The compressed biogas (CBG) sector in India is gradually gaining the attention it deserves due to its high potential of 40 mmt. Five states – Uttar Pradesh, Madhya Pradesh, Maharashtra, Punjab and Gujarat – contribute 50 per cent to the total national potential. These states also lead in terms of the number of functional plants and CBG production capacity. India’s significant CBG production potential can be attributed to the availability of surplus feedstock, with animal and poultry waste contributing 38 per cent and agricultural residue 31 per cent.

Given this potential and the available opportunities, the CBG sector has attracted interest from several private and public companies. Overall, as of April 2024, 68 CBG plants and 194 retail CBG outlets have been commissioned, with around 750 plants expected by March 2029. Meanwhile, large urban waste-to-energy (WtE) projects, with a cumulative installed capacity of around 591 MWeq, are producing around 824,647 cubic metres of biogas per day and 450,735 kg of CBG per day.

Policy initiatives

Several policy initiatives have been announced to fully tap India’s CBG potential. The Ministry of New and Renewable Energy (MNRE) announced the National Bioenergy Programme with a budget outlay of Rs 17.15 billion for two phases for the fiscal years 2021-22 to 2025-26. This includes a WtE programme of Rs 6 billion, a biomass programme of 1.58 billion and biogas programme of Rs 1 billion. The incentive for CBG generation from a new biogas plant is Rs 40 million per 4,800 kg per day, while incentive for CBG generation from the existing biogas plant is Rs 30 million per 4,800 kg per day (maximum CFA being Rs 100 million per project). As part of the programme, the MNRE has supported 63 WtE projects, 24 biomass projects and 143 biogas projects so far. In November 2022, the government introduced guidelines for a central financial assistance to bioenergy projects such as non-bagasse, CBG and biogas plants, for the period up to 2025-26.

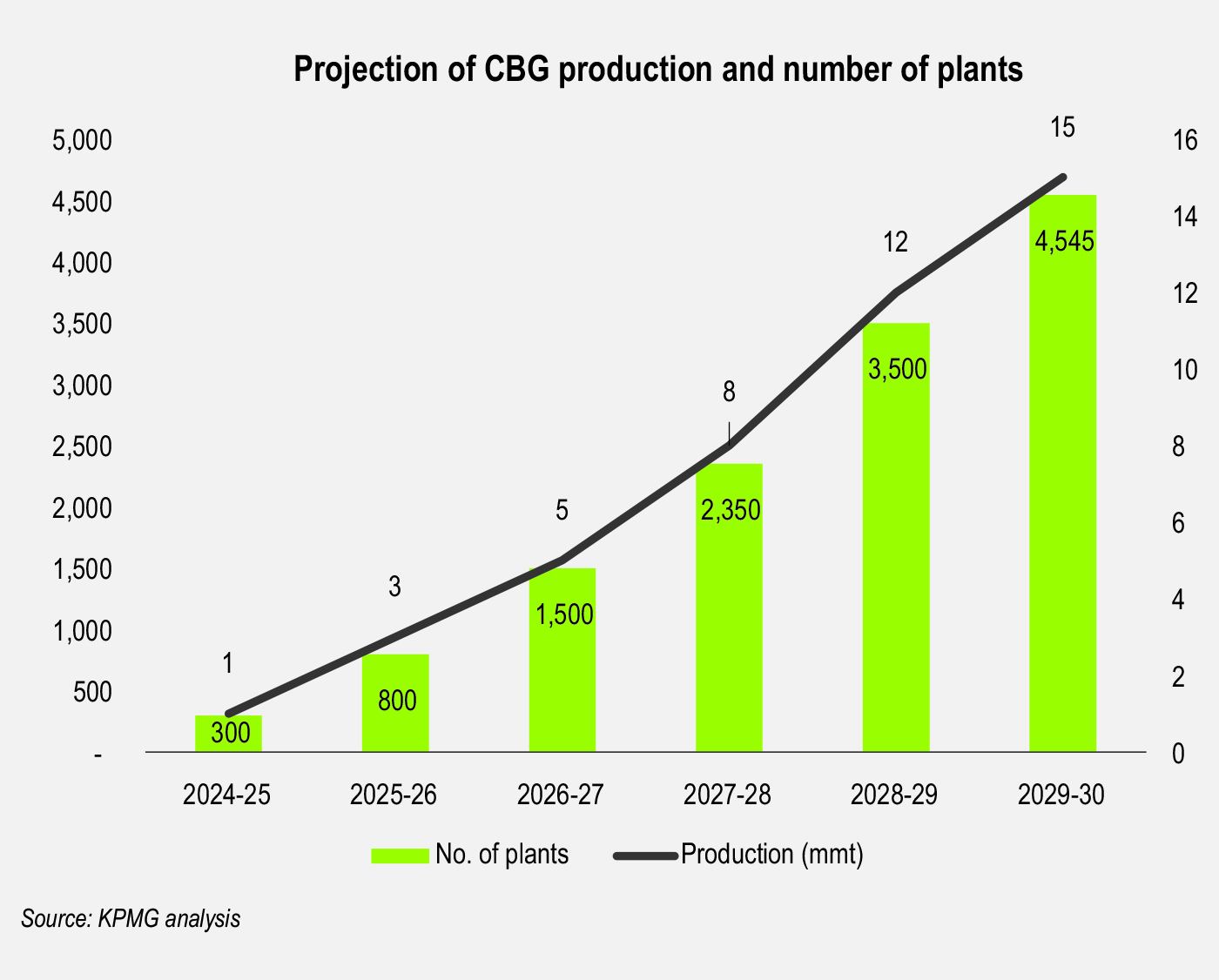

In 2018, the Ministry of Petroleum and Natural Gas (MoPNG) had launched the SATAT (Sustainable Alternative Towards Affordable Transportation) scheme to promote the production and utilisation of CBG as an alternative green fuel for the transport segment and reduce India’s dependence on oil and gas imports by producing CBG using agricultural residues, cattle dung, sugarcane press mud, MSW and sewage treatment plant waste. The MoPNG had set a target of establishing 5,000 CBG plants producing 15 mmt per annum by 2024. As of March 2024, 53 CBG projects have been commissioned under the SATAT initiative.

Further, the government has issued guidelines for blending of domestic gas with compressed natural gas (CNG) for the transport sector and piped natural gas for domestic use in city gas distribution (CGD) networks for the synchronisation of CBG with CNG in the CGD network. Recently, after a long wait, the MoPNG issued guidelines for the development of pipeline infrastructure for injecting CBG into the CGD network. These guidelines outline the incentives available for pipeline infrastructure, as demanded by the CBG industry. The allocated budget for this initiative is Rs 9.945 billion for the fiscal years 2024-25 to 2025-26.

The other key policy initiatives include obligations for blending CBG in the CGD network, introduction of the GOBARdhan scehme, financial assistance for bio-mass aggregation machinery to CBG producers, inclusion of CBG plants in priority sector lending by the Reserve Bank of India.

Uptake in the oil and gas sector

The oil and gas PSUs, particularly Bharat Petroleum Corporation Limited (BPCL) and Oil and Natural Gas Corporation Limited (ONGC), have ambitious plans in the CBG space.

Currently, BPCL has CBG projects at various stages of progress in Kochi, Saharanpur, Bhilai and Mysore. The MoPNG has advised BPCL to establish 195 CBG projects in total. BPCL is planning to set up 26 CBG plants of approximately 50 mtpa in the next two to three years, either through its own investment or through private partnerships. The organisation has prioritised 37 locations and has explored nearly 100 locations. For MSW-based CBG plants, it has submitted request letters to municipal commissioners in 77 locations.

Meanwhile, ONGC has identified 23 plant sites for CBG projects based on agri-residue feedstock and one based on MSW feedstock. Of these, project feasibility reports have been completed for eight locations and a detailed feasibility report has been prepared for one location. Surveys for surplus feedstock availability have been completed for prospective locations in Uttar Pradesh, Andhra Pradesh, Punjab, West Bengal and Madhya Pradesh. One plant, with a CBG production capacity of 1,130 tpd using MSW feedstock, has already been planned.

Challenges and the way forward

One of the major challenges in the CBG sector is the supply chain management of feedstock. Ensuring supply chain assurance and quality consistency remain key concerns for scaling up operations. To address these issues, partnerships with aggregators and diverse feedstock sources are being explored. Paddy straw remains the most difficult feedstock to handle due to inconsistent moisture levels. Going forward, better data on surplus availability at the tehsil level will be required for expansion. Developers also need support for storage infrastructure.

Offtake faces significant hurdles, particularly for medium-scale projects. Marketing both gas and manure is challenging. Current 50 per cent offtake guarantees are insufficient, and the industry recommends 100 per cent offtake guarantees for the first three to four years to support the sector. For pipeline infrastructure, the existing 75 km limit on subsidies is inadequate for plants located far from the grid. Therefore, CBG producers need additional support for transport and marketing for such projects.

Overall, economic viability is currently low for CBG projects due to high set-up costs and operational expenses. Capital costs vary based on feedstock type. MSW plants have high preprocessing set-up costs and liquid digestate issues, costing around Rs 100 million per tpd. The business case is not viable, as it currently relies only on gas revenue. The average offtake price is about Rs 65 per kg.

Developers need to ensure a second revenue source by selling fermented organic manure, which faces significant challenges in meeting moisture content specifications and marketing. A third revenue source from the sale of carbon credits is also crucial going forward. This requires the development of the Indian carbon credit system. The sale of carbon credits could supplement gas and manure revenues, making the overall business model more viable.

Net, net, the CBG market in India holds immense promise, but several issues need to be addressed to achieve the sector’s full potential.

Based on remarks and presentations at Renewable Watch’s Compressed Biogas in India conference