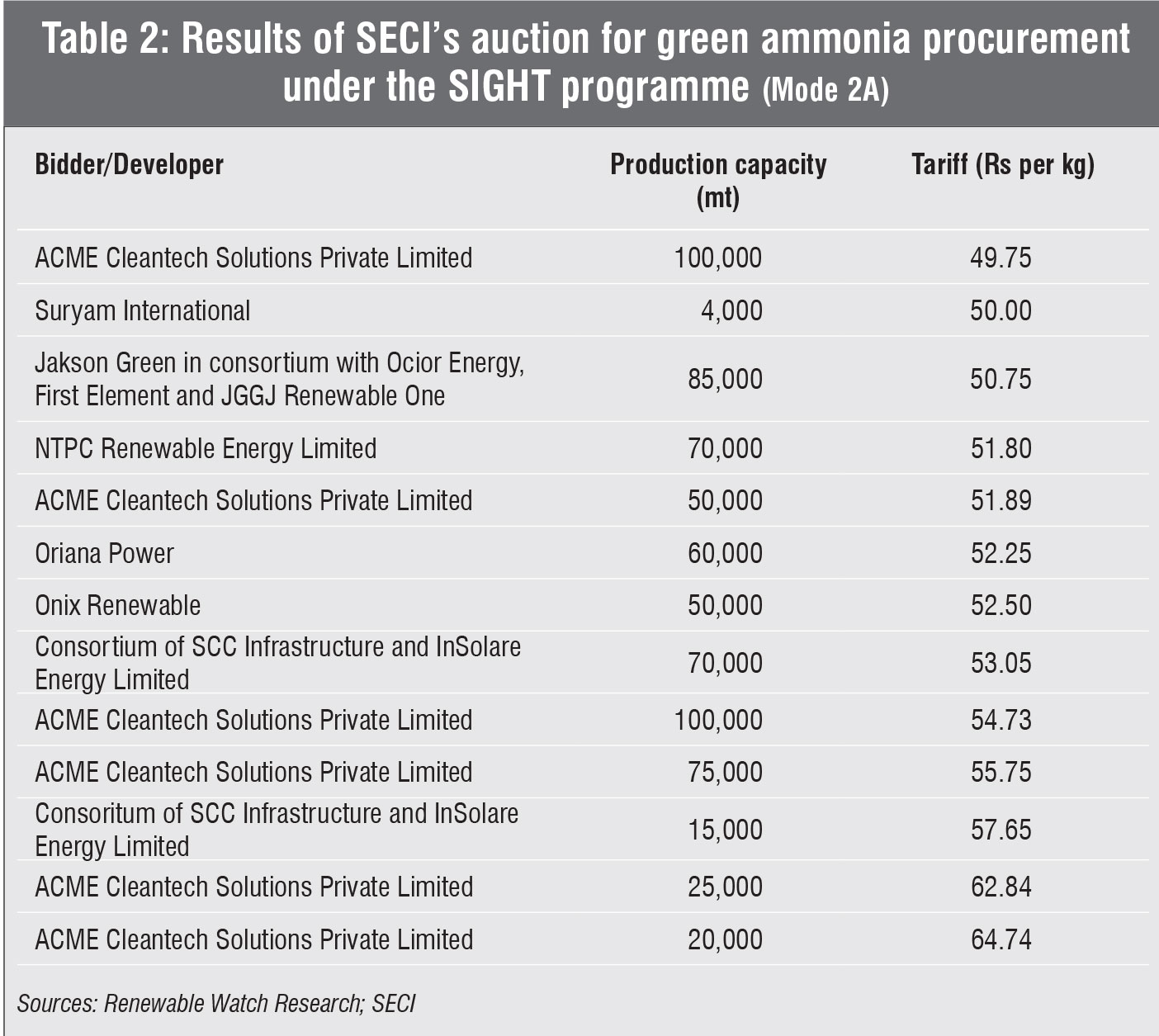

In September 2025, SECI announced the results of the Tranche 2A green ammonia auction under SIGHT Mode 1 for the uptake of green ammonia by fertiliser companies. The lowest tariff discovered was Rs 49.75 per kg of green ammonia, as shown in Table 2. This marked a significant milestone, with prices only marginally higher than prevailing grey ammonia costs, indicating rapid progress towards cost competitiveness.

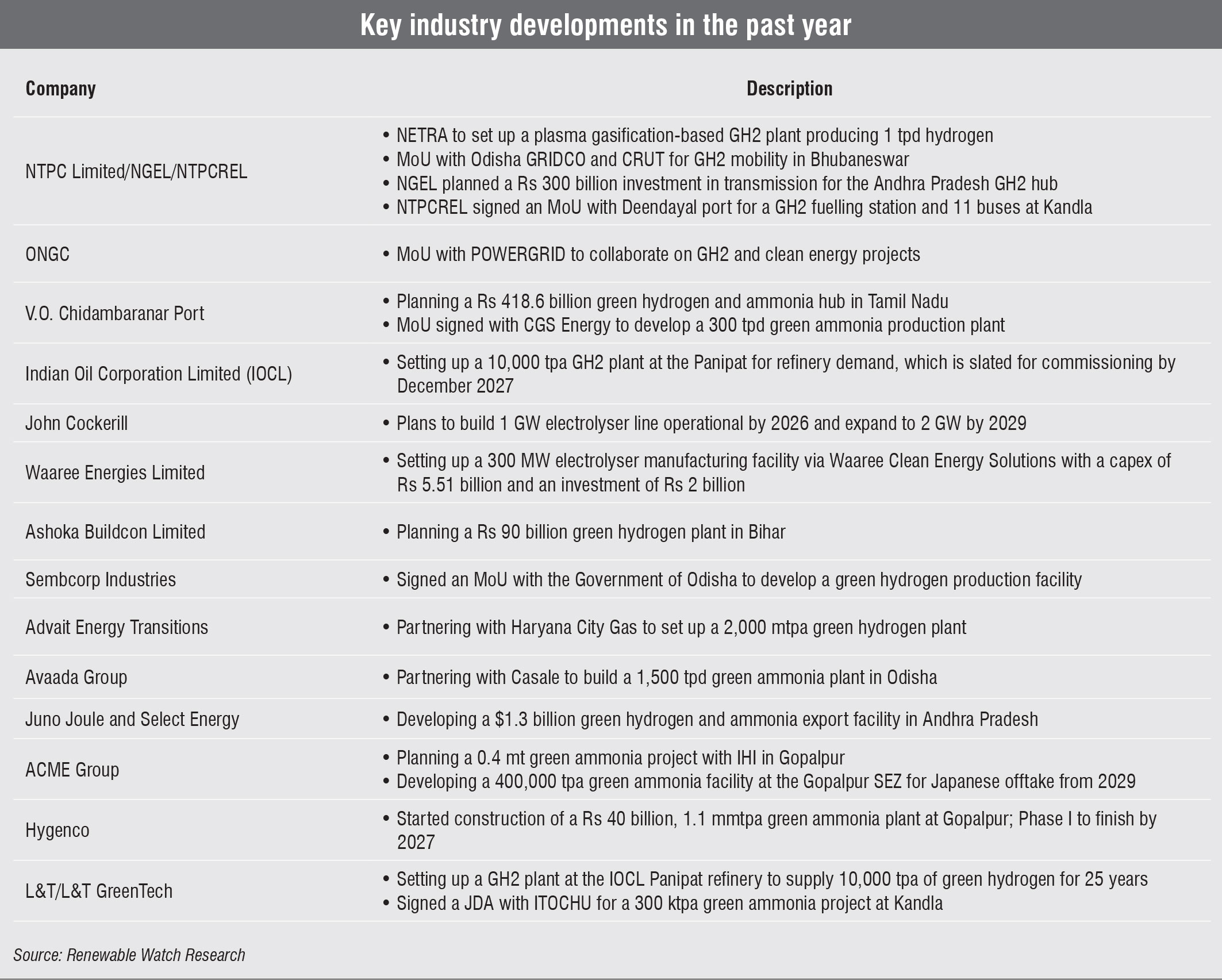

Furthermore, the year saw growing traction for green hydrogen in the refinery segment, with oil and gas majors moving towards long-term offtake arrangements. Larsen & Toubro won Indian Oil Corporation Limited’s tender to develop a green hydrogen plant at IOCL’s Panipat refinery in Haryana, which will supply 10,000 tonnes of green hydrogen annually. Ocior Energy secured a contract to supply 5,000 tonnes of green hydrogen per year to Hindustan Petroleum Corporation Limited’s Visakhapatnam refinery in Andhra Pradesh. The project will be implemented under a build, own and operate model and operate for 25 years.

The year also saw continued tender activity from NTPC Limited, SJVN Limited, Chennai Petroleum Corporation Limited, Power Grid Corporation of India Limited, oil and gas majors, and several state renewable energy agencies, reflecting a broad national commitment to advancing hydrogen production, storage and mobility applications. The tenders were issued for green hydrogen production plants, electrolyser systems, fuel cell-based microgrids and hydrogen refuelling stations, signalling a decisive shift towards building a nationwide hydrogen ecosystem. The steady flow reinforced the demand-side assurances needed for commercial-scale investments.

Challenges and the way forward

Despite visible progress, the green hydrogen sector continues to face structural challenges that limit the pace and scale of implementation. The most critical constraint remains access to round-the-clock renewable energy, which is essential for operating large electrolyser systems efficiently. Transmission availability, banking provisions and storage integration require further clarity and streamlined regulations, particularly for developers planning gigawatt-scale projects. Water availability and land allocation challenges, especially around coastal zones earmarked for green ammonia facilities, continue to slow down project development.

Project developers are also navigating the growing complexity of certification and monitoring requirements under the Green Hydrogen Certification Scheme of India. While these frameworks are essential for ensuring global market competitiveness and traceability, they add compliance burdens for early-stage projects. Domestic electrolyser manufacturing has gained momentum but remains dependent on imported stacks and key components, keeping costs elevated. Uncertain demand offtake remains a major bottleneck, creating a vicious cycle of low scale and high capital costs. Hard-to-abate sectors such as steel, fertilisers and heavy transport require clearer long-term procurement signals to support investment decisions.

Financial closure is another challenge, as lenders remain cautious about first-of-a-kind hydrogen and ammonia projects with untested business models. Although auction prices have started to fall, the cost gap between green and grey hydrogen persists, affecting near-term commercial viability.

Looking ahead, the focus will be on scaling pilots, strengthening certification infrastructure and building regional hydrogen ecosystems that can support both industrial and decentralised applications. The coming year is expected to see increasing hydrogen production and electrolyser capacity. Continued tendering under the SIGHT programme, combined with a maturing green ammonia market, is likely to draw stronger investment in 2026. If regulatory support continues to align with falling renewable energy costs, India can position itself among the world’s lowest-cost producers, with the potential to bring green hydrogen below $3 per kg and gradually approach $1 per kg by 2030. Recent price discoveries in competitive auctions have strengthened this outlook, indicating that cost reductions are already beginning to materialise at scale.

Going forward, addressing the current challenges, particularly around offtake certainty, scale and manufacturing capacity, will remain key to sustaining the sector’s growth. The past year marks India’s transition from planning to early execution, with green hydrogen steadily moving from just vision to reality.