By Sakshi Bansal

The solar energy sector in India is witnessing tremendous growth, driven by a combination of progressive government policies, technological advancements, declining solar panel costs and increased investments. Since 2014, India’s installed solar power capacity has grown significantly, rising from 2.8 GW in 2014-15 to about 92.1 GW in 2024-25 (as of October 2024), according to the Ministry of New and Renewable Energy (MNRE). This translates into a growth rate of 3,189.3 per cent over the decade. Currently, utility-scale solar accounts for the majority of the total installed capacity, contributing around 71 GW. Rooftop solar and off-grid solar projects, though smaller in scale, have added approximately 14.4 GW and 4 GW respectively. The remaining solar capacity, about 2.6 GW, falls under the hybrid solar category.

Over the past year, the sector has witnessed several notable developments, particularly in the residential rooftop solar and off-grid solar segments, which required a significant policy impetus due to their low-capacity increase. Apart from policy announcements, several solar auctions were held in the utility-scale space, witnessing competitive tariffs. In addition, the floating solar segment gained significant industry interest in the past year, with several projects commissioned

and planned.

Another highlight has been the growing investments in solar manufacturing, driven by the government’s proactive policymaking, with several companies setting up their facilities in the past year. Despite these positives, the sector also experienced uncertainty around the Approved List of Models and Manufacturers (ALMM) policy, which was eventually resolved.

An overview of the recent policy developments, tender auctions and key trends across major solar subsegments, as well as the outlook for the future…

Policy developments

In light of the growing importance of rooftop solar, floating solar and off-grid solar, various policy measures have been introduced to support the goal of achieving 280 GW of solar capacity by 2030.

Solar pumps

In January 2024, the government amended the implementation guidelines for the PM-KUSUM scheme. The key amendment was the expansion of the scheme with revised targets to solarise 4,900,000 pumps under Components B and C. Several other amendments were introduced to simplify the policy and promote uptake. For instance, the guidelines were revised to simplify the land aggregation process in Component C. In addition, the mandatory state share provision was removed and the exemption of the domestic content requirement under Component C was extended until March 31, 2024. Moreover, individual farmers in the north-eastern states, hilly states/union territories (UTs) and island UTs are now eligible for central financial assistance (CFA) for pump capacities of up to 15 HP, a significant increase from the previous limit of 7.5 HP. Additionally, farmers involved in cluster or community irrigation projects in high-water-table areas across all states/UTs are also eligible for this assistance. The requirement for performance bank guarantees in Component A and Component C (feeder-level solarisation) has been relaxed.

Off-grid solar

In January 2024, the President of India granted approval to the MNRE for the execution of a new solar power initiative in the off-grid solar space. With a budget of Rs 5.15 billion, this programme is designated for habitations and villages of particularly vulnerable tribal groups (PVTGs) under the Pradhan Mantri Janjati Adivasi Nyaya Maha Abhiyan (PM JANMAN). The objective of the initiative is to provide electricity to 100,000 households belonging to PVTGs in regions where grid-based electricity supply is not considered technologically and economically viable. This is intended to be achieved through the installation of 0.3 kW off-grid solar power systems. In addition, the initiative involves arrangements for solar lighting at 1,500 multi-purpose centres (MPCs) located in PVTG areas, where grid-based electricity is not accessible. The government is set to allocate Rs 100,000 per MPC, with a designated budget of Rs 150 million. The programme saw some revisions in October 2024. As per the revisions, it will be implemented under PM JANMAN and Pradhan Mantri Janjatiya Unnat Gram Abhiyan (PM JUGA). It has an additional budget of Rs 9.15 billion now. The revised programme includes the solarisation of 2,000 public institutions, as approved under PM JUGA. The programme approvals under PM JANMAN from the previous phase will be integrated into the updated scheme.

Rooftop solar

In February 2024, the government launched the PM Surya Ghar Muft Bijli Yojana (PMSGY). The scheme, with a total outlay of Rs 750 billion until 2025-26, aims to provide free electricity of up to 300 units every month to 10 million households across the country. Furthermore, in May 2024, the ministry established a mission directorate to execute the scheme to ensure its objectives are met and manage daily operations. In June 2024, in order to facilitate multistate vendor registrations on the national portal for the residential rooftop solar programme, the MNRE announced that vendors will now have the option for multistate registration in addition to national registration. In the same month, the ministry released operational guidelines for implementing the scheme’s CFA component targeted at residential consumers. In July 2024, the MNRE issued guidelines for implementing the “Incentives to DISCOMs” component under the PMSGY. Discoms will be responsible for ensuring net meter availability, and timely inspections and commissioning. The total budget for this component is Rs 49.5 billion, incorporating provisions from the previous Grid Connected Rooftop Solar Phase II programme. In the same month, the ministry allocated Rs 10 billion to incentivise rooftop solar installations. For each installation, the urban local bodies and panchayati raj institutions will receive an incentive of Rs 1,000.

Furthermore, in August 2024, the ministry released new guidelines for the model solar village component under the scheme. While the overall scheme is aimed at installation of solar panels on residential rooftops, this component aims to create one model solar village in every district of the country. The total budget outlay for this component is Rs 8 billion. Each model village will receive Rs 10 million as CFA. In October 2024, the ministry notified scheme guidelines for implementing “innovative projects” under the scheme. For this, Rs 5 billion has been set aside to encourage advancements in rooftop solar technologies, business models and integration techniques.

ALMM

The ALMM policy underwent several reversals over the past year. It was suspended in March 2023, which allowed solar projects commissioned by March 2024 to bypass ALMM compliance. Yet, on February 9, 2024, the government reintroduced ALMM requirements for solar PV modules, effective April 1, 2024, with some exemptions for open access and captive power projects in advanced construction stages or with orders placed before March 31, 2024. Subsequently, on February 15, 2024, the MNRE reversed its decision again, suspending the ALMM until further notice. Finally, in March 2024, the MNRE announced that the ALMM would be reinstated from April 1, 2024, without any exemptions. In September 2024, the ministry issued a draft amendment to the ALMM List-II for solar PV cells, effective from April 1, 2026, to accommodate the expected increase in solar PV cell capacity.

Segment-wise developments

Ground-mounted solar

Over the past few years, utility-scale solar has shown consistent and promising growth, driven by strong investor and developer confidence, timely regulatory interventions and favourable cost economics. The solar energy landscape remained dynamic in 2024, marked by several commissioned projects, auctions, tender bids and major announcements from companies outlining key plans and important MoUs. In December 2023, Rays Power Infra Limited signed an MoU with the Uttarakhand government to establish a 500 MW solar park in the state, and NTPC Limited invited bids for 1.5 GW of interstate transmission system-connected solar projects. In February 2024, Adani Green Energy Limited (AGEL) commissioned 551 MW of solar capacity in Gujarat. In the same month, Uttar Pradesh Power Corporation Limited invited bids for 2 GW of grid-connected solar projects to be located anywhere in India. Meanwhile, SJVN Limited commenced operations at the 100 MW Raghanesda solar power station in Banaskantha district of Gujarat. In March 2024, AGEL commissioned a 180 MW solar power plant at Devikot, Rajasthan. In April 2024, TP Saurya Limited announced the effective initiation of a 200 MW solar project in Bikaner, Rajasthan.

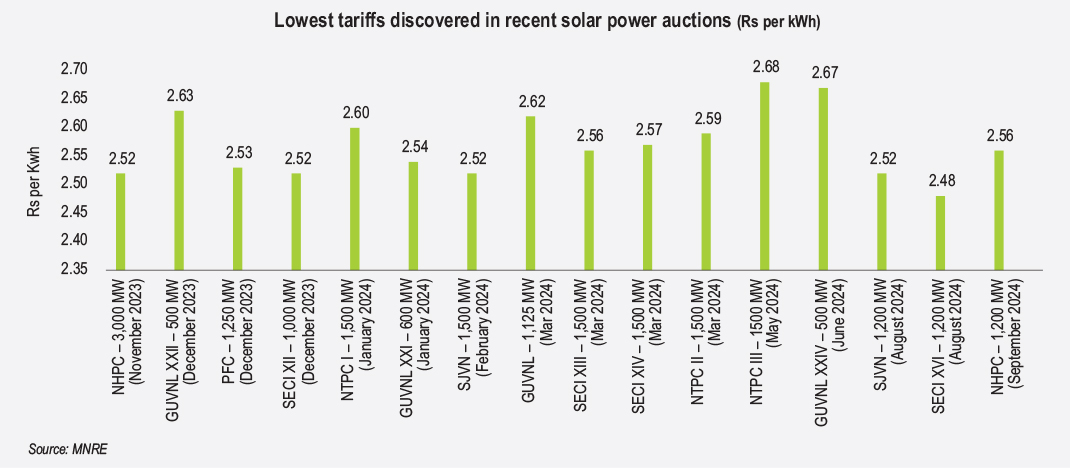

Furthermore, Renewable Watch Research tracked 16 solar power auctions between November 2023 and October 2024, with the lowest tariffs ranging from Rs 2.48 per kWh to Rs 2.68 per kWh. The lowest tariffs were discovered in Solar Energy Corporation of India Limited (SECI) Tranche XVI 1,200 MW auction, conducted in August 2024. In this auction, Sustainable and Affordable Energy for Life Industries Limited and NTPC Limited secured 250 MW and 200 MW respectively, by quoting a tariff of Rs 2.48 per kWh each. Meanwhile, BluPine Energy quoted a tariff of Rs 2.49 per kWh and won 50 MW in this auction. In NTPC’s May 2024 auction to develop 1,500 MW of grid-connected solar power projects (Phase III), Apraava Energy won 50 MW by quoting the lowest tariff of Rs 2.68 per kWh (upper range of the L1 tariffs bid during the year). While Avaada Energy won 750 MW, JSW Energy secured 400 MW and ReNew 300 MW by quoting a tariff of Rs 2.69 per kWh each in this auction. Additionally, auctions held during this period in Gujarat saw tariffs ranging from Rs 2.54 per kWh to Rs 2.72 per kWh. In the auctions conducted by various central PSUs, tariffs ranged from Rs 2.52 per kWh to Rs 2.69 per kWh.

Furthermore, in August 2024, NTPC commissioned a 160 MW solar project in Rajasthan as part of its 320 MW Bhainsara solar project. In September 2024, BluPine Energy commissioned its first 120 MW solar project in Gujarat. It comprises a 70 MW plant at Radhanpur and a 50 MW plant at Nenava. In October 2024, Global Energy Alliance for People and Planet expressed interest in collaborating with the Uttar Pradesh Expressways Industrial Development Authority to develop a 450-500 MW solar park on the Bundelkhand expressway.

Although these large project auctions and announcements are promising, urgent measures are still needed to ensure their timely and effective implementation. The challenges related to land acquisition and securing appropriate land near grid substations must be resolved. Inefficient power procurement and management practices by discoms, along with the risk of power curtailment, must be eliminated. The dependence on imports for critical minerals poses risks to domestic production, which must be addressed. Additionally, the heavy concentration of solar power in specific states could lead to system congestion, impacting grid stability, the ability to quickly despatch energy and the development of the necessary ancillary services for load balancing.

Rooftop solar

The rooftop solar market in India encompasses the residential, C&I and government sectors. However, the adoption of rooftop solar in the residential sector has been significantly slower than in the C&I sector. The government announced the PMSGY in February 2024 to accelerate rooftop solar installations. The government has set up approximately 400,000 rooftop solar connections so far, contributing to around 1.8 GW of new residential rooftop solar capacity, which accounts for more than half of India’s total, in just six months. Several industry developments took place in this segment, especially after the launch of

the scheme.

In December 2023, the Uttar Pradesh New and Renewable Energy Development Agency invited bids to develop grid-connected rooftop solar projects aggregating 500 MW, the biggest tender bid for the year. In March 2024, Mahatma Phule Renewable Energy and Infrastructure Technology Limited (MAHAPREIT) issued a tender for 400 MW of grid-connected rooftop solar projects in Maharashtra. In July 2024, Godrej Electricals and Electronics commissioned a 12.5 MWp rooftop solar project for a textile facility in Madhya Pradesh. In October 2024, MAHAPREIT floated a tender for 30 MW of distributed grid-connected rooftop solar systems on government buildings in Goa.

Moreover, driven by robust support from the Indian government, the rooftop solar financing space also saw positive movement. In March 2024, Tata Power Solar Systems Limited declared the continuation of its collaboration with the Union Bank of India to provide financial solutions to residential customers in line with the government’s PMSGY, as well as to C&I customers. In May 2024, Orb Energy and the State Bank of India (SBI) entered into a partnership as part of SBI’s Surya Shakti Solar Finance scheme. In July 2024, the Asian Development Bank sanctioned loans worth $240.5 million to SBI and the National Bank for Agriculture and Rural Development for financing rooftop solar systems in India. In October 2024, Insolation Energy Limited secured a contract worth Rs 5 billion from Rajasthan Renewable Energy Corporation Limited for the installation of 77 MW of rooftop solar plants in Rajasthan.

Despite these advancements, rooftop solar continues to face challenges. One key issue is the limited availability of domestic content requirement modules in the residential sector, given the substantial gap between India’s PV cell and module manufacturing capacities. There are also concerns about the adoption of the scheme by its intended target group, which consists of small- to medium-scale electricity consumers. The cost structure and access to financing still predominantly benefit wealthier and more creditworthy residential consumers.

Floating solar

Floating solar provides a flexible solution to land acquisition challenges and helps conserve water by reducing evaporation. Different studies indicate India’s floating solar potential at 206-280 GW, with Madhya Pradesh, Maharashtra and Karnataka leading the way. Although still in its early stages, the floating solar market in India is growing, with an increasing number of tenders and tariff-based auctions. This segment too witnessed notable activities over the past few months. For example, in December 2024, Rewa Ultra Mega Solar Limited invited bids for setting up three floating solar projects, with a cumulative capacity of 490 MW. In March 2024, Larsen & Toubro won the engineering, procurement and construction contract from the SECI for a 100 MW floating solar project in Jharkhand. In the same month, the Navi Mumbai Municipal Corporation issued a tender to set up a 100 MW floating solar project in Maharashtra. In April 2024, NHPC and Ocean Sun signed an MoU to explore floating solar energy technologies in India. In May 2024, Madhav Infra Projects Limited received the letter of award from NTPC-SAIL Power Company Limited (NSPCL) to set up a 15 MW floating solar project at Maroda Reservoir-I of NSPCL in Bhilai, Chhattisgarh. In August 2024, SJVN Limited commissioned its 90 MW Omkareshwar floating solar project. Moreover, in the same month, a 4.096 MWp floating solar power plant was built for Amplus KN One Power in Awarpur, Maharashtra, by Ciel & Terre India. Recently, in November 2024, Tata Power Renewable Energy Limited commissioned the 126 MW Omkareshwar Floating Solar Project at an investment of

Rs 5.96 billion.

With these developments, the continued growth of floating solar projects is certain, as long as key issues are addressed promptly. These include a lack of policies and incentives, operations and maintenance hurdles, absence of standardised agreements for water rights, shortage of expertise for the design of floaters, anchoring and mooring systems, higher capital expenditure compared to conventional ground-mounted solar plants, and the risk of pollution in waterbodies. These issues need to be addressed through adequate research and development, site identification studies, clear policies and regulatory frameworks.

Manufacturing

The Indian domestic manufacturing industry will play a major role going forward, primarily as India aims to reduce its dependence on imports from China and other nations. The Indian government is supporting this cause with various incentives, tariff and non-tariff barriers. Several companies have also announced or commissioned large solar manufacturing facilities in the past year. For instance, Luminous Power Technologies inaugurated the solar panel factory in Uttarakhand. TPSSL started commercial production of a 2 GW solar cell line in Tamil Nadu. The Avaada Group laid the foundation for a new manufacturing facility at the Butibori Industrial Park in Nagpur. Moreover, Alpex Solar Limited announced plans to manufacture solar cells in Uttar Pradesh. In addition, Adani Solar announced plans to develop a 225 MW solar power manufacturing plant in Puranpura within a year. Gautam Solar also announced its plan to launch and establish a 2 GW solar cell manufacturing plant at an estimated cost of Rs 10 billion. AXITEC inaugurated a new manufacturing plant in Tamil Nadu, with a production capacity of 300 MW. Indosolar Limited announced the inauguration of its new solar module manufacturing plant in Noida’s industrial hub.

Future outlook

Overall, the healthy project pipeline, backed by a consistent flow of new tenders and bids, underscores the solar sector’s growth momentum. Government initiatives, supportive regulatory frameworks and investment interest from players are setting the stage for sustained expansion. This positive environment is expected to propel India closer to its renewable energy goals, making solar a key pillar of the country’s energy landscape.

The government is expected to amend the ALMM policy to include solar cells in the ALMM framework. This change is expected to increase solar cell production capacity, providing a significant impetus to the solar sector. There have been debates among industry stakeholders regarding the increased cost of solar generation when using ALMM-compliant modules. Going forward, ALMM for solar cells may further spark a similar debate. The sector will need to balance these cost concerns with the benefits of increased domestic manufacturing and enhanced product quality.

Another key highlight for next year will be the greater uptake of mono-PERC, Topcon and HJT solar modules, which are gaining traction. In addition, there will likely be an increased emphasis on developing solar-storage hybrid and round-the-clock projects. Scaling up the size of rooftop solar projects for green hydrogen production also offers a promising avenue, particularly in urban and industrial regions where space constraints limit the feasibility of ground-mounted systems. While the government’s recent policy supporting off-grid decentralised solar is a commendable move, effective on-ground implementation will be critical to its success. Looking ahead, it will be interesting to see how these advancements unfold and whether the government lives up to expectations.