By Sakshi Bansal

India’s solar energy segment is undergoing a significant transformation as the country intensifies its efforts to harness solar power to meet its growing energy demand. This growth is driven by a combination of progressive government policies, technological advancements, falling equipment costs and increased investments.

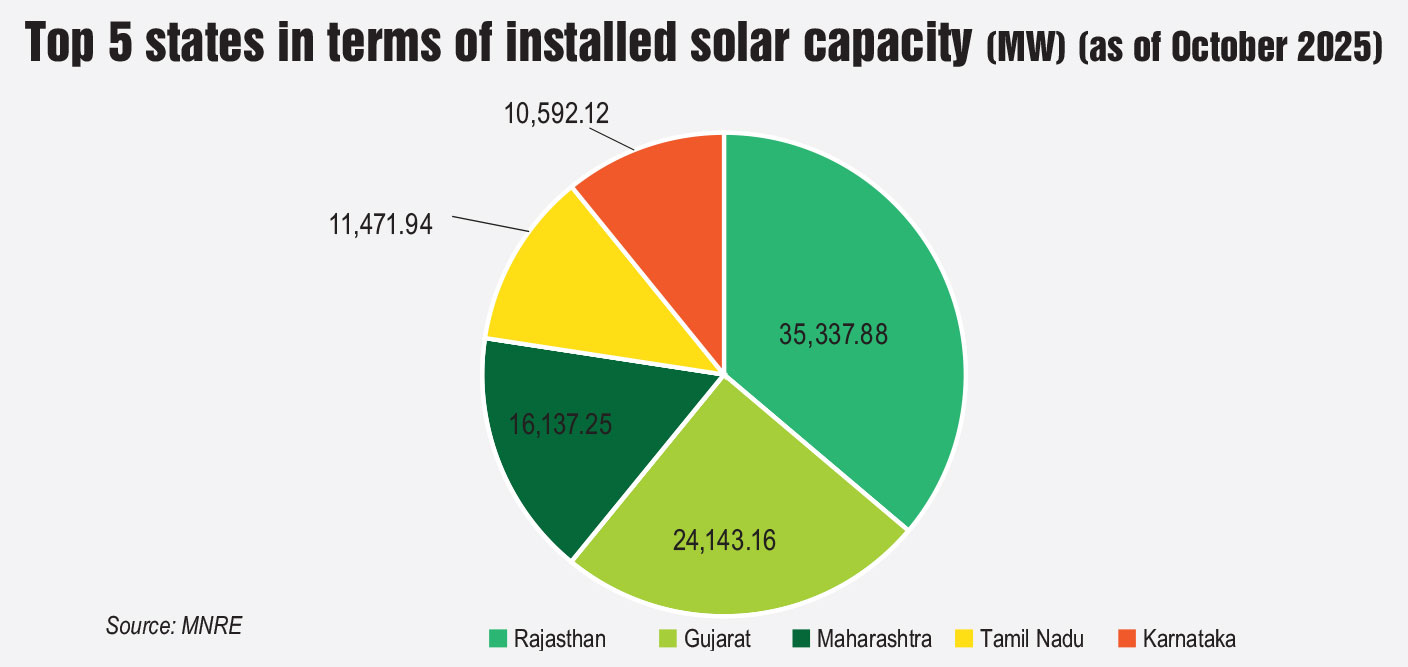

India’s installed solar power capacity has grown significantly, rising from 2.8 GW in 2014-15 to about 129.92 GW (as of October 31, 2025), according to the Ministry of New and Renewable Energy (MNRE). This translates into a growth rate of 4,540 per cent over the decade. Solar power accounts for over 51.84 per cent of the total installed renewable capacity. Utility-scale solar accounts for about 76 per cent of the total solar installations, contributing around 98.7 GW of capacity. Rooftop solar and off-grid solar projects, although smaller in scale, have added approximately 22.4 GW and 5.4 GW respectively. The remaining solar capacity, about 3.3 GW, falls under the hybrid solar category.

Over the past year, there have been several notable developments – in terms of policy announcements and project implementation – across all solar subsegments. Investments in solar manufacturing have also been rising, driven by proactive government policies.

An overview of the recent policy developments, tendering activity and key trends across the solar segment, as well as the future outlook…

Policy developments

In light of the growing importance of rooftop solar, off-grid solar, and domestic manufacturing, various policy measures have been introduced to support the goal of achieving 280 GW of solar capacity by 2030.

Rooftop solar

Under the PM Surya Ghar Muft Bijli Yojana (PMSGMBY), the past year saw multiple new guidelines and amendments to boost outcomes. These included the MNRE’s guidelines in January 2025 for implementing two critical components – central financial assistance (CFA) for residential consumers under the renewable energy service company (RESCO) and utility-led aggregation (ULA) models and a payment security mechanism to ensure timely payments to RESCO developers. In May 2025, the MNRE issued a call for proposals under the Innovative Projects component of the PMSGMBY scheme. Furthermore, in July 2025, it issued amendments to the guidelines for implementation of the CFA component of the scheme for residential consumers. In the same month, the ministry amended the “incentive to local bodies” component of the implementation guidelines under the scheme. Additionally, the MNRE amended the guidelines for implementing the Model Solar Village under the scheme, with a focus on eligibility and selection procedures. During the same month, the ministry mandated that all original equipment manufacturers enlisted for supplying inverters under the scheme should connect their inverters directly to the national servers and software managed by the MNRE or its designated agencies. Furthermore, in October 2025, the MNRE issued guidelines for the release of CFA for rooftop solar projects under the ULA model.

Offgrid

In May 2025, the MNRE revised the minimum efficiency norms for solar modules under the Approved List of Models and Manufacturers (ALMM). The update applies to offgrid projects such as solar lamps, streetlights and fans using modules below 200 Wp, excluding agricultural pumps and rooftop systems. The minimum efficiency for crystalline silicon (c-Si) modules has been reduced from 19 per cent to 18 per cent, while cadmium telluride (CdTe) modules remain at 18 per cent. A new ALMM List-I (DRE) has been created for offgrid applications, separate from the main list. The MNRE has also added a fourth category, “Any other application”, with minimum efficiency requirements of 19 per cent for c-Si and 18 per cent for CdTe modules.

ALMM

The solar manufacturing segment has also witnessed notable growth during the past year, with the announcement of an ALMM for solar cells in December 2024. The MNRE announced the inclusion of solar PV cells in the newly introduced List II under the ALMM, from June 1, 2026 onwards. In March 2025, the MNRE issued updated domestic content requirement norms for solar cells. Furthermore, in May 2025, the ministry clarified that net billing, virtual net metering and group net metering will be treated at par with the net metering provisions under ALMM List II. Recently, in August 2025, the ministry released the ALMM List II for solar cells, listing nine domestic manufacturers with a cumulative annual production capacity of 13,067 MW. Moreover, in September 2025, the MNRE proposed to issue ALMM List III for solar wafers, which will come into effect from June 1, 2028.

Segment-wise developments

Ground-mounted solar

Over the past few years, utility-scale solar has shown consistent and promising growth, driven by strong investors, an enthusiastic developer base, timely regulatory interventions, favourable cost economics, and a transparent and competitive bidding mechanism. The solar energy landscape remained dynamic in 2025, marked by several tender bids, auctions and project commissionings.

In January 2025, THDC India invited bids to set up 100.1 MW ground-mounted solar projects at Karnataka Power Corporation’s thermal projects in Bellary and Raichur in the state. In February 2025, the Solar Energy Corporation of India (SECI) launched a tender for 500 MW of interstate transmission system (ISTS)-connected solar projects under Tranche XIX. Moreover, Singareni Collieries Company Limited (SCCL) floated two tenders in March 2025 to develop solar projects with a cumulative capacity of 137 MW in Telangana. In July 2025, NHPC Limited invited bids for 1.2 GW of solar projects at the Jalaun Solar Park in Uttar Pradesh. Meanwhile, Coal India Limited invited bids to set up an 875 MW solar project at Rajasthan Rajya Vidyut Utpadan Nigam’s 2 GW Solar Park at Pugal. In September 2025, the Deendayal Port Authority floated a tender for a 1 GW ground-mounted solar project on its coastal land parcel between Chirai and Jangi, Gujarat. Moreover, in October 2025, the Assam Power Distribution Company Limited (APDCL) invited bids for a 15 MW solar project in Assam.

In January 2025, THDC India invited bids to set up 100.1 MW ground-mounted solar projects at Karnataka Power Corporation’s thermal projects in Bellary and Raichur in the state. In February 2025, the Solar Energy Corporation of India (SECI) launched a tender for 500 MW of interstate transmission system (ISTS)-connected solar projects under Tranche XIX. Moreover, Singareni Collieries Company Limited (SCCL) floated two tenders in March 2025 to develop solar projects with a cumulative capacity of 137 MW in Telangana. In July 2025, NHPC Limited invited bids for 1.2 GW of solar projects at the Jalaun Solar Park in Uttar Pradesh. Meanwhile, Coal India Limited invited bids to set up an 875 MW solar project at Rajasthan Rajya Vidyut Utpadan Nigam’s 2 GW Solar Park at Pugal. In September 2025, the Deendayal Port Authority floated a tender for a 1 GW ground-mounted solar project on its coastal land parcel between Chirai and Jangi, Gujarat. Moreover, in October 2025, the Assam Power Distribution Company Limited (APDCL) invited bids for a 15 MW solar project in Assam.

The momentum is further reflected in recent auction outcomes. Since December 2024, five auctions have been conducted. The lowest utility-scale solar tariffs discovered in the tenders ranged from Rs 2.55 per kWh (GUVNL Phase XXV 500 MW and NTPC 1,200 MW in the auction conducted in December 2024) to Rs 3.04 per kWh (SECI’s Tranche XVIII 1 GW auction, conducted in December 2024).

This concerted effort is evident in the recent wave of project commissioning. In August 2025, Sustainable and Affordable Energy for Life Industries Limited commissioned a 200 MW solar project in Jalore, Rajasthan. In September 2025, Adani Green Energy Limited commissioned an 87.5 MW and a 125 MW solar power project at its Khavda site in Gujarat. As of October 2025, further additions have been made, including NTPC Green Energy’s 95.75 MW solar capacity at the Khavda I solar project. Furthermore, SJVN commissioned a part capacity of 128.88 MW at its 1,000 MW Bikaner solar power project. In November 2025, NLC India Limited commissioned a 106 MW part capacity of its 300 MW solar power project at Barsingsar, Rajasthan.

Although these large project auctions and announcements are promising, urgent measures are still needed to ensure their timely and effective implementation. The challenges relating to land acquisition and securing of appropriate land near grid substations must be resolved. Inefficient power procurement and management practices by discoms, along with the risk of power curtailment, must be eliminated. Additionally, the heavy concentration of solar power in specific states could lead to system congestion, impacting grid stability, the ability to quickly despatch energy and the development of the necessary ancillary services for load balancing.

Rooftop solar

According to the MNRE, India added 5.15 GW of rooftop solar capacity in 2024-25, a 72 per cent increase over 2023. The country’s cumulative rooftop capacity has surpassed 20 GW. Policy interventions such as the PM Surya Ghar Muft Bijli Yojana announced in February 2024 and financial subsidies (Rs 130 billion disbursed so far under the scheme) have been instrumental in accelerating adoption. Several industry developments have taken place in this segment, especially after the launch of this scheme.

In February 2025, APDCL invited bids to set up rooftop solar projects with a cumulative capacity of 134 MW across government buildings in the state. In May 2025, Uttar Pradesh New and Renewable Energy Development Agency issued a tender to set up 500 MW rooftop solar projects at government, semi-government and other institutions in Uttar Pradesh. Moreover, in June 2025, NHPC issued a tender for rooftop solar projects with cumulative capacity of 19.2 MW on government buildings in Haryana. In July 2025, Telangana Renewable Energy Development Corporation Limited invited bids for rooftop solar projects with a cumulative capacity of 80.69 MW across 80 villages. Furthermore, the West Bengal State Electricity Distribution Company Limited invited bids in September 2025 for 10 MW of grid-connected rooftop solar projects. Additionally, in October 2025, APDCL invited bids for a cumulative 67 MW of grid-connected rooftop solar projects on government buildings.

However, despite rapid growth and policy support, the rooftop solar segment continues to face several constraints. These include high initial expenses for the residential sector, limited access to affordable financing and the discoms’ complex processes. Moreover, consumer awareness and readiness to embrace these technologies remain low. Concerns over system quality also undermine consumer confidence. Further, even after subsidies, many consumers are unwilling to give up their rooftop space for solar systems. Regulatory challenges such as varying net metering policies across states also impede the growth of this sector.

Floating solar

India’s floating solar journey began in 2015, marking a milestone in substantial development. However, the segment gained significant momentum only in recent years, with a steady rise in tendering activity. The past one year, in particular, witnessed a notable surge in the number of tenders floated, signalling growing investor interest and policy push in this space. In January 2025, SECI, on behalf of SCCL, invited bids for a 10 MW floating solar project in Telangana. In the same month, West Bengal invited bids for a 6 MW floating solar project at the Purulia pumped storage project. In March 2025, SECI invited bids for two grid-connected floating solar projects totalling 2.7 MW with battery storage in Lakshadweep. Moreover, Bihar State Power Generation Company Limited issued a tender in June 2025 for a 10 MW floating solar project at the Durgawati Dam reservoir. Furthermore, the Damodar Valley Corporation issued a tender in August 2025 for a 228 MW floating solar project at Konar Dam in Jharkhand. It also issued a tender in September 2025 for a 14 MW floating solar project at the raw water reservoir of its Mejia Thermal Power Station in West Bengal.

However, the commissioning landscape portrays a more cautious picture. Despite the proliferation of tenders, their rate of conversion into successful auctions and project commissioning remains relatively low. In recent years, only a few auctions have reached completion, such as Madhav Infra Projects securing a 15 MW NTPC-SAIL project in Chhattisgarh (May 2024) and Larsen & Toubro winning a 100 MW SECI project in Jharkhand (March 2024). Earlier, developers such as SJVN Limited, NTPC and Hinduja Renewables won projects in Madhya Pradesh.

Notably, only a handful of projects have been commissioned since 2024-25. These include SJVN’s 90 MW floating solar project at Omkareshwar, Madhya Pradesh, commissioned in August 2024; Tata Power Renewable Energy Limited’s 126 MW project at the same site in November 2024; and a 15 MW floating solar project at the Maroda-1 reservoir of Bhilai Steel Plant in Chhattisgarh, commissioned by a joint venture of Steel Authority of India and NTPC-SAIL Power Company in October 2025. These developments indicate that a significant gap still exists between auction awards and actual project commissioning, highlighting ongoing execution challenges.

To achieve large-scale deployment, several critical hurdles must be overcome. These include a lack of policies and incentives, operations and maintenance hurdles, absence of standardised agreements for water rights, shortage of expertise for the design of floaters, anchoring and mooring systems, higher capital expenditure compared to conventional ground-mounted solar plants and the risk of pollution in water bodies. These issues need to be addressed through adequate research and development, site identification studies, clear policies and regulatory frameworks.

Manufacturing

The domestic manufacturing industry will play a major role going forward, as India aims to reduce its dependence on imports from China and other nations. Several companies have announced or commissioned large solar manufacturing facilities in the past year. For instance, in March 2025, the Avaada Group inaugurated a 1.5 GW solar module manufacturing facility in Dadri, Noida, with a focus on TOPCon N-type bifacial glass-to-glass modules. Furthermore, in April 2025, Reliance Industries commissioned its first solar module manufacturing line in Jamnagar, Gujarat, with an initial capacity of 10 GW per year, which can be expanded up to 20 GW. Additionally, in June 2025, Premier Energies commissioned a 1.2 GW TOPCon solar cell manufacturing line in Telangana. In the same month, Sunkind Energy signed an MoU with ConfirmWare PV Manufacturing Solutions to establish solar module and cell manufacturing units with a cumulative capacity of 4 GW. Meanwhile, Solarium Green Energy announced its re-entry in the solar module manufacturing space with the development of a 1 GW facility in Ahmedabad, Gujarat. Furthermore, INA Solar operationalised its 4.5 GW solar module manufacturing plant in Sawarda village, Jaipur district, Rajasthan. In October 2025, RPSG Solvanta announced the commissioning of its 4 GW solar module manufacturing facility in Greater Noida, Uttar Pradesh.

The way forward

Solar has played a pivotal role in India’s renewable energy sector. While each renewable technology presents its own set of advantages and challenges, the outlook for solar remains highly optimistic. Overall, the healthy project pipeline, backed by a consistent flow of new tenders and bids, underscores this. Government initiatives, supportive regulatory frameworks and investment interest from players are setting the stage for significant expansion. This positive environment will take India closer to its renewable energy goals, making solar a key pillar of the country’s energy transition.