By Nidhi Dua

By Nidhi Dua

Punjab’s power sector reflects the unique characteristics of an agriculture-driven economy, where electricity demand witnesses a sharp seasonal surge during the paddy procurement and irrigation months. Over the years, the state has steadily expanded its power infrastructure to keep pace with rising consumption while also increasing the share of cleaner energy sources in its energy mix.

According to the Central Electricity Authority (CEA), as of April 2026, Punjab’s total installed power capacity stood at 14,769.81 MW, with thermal power contributing 8,364 MW and nuclear power accounting for 229.09 MW. According to data from the Ministry of New and Renewable Energy (MNRE), the state’s installed renewable energy capacity reached 3,458.18 MW as of May 2026. This installed renewable energy capacity comprises 176.1 MW of small hydro, 582.59 MW of biopower, 1,096.30 MW of large hydro, and 1,603.19 MW of solar power.

Punjab’s solar portfolio includes 886.77 MW of ground-mounted solar, 599.8 MW of rooftop solar installations (including those under the PM Surya Ghar: Muft Bijli Yojana) and 117.02 MW off-grid capacity under Component B of the Pradhan Mantri Kisan Urja Suraksha evam Utthan Mahabhiyan (PM-KUSUM). The state’s biopower capacity constitutes 299.5 MW of biomass power/bagasse cogeneration, 237.79 MW of non-bagasse biomass cogeneration, 10.75 MW of waste-to-energy (WtE) and 34.55 MW of off-grid WtE components.

With its strong agricultural base, abundant availability of crop residue, and extensive network of rivers, Punjab is increasingly positioning itself as a key state for compressed biogas projects, decentralised solar applications and small-hydro projects. Renewable Watch takes a look at recent developments across renewable energy segments, and the state’s future outlook…

Surplus biomass waste to produce CBG, reduce stubble burning

Surplus biomass waste to produce CBG, reduce stubble burning

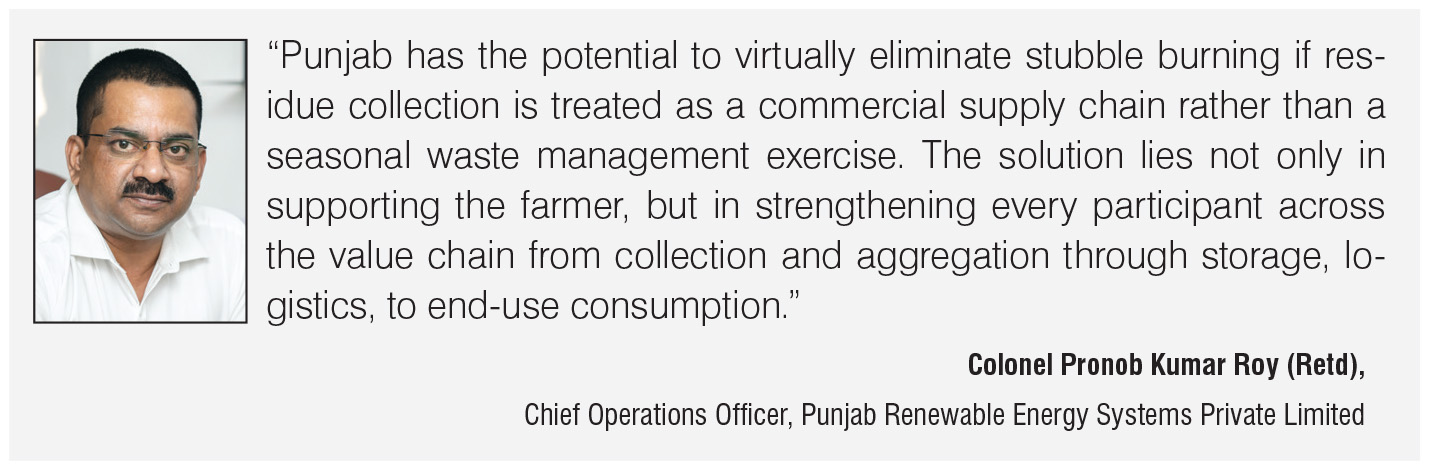

The state’s surplus agricultural residue has immense potential for clean energy applications. However, it also leads to extensive stubble burning in the winter months. Therefore, making efficient procurement and utilisation of biomass is crucial for the state. According to Col Pronob Kumar Roy (Retd), chief operations officer, Punjab Renewable Energy Systems Private Limited, the state generates approximately 19.3 million tonnes (mt)-19.5 mt of paddy straw and over 20 mt of wheat straw per annum. While wheat straw is primarily utilised for fodder, paddy straw remains the principal agricultural residue available for energy applications.

Over the past few years, the state has increasingly shifted towards utilising agricultural residue as an economic resource rather than treating it solely as waste. “The utilisation of paddy straw for energy has grown steadily through biomass power plants, compressed biogas (CBG) facilities, industrial boilers, pellet manufacturing units, briquetting plants, and other thermal applications. Moreover, biomass power projects in Punjab currently account for an estimated consumption of nearly 1 mt of paddy straw annually,” says Col Roy.

The growing utilisation of crop residue has also coincided with a significant decline in stubble-burning incidents. According to government sources, Punjab has recorded a steady reduction in paddy stubble burning under the Commission for Air Quality Management’s (CAQM) coordinated framework to curb farm fires in the region. During the paddy harvesting season of 2025, the state recorded the lowest number of farm fire incidents at 5,114. This marked a decline of 53 per cent compared to 2024, 86 per cent over 2023, 90 per cent over 2022 and 93 per cent over 2021. Fire counts declined consistently, dropping from 71,304 incidents in 2021 to 49,922 in 2022, 36,663 in 2023, 10,909 in 2024 and 5,114 in 2025.

“Punjab has the potential to virtually eliminate stubble burning if residue collection is treated as a commercial supply chain rather than a seasonal waste management exercise. The solution lies not only in supporting the farmer, but in strengthening every participant in the value chain from collection and aggregation through storage, logistics, to end-use consumption,” says Col Roy.

Meanwhile, Punjab is witnessing growing investments in the bioenergy segment. According to the GOBARdhan portal, the state had 93 registered CBG/bio-compress natural gas plants as of May 2026. Of these, 11 plants have been commissioned, 12 are under construction, and 70 are yet to begin construction. The sizeable project pipeline highlights Punjab’s increasing focus on converting paddy straw and other agro-residues into clean energy and biofuels.

In addition, the state has 27 registered biogas plants, of which 24 are operational, while two are under construction and one is yet to commence construction, as per the GOBARdhan portal data. These plants are spread across 20 districts, covering nearly 87 per cent of Punjab’s districts, indicating a relatively broad geographical spread of biogas adoption across the state.

Rooftop solar, solar pumps, canal-top

solar projects

Punjab possesses an abundant, consistent solar resource; however, its utilisation remains constrained by the limited availability of non-agricultural and non-arable land. This necessitates planned and innovative approaches – such as rooftop solar, solar pumps and canal-top solar projects – to overcome space limitations, though the overall uptake in the sector has been slow.

The state has witnessed a moderate uptake in the rooftop solar segment under the PM Surya Ghar scheme. According to the scheme’s website, the state received 24,283 applications, of which 14,070 installations had been completed, covering 16,184 households. This translates into a conversion rate of 57.94 per cent. Punjab’s cumulative installed capacity under the scheme stands at 62.09 MW, while subsidy disbursements amount to Rs 947.4 million.

The state has witnessed a moderate uptake in the rooftop solar segment under the PM Surya Ghar scheme. According to the scheme’s website, the state received 24,283 applications, of which 14,070 installations had been completed, covering 16,184 households. This translates into a conversion rate of 57.94 per cent. Punjab’s cumulative installed capacity under the scheme stands at 62.09 MW, while subsidy disbursements amount to Rs 947.4 million.

Meanwhile, Punjab has demonstrated mixed performance under the PM-KUSUM scheme. Under Component B, which focuses on standalone solar-powered agricultural pumps, 18,048 pumps were sanctioned in the state, of which 17,920 had already been installed as of May 2026, reflecting a high implementation rate. This component is particularly significant for Punjab due to its agrarian economy and high dependence on groundwater-based irrigation. Under Component C (Individual Pump Solarisation), however, the state has shown relatively limited progress. As per the latest PM-KUSUM data, 186 pumps had been sanctioned under the component, of which only 25 had been solarised.

Furthermore, it currently has around 20 MW of operational canal-top solar capacity, developed primarily under the MNRE’s pilot-cum-demonstration programme and implemented by the Punjab Energy Development Agency (PEDA). These projects are installed over major irrigation canals such as the Ghaggar and Sidhwan canals. The projects were designed to address Punjab’s land constraints by utilising canal surfaces for solar power generation while simultaneously reducing water evaporation losses. The state is now planning a significant expansion of canal-top solar infrastructure. In September 2025, Punjab invited expressions of interest for the development of 40 MW of canal-top solar PV projects. Spearheaded by PEDA, the initiative will follow a build-own-operate model to increase clean energy generation while addressing land acquisition constraints in the state.

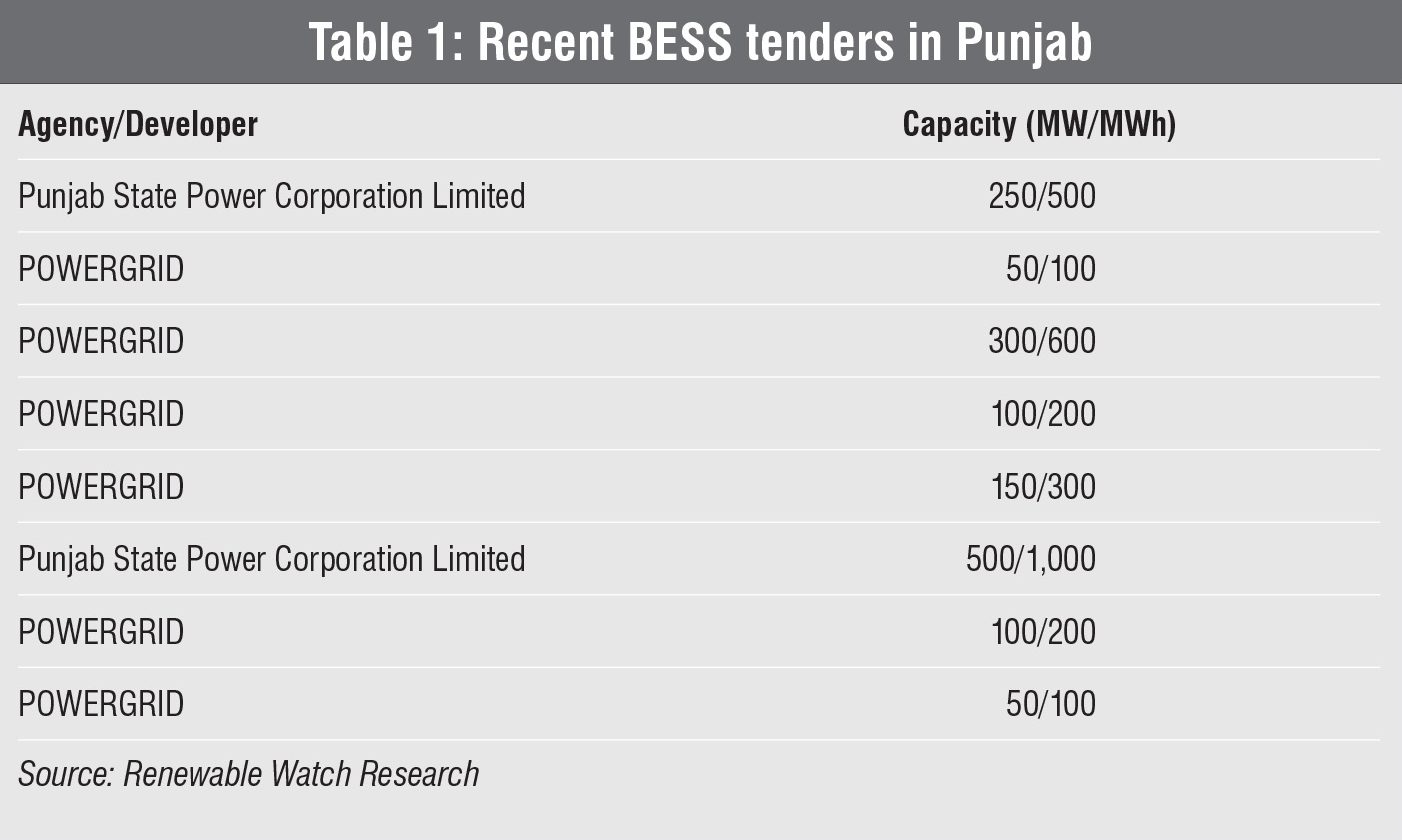

BESS activity gains momentum

Punjab has been actively expanding its energy storage infrastructure, with increasing focus on both battery energy storage systems (BESSs) to support renewable energy integration and grid stability. According to the CEA, the state’s installed energy storage capacity is projected to reach 2,812 MW by 2034-35. Punjab has also witnessed an increase in BESS tendering activity in recent months. As evident from Table 1, Punjab released eight standalone BESS tenders between January 2026 and March 2026, with a cumulative capacity of 1,500 MW/3,000 MWh. These tenders were floated by Punjab State Power Corporation Limited (PSPCL) and Power Grid Corporation of India (POWERGRID).

In a major development, PSPCL announced the results of its 500 MW/1,000 MWh standalone BESS auction in May 2026. The projects were awarded under bucket-filling mechanism. Stockwell Solar secured 150 MW/300 MWh capacity at a tariff of Rs 335,000 per MW per month. Rama Reflection India won 250 MW/500 MWh at a tariff of Rs 344,000 per MW per month, while Ceigall India secured 100 MW/200 MWh at the same tariff. The tender for the projects had been issued in January 2026. The growing tendering activity reflects Punjab’s increasing emphasis on energy storage deployment to manage renewable energy intermittency, support peak demand management and strengthen grid reliability as the state accelerates its clean energy transition.

Hydropower prospects

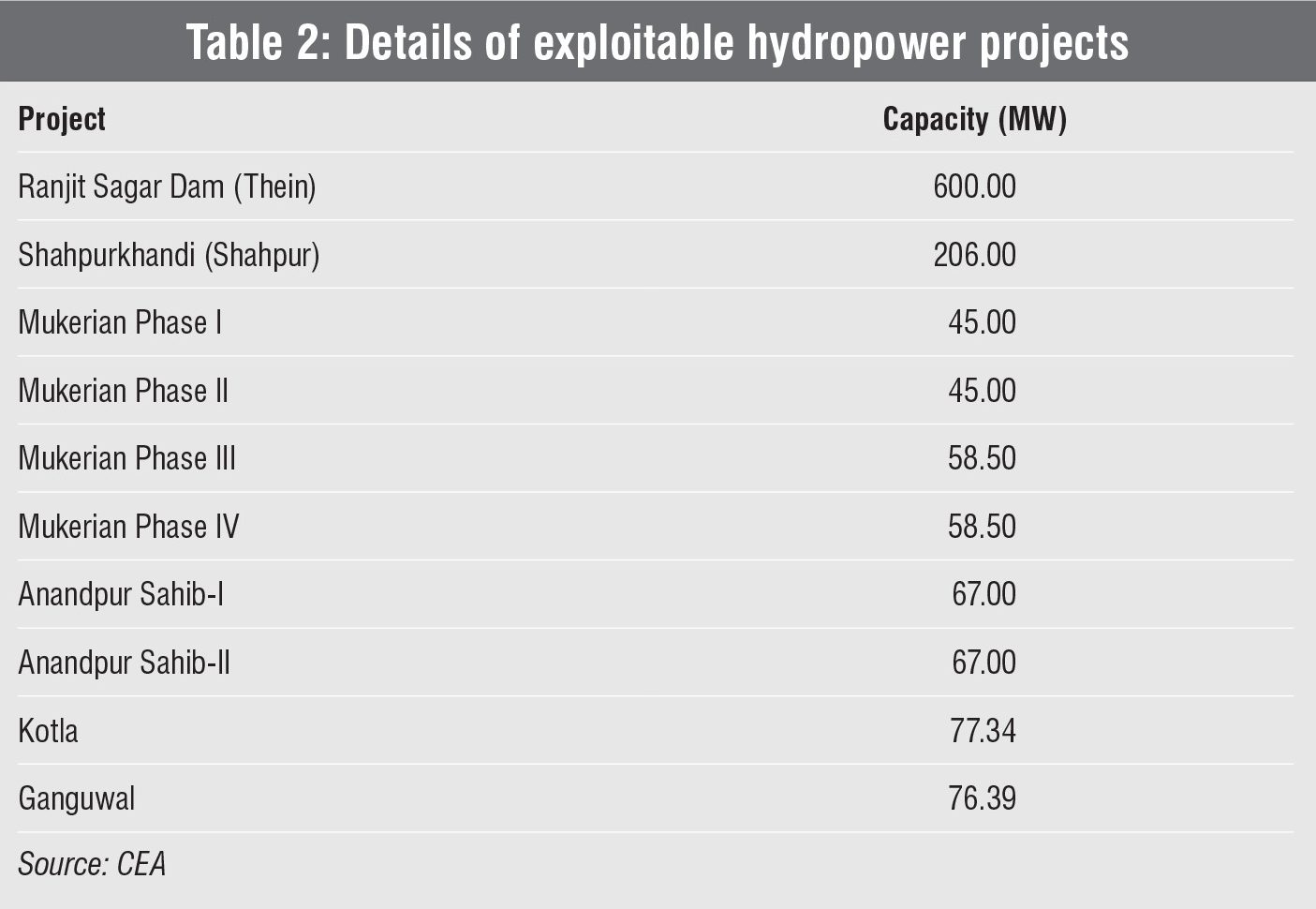

Punjab has significant hydropower potential. According to a CEA study for the 2017-23 period, the state’s exploitable hydropower potential from projects above 25 MW stood at 1,300.73 MW across 10 projects. The details of these projects are highlighted in Table 2.

As of April 2026, Punjab had a total installed hydropower capacity of 1,096.3 MW across nine operational projects. These are – Ranjit Sagar (600 MW), Anandpur Sahib-I (67 MW), Anandpur Sahib-II (67 MW), Mukerian-I (45 MW), Mukerian-II (45 MW), Mukerian-III (58.5 MW), Mukerian-IV (58.5 MW), Ganguwal (77.65 MW), and Kotla (77.65 MW). Most of these projects are run-of-the-river projects, while Ranjit Sagar is a storage-based project. All projects are located within the Indus basin. Additionally, the state has one hydropower project under construction as of April 2026. The 206 MW Shahpurkandi hydroelectric project, located on the Ravi river in Pathankot district, is being implemented by the Irrigation Department and PSPCL. This state sector storage-based project is expected to be completed by May 2027, and commissioned in 2027-28.

Renewable steam set to decarbonise industries

Renewable steam is emerging as a key segment in the state government’s efforts to decarbonise industries. It directly addresses thermal energy demand, which accounts for a significant share of industrial energy consumption. Key sectors demonstrating growing interest in renewable steam solutions in Punjab include textiles, food processing, breweries, dairy processing, pharmaceuticals, chemicals, packaging, and paper and pulp.

“A rising number of industrial units are evaluating biomass-fired boilers, steam-at-cost arrangements, and build-own-operate-transfer (BOOT) models to reduce their dependence on fossil fuels,” says Col Roy. The economics of renewable steam projects have also evolved considerably in recent years. The key cost components of renewable steam projects include biomass procurement, collection, baling and loading, storage and inventory management, transportation, fuel processing and densification, boiler and utility infrastructure capital expenditure, operations and maintenance expenditure, manpower costs and working capital requirements, and environmental and compliance-related expenditure. Among these, feedstock cost, transportation distance, storage efficiency, boiler performance, and annual utilisation levels remain the most critical drivers influencing project viability and overall economics,” says Colonel Roy.

Furthermore, to cater to varying customer requirements and risk-sharing preferences, renewable steam projects are being deployed under multiple business models. These include the fuel supply model, the operations and maintenance model, the steam-at-cost model, and the BOOT model. Colonel Roy explains, “Over time, the market has gradually moved away from simple fuel supply arrangements towards integrated utility service models that offer greater cost certainty, operational reliability and sustainability benefits.”

State of the sector

Punjab’s power sector continues to be shaped by a highly subsidised consumption structure, particularly in the agricultural segment. Agriculture remains one of the largest consumers of electricity in the state. As per the Punjab Economic Survey 2026-27, it accounted for over 30 per cent of the total electricity sales in 2011-12 and represented 24 per cent in 2021-22, significantly above the national average of 20 per cent. The state has maintained its policy of providing free electricity to farmers, with Rs 77.15 billion allocated towards agricultural power subsidies in 2025-26. Simultaneously, Punjab’s industrial growth strategy has relied heavily on power-related incentives. Under the Industrial and Business Development Policy 2022, the state has offered substantial fiscal support through electricity duty exemptions and power tariff subsidies. Since 2022, over Rs 92.74 billion has been released towards subsidised power tariffs to enhance industrial competitiveness.

Punjab’s power sector continues to be shaped by a highly subsidised consumption structure, particularly in the agricultural segment. Agriculture remains one of the largest consumers of electricity in the state. As per the Punjab Economic Survey 2026-27, it accounted for over 30 per cent of the total electricity sales in 2011-12 and represented 24 per cent in 2021-22, significantly above the national average of 20 per cent. The state has maintained its policy of providing free electricity to farmers, with Rs 77.15 billion allocated towards agricultural power subsidies in 2025-26. Simultaneously, Punjab’s industrial growth strategy has relied heavily on power-related incentives. Under the Industrial and Business Development Policy 2022, the state has offered substantial fiscal support through electricity duty exemptions and power tariff subsidies. Since 2022, over Rs 92.74 billion has been released towards subsidised power tariffs to enhance industrial competitiveness.

The state’s power distribution sector has historically performed better than that of many states in terms of operational efficiency. As shown in Table 3, AT&C losses declined significantly from 18.54 per cent in 2021 to 10.96 per cent in 2024. However, losses increased sharply to 19.21 per cent in 2025. Billing efficiency remained relatively stable during the period, ranging between 87 per cent and 89 per cent, while collection efficiency consistently remained strong, peaking at 100 per cent in 2023 before declining to 92 per cent in 2025. The state’s power sector continues to face pressure from high subsidy commitments to agriculture and industry. These commitments place a substantial burden on public finances, underscoring the need for sustained efficiency improvements and financial reforms.

The way forward

Bioenergy is expected to take centre stage in Punjab’s energy transition; however, legacy issues remain. A key challenge is the underutilisation of the total agricultural residue in organised energy applications. Thus, going forward, efficient feedstock management, aggregation, storage and transportation will be paramount.

“Feedstock management remains the primary challenge for Punjab’s biomass and CBG sectors. Paddy straw is generated within a limited harvesting window, whereas CBG plants and other biomass-consuming facilities require a consistent year-round supply of feedstock. This creates a need for extensive infrastructure for aggregation, densification, storage, and inventory management,” says Colonel Roy.

He adds that operational projects continue to face several challenges, including seasonal feedstock availability, high working capital requirements for biomass procurement and storage, moisture management issues, dry matter losses during long-term storage, fire risks and inadequate storage infrastructure. Transportation economics is becoming challenging as procurement radii expand, while competition for biomass is intensifying from industrial boilers, biomass power plants, pellet manufacturers and other energy users. In addition, the availability of skilled aggregation and logistics partners at scale, along with maintaining consistent feedstock quality and contamination control, remain key concerns.

“Going forward, the greatest opportunity lies beyond electricity generation in applications such as renewable steam, CBG, pellets, briquettes, biochar, and other bio-based products. Realising this potential will require continued investment in biomass aggregation infrastructure, storage systems, market linkages and long-term demand creation mechanisms. Strengthening these areas can facilitate the transition from residue disposal to residue utilisation, creating significant environmental and economic value while supporting Punjab’s broader clean energy and sustainability objectives,” says Colonel Roy.