India’s power demand has been growing rapidly, keeping pace with economic activity and industrial growth, as well as for meeting its energy needs in the prevailing heatwave. On May 30, 2024, the country met the highest-ever peak demand of 250 GW. Due to its proactive measures, India has performed well in meeting its energy needs with the support of existing thermal and renewable capacities. Renewable energy has been playing a crucial role in meeting power demand during solar hours, while the reliance on thermal power remains high during evening peaks.

Growing power demand

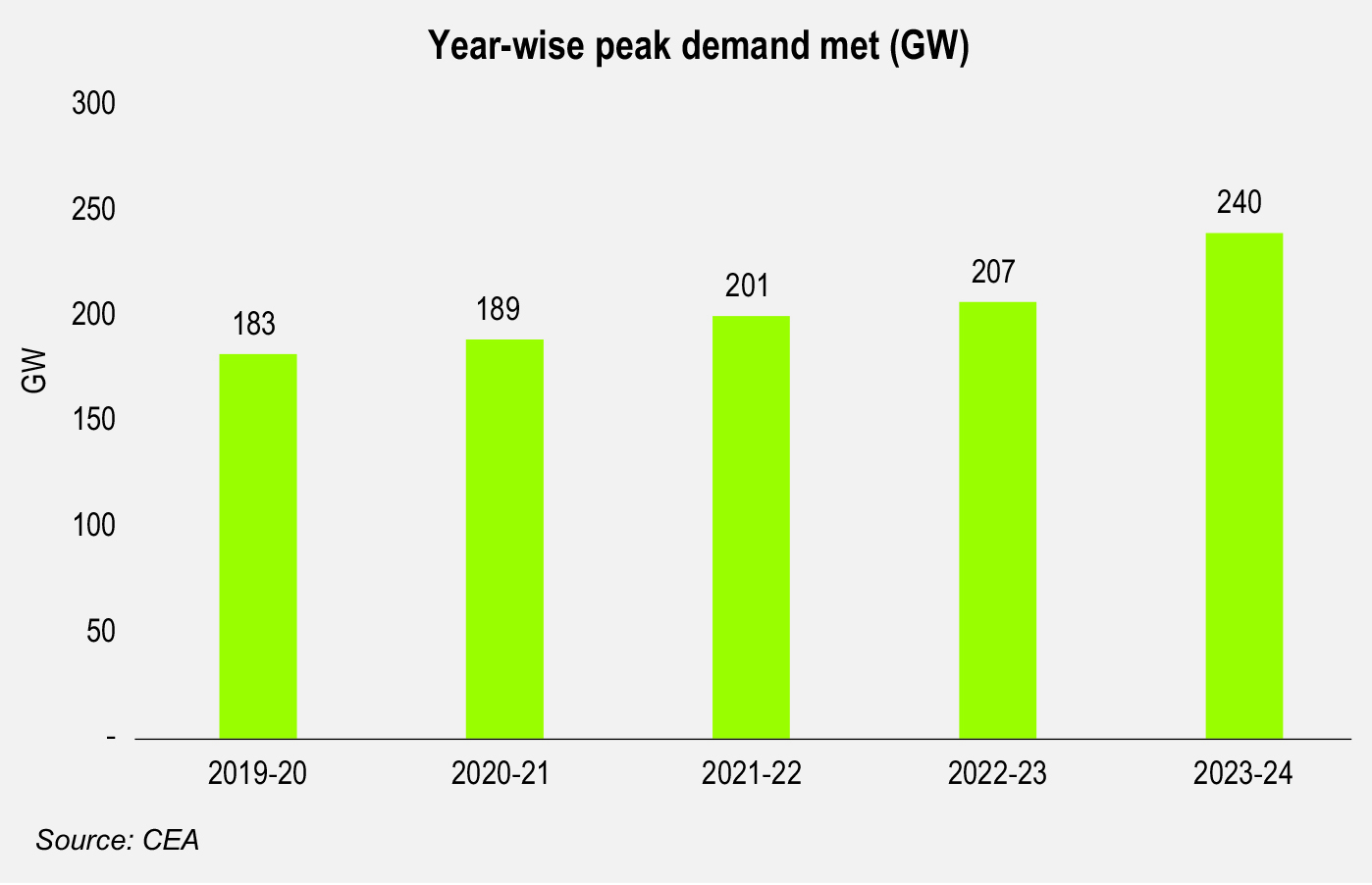

India’s power demand has been growing rapidly year on year. In 2023-24, the power demand stood at 1,622 BUs, recording an increase of 7.8 per cent. Industry experts expect that energy demand growth will remain at about 6-6.5 per cent in 2024-25, surpassing the 10-year historical average. With regard to peak power demand, India recorded the highest-ever peak power demand of 250 GW on May 30, 2024. In 2023-24, the peak power demand was recorded at 240 GW, marking an increase of nearly 16 per cent over that in the previous year. Going forward, as per the 20th Electric Power Survey (EPS) of the Central Electricity Authority (CEA), the peak electricity demand of the country is expected to increase to 334 GW and the electrical energy requirement is expected to increase to 2,279 BUs in 2029-30. During 2022-23 to 2029-30, the compound annual growth rate (CAGR) of peak electricity demand is expected to be 7.09 per cent and the CAGR of the electrical energy requirement is expected to be 6.12 per cent.

The increasing power demand is driven by several factors such as hot weather, resilient economic activity, higher penetration of residential end-use appliances, manufacturing growth and the emergence of new use cases of power such as data centres, electric vehicles and hydrogen in the future. These growth drivers are expected to continue to increase the country’s power demand in the coming years. Vasudha Foundation, in its recent report, “An Outlook of India’s Electricity Demand”, presents a sectoral outlook of power demand up to 2030. The report indicates that the industrial sector will continue to drive the surge in electricity demand, accounting for about 40 per cent of the total electricity demand mix by 2030. Space cooling will account for the largest share of approximately 67 per cent in residential electricity consumption. By 2030, road transport electrification is anticipated to be significantly driven by both private and public transport, creating new electricity demand for the sector and accounting for 3-4 per cent of the total electricity demand.

Notably, the trend in rising power demand is being witnessed globally, and this is expected to continue in the coming years. A recent report by the International Energy Agency notes that while electricity demand grew by 2.3 per cent in 2023 – less than the 2.4 per cent recorded in 2022 – this growth is expected to accelerate over the next three years, with an average annual increase of 3.4 per cent through 2026.

Tapping thermal and renewable power

In the prevailing heatwave conditions, the northern and western regions met a record demand met of 86.7 GW and 74.8 GW respectively. However, the peak demand for the northern region reached a new high of 89 GW on June 17, 2024. Notably, the all-India non-solar demand that was met touched an all-time high of 234.3 GW on May 29, 2024. At the same time, the all-India thermal generation that was met stood at 176 GW (ex-bus) of the peak demand, especially during non-solar hours. The steady and extensive support from thermal plants in meeting the power demand was made possible with the implementation of Section 11 of the Electricity Act, 2003, directing imported coal-based plants to maximise generation and revive gas-based power plants, alongside directives to gencos to schedule maintenance in a way that minimises partial and forced shutdowns. Renewable energy, including solar during solar hours and wind during non-solar hours, complemented thermal generation in meeting the peak demand. An analysis of source-wise power generation on May 30, 2024, as per Grid Controller of India Limited, indicates that thermal generation accounted for 74 per cent of the total generation (thermal and lignite 70 per cent; and gas, diesel and naphtha 4 per cent), while non-fossil fuel-based generation accounted for the remaining 26 per cent (renewable energy sources, including wind, solar and biomass, with 15 per cent; hydropower 9 per cent and nuclear 2 per cent).

Amidst the soaring power demand, a major relief has been the availability of adequate coal stocks at thermal power plants (TPPs). Unlike in the past couple of years, power plants now have reasonable coal stock available due to enhanced coal production and efficient logistics management. To put this in perspective, as of June 16, 2024, coal stocks at TPPs stood at around 45 million tonnes (mt), which is nearly 32 per cent higher compared to the same period in the previous year when it was 34.25 mt. Further, as of June 16, 2024, the cumulative coal production stands at 207.48 mt, reflecting a growth of 9.27 per cent over that in the corresponding period in the previous year, which was 189.87 mt. The cumulative coal despatch stands at 220.31 mt as of June 16, 2024, registering a growth of 7.65 per cent over that in the corresponding period in the previous year, which was 204.65 mt.

Apart from this, power utilities are relying on the power exchanges to meet their energy requirements. The average June 2024 price (in the first 20 days) in the day-ahead market at the Indian Energy Exchange was Rs 5.45 per unit, as against Rs 5.21 per unit in the corresponding period of the previous month. However, reportedly, in June 2024, the duration of power prices hitting the cap of Rs 10 per unit rose to 12 hours a day, up from four hours a month earlier. Further, apart from purchase on the exchanges, discoms are also tying up more for short-term purchases on the DEEP portal compared to last year.

Future outlook

There is a need for policy interventions and reform measures to continue in order to meet the country’s growing power demand. First, while existing thermal and solar capacities have been instrumental in meeting power demand in the ongoing summer season, power capacity needs to keep pace with the growing demand. In the thermal power segment, as per the CEA, coal-based power plants aggregating 31 GW of capacity are under construction, while in the renewable energy segment, around 89 GW of capacity is under construction. The pace of commissioning generation capacity is expected to gain momentum in the coming years. As per ICRA Research, generation capacity addition is expected to reach 30 GW in FY2025 from 25 GW in FY2024. The thermal segment is expected to add 5-5.5 GW capacity in FY2025, with the remaining 25 GW contributed by the renewable energy segment. While the renewable energy segment will remain the key driver of the generation capacity addition, ICRA expects the thermal segment to witness new project announcements going forward, given the healthy demand growth.

Second, in addition to capacity additions in the thermal and renewable energy capacities, augmenting round-the-clock (RTC) power is a must. While adequate solar power meets daytime peak effectively, evening peak power demand needs greater attention. In view of the country’s renewable energy goals and net-zero target by 2070, RTC needs a greater policy push and its share of tenders needs to increase. Notably, tariffs discovered in the recent RTC tenders have been in the range of Rs 4 per unit to Rs 4.50 per unit, highly competitive with the Rs 5.20 per unit discovered in recent medium-term bids for coal-based projects.

Third, large-scale energy storage projects will play a crucial role in meeting the future needs of the country. Since grid demand is lower during the afternoon, grid-scale batteries can store the excess solar generation and supply power during the night/peak demand hours. In the battery energy storage systems (BESS) space, there is a need for proper planning, technological advancements and economies of scale. While there have been noteworthy initiatives to promote the segment, such as the viability gap funding of Rs 37.6 billion, or up to 40 per cent capital cost for private players to set up BESS, there is a need for greater policy support to incentivise investment in the segment.

Fourth, there is a need to deepen the power market. Measures such as introducing capacity markets would allow generators to be compensated for their available capacity, ensuring long-term grid reliability by incentivising investment in generation capacity, particularly for peaking power plants.

Finally, as an immediate measure to meet the country’s rising power demand, the government pulled out all stops and even resorted to expensive gas-based power generation. However, with the upward trajectory of power demand expected to continue, there is a need to augment sustainable and affordable sources of power to meet the future demand.

To conclude, while India has ambitious renewable energy targets and energy transition goals, ensuring uninterrupted power supply is among the top priorities of policymakers and sector stakeholders. What lies ahead is quite interesting as India navigates the energy trilemma of availability, affordability and sustainability.