India’s electric vehicle (EV) market is experiencing substantial growth, with a notable surge in EV sales over the past two years. Specifically, electric two-wheeler sales have increased by 41 per cent and electric three-wheeler sales have increased by 200 per cent from 2022 to 2023. Moreover, the combined sales of EVs in these segments are expected to reach 80 per cent by 2030.

This growth can be largely attributed to government subsidies under the Faster Adoption and Manufacturing of Electric Vehicles Scheme (FAME I and II), registration and road tax waivers in some states, and subsidised electricity tariffs, which have led to the total ownership cost of EVs coming closer to or being at par with their internal combustion engine (ICE) counterparts in many use cases.

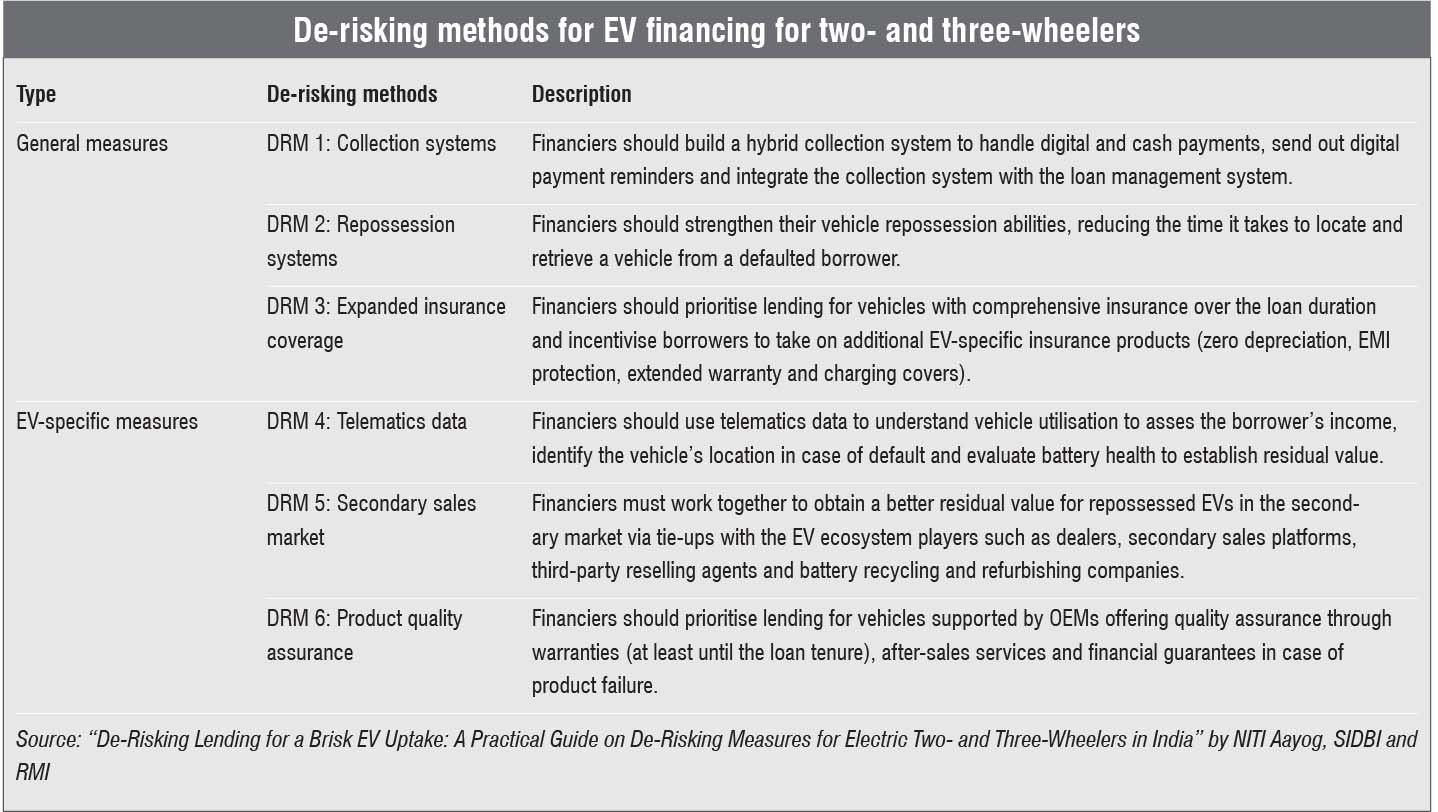

Despite this momentum, the key limiting factor is the lack of access to low-cost financing to mobilise capital at scale for EV adoption. To mitigate this challenge, de-risking strategies are needed in the EV financing space. Recently, in March 2024, NITI Aayog, the Small Industries Development Bank of India (SIDBI) and the Rocky Mountain Institute (RMI) launched a report titled “De-Risking Lending for a Brisk EV Uptake: A Practical Guide on De-Risking Measures for Electric Two- and Three-Wheelers in India”. The report emphasises the role of partial credit guarantees and on-lending products in addressing financing barriers in the EV market. Furthermore, it outlines six prioritised de-risking measures (DRMs) that can effectively mitigate risks and assist financiers by streamlining their operational costs, enhancing lending terms, strengthening their EV lending portfolios and providing more affordable lending options for borrowers. Renewable Watch provides an extract of the report…

EV financing market overview

The two- and three-wheeler EV segment is primarily financed by scheduled commercial banks (SCBs) and non-banking financial companies (NBFCs) that lend based on their risk appetite and desired profits. The lending cost depends on the financier’s cost of capital, operating costs and the risk premium, which includes the borrower’s credit risk, the quality of collateral and the business model’s operating and technical risks.

SCBs, which cater to less risky borrowers such as salaried individuals, have comparatively lower costs of capital in comparison to NBFCs, which serve new-to-credit (NTC) borrowers who are unable to secure loans from commercial banks, or those investing in new technologies, resulting in higher interest rates. As of now, NBFCs are the most common source of financing for electric two- and three-wheelers in India, with SCBs slowly becoming more comfortable with entering this market segment.

Financing challenges

Despite several factors supporting EV sales, in 2023, the overall sales penetration of electric two- and three-wheelers (goods and passenger vehicles) stood at 5.3 per cent. Specifically, after June 2023, sales witnessed a sharp decline due to the gradual reduction of subsidies under FAME II by the government.

Currently, most SCBs and NBFCs have assets under management valued at less than Rs 10 billion, leading to a high cost of financing for electric two- and three-wheelers compared to ICE vehicles. In particular, risk-averse lenders have a lower affinity for lending credit to NTC borrowers such as gig workers engaged in commercial last-mile deliveries and ride-hailing services, who constitute a key segment of borrowers in the EV ecosystem. These factors pose a significant challenge in scaling up EV adoption for the two- and three-wheelers market in the country.

Another key challenge is that the two-wheeler market has seen a remarkable increase in NPAs – from 7.7 per cent to 11.8 per cent – between financial years 2020-21 and 2022-23. This is partly due to the disruptions caused by the Covid-19 pandemic, which have prompted NBFCs to implement stricter lending norms.

Moreover, EVs face five key risks: counterparty, product, operation, repossession and residual. These risks are significantly higher in comparison to ICEs. Due to this, EV loans have higher interest rates, higher down payments, shorter cycles and higher EMIs for end consumers in comparison to ICEs, particularly affecting the lower credit borrower segment.

DRMs for EVs

EV financiers assess credit risk based on their portfolios to reduce expected losses based on three major factors: the likelihood of a borrower defaulting on a loan, the actual loss incurred by financiers after deducting the value they can derive from repossession and sale of the collateral on the defaulting loan, and the outstanding loan amount at the time of default. The report identifies six DRMs, which have been summarised in the table.

The way forward

The annual EV finance market is estimated to reach Rs 3,700 billion by 2030. To meet this potential, policy initiatives are needed in the EV financing space. For instance, SIDBI, in collaboration with various stakeholders, plans to introduce a financing facility for electric two- and three-wheeler loans in India. This includes a partial risk-sharing guarantee and an on-lending facility for SCBs and NBFCs. The facility, with its focus on DRMs, aims to provide lower-cost loans totalling

Rs 10.36 billion to financial institutions for EV loans and set up a partial credit guarantee (PCG) structure as a second-loss cover for SCBs and NBFCs. However, implementing this facility with DRMs requires cooperation among financiers, insurance companies, original equipment manufacturers (oems), technology start-ups and EV fleet operators to deliver cost-effective and sustainable value to the entire EV ecosystem.

The DRMs, if implemented properly in conjunction with the PCG and on-lending facilities considered under the financing facility, can kick-start a positive cycle of affordable lending for electric two and three-wheelers by mitigating financiers’ risks. It will ensure the availability of clear information for financiers to evaluate the risk profile of their borrowers, leading to lower borrowing costs through the on-lending facility, coverage of losses through the PCG facility and lower risk premiums.

Moreover, with the decrease in up-front costs due to economies of scale and financiers experiencing significant reductions in losses, lending at attractive rates will grow. This will stimulate EV demand across various segments, particularly for micro, small and medium enterprises (MSMEs), achieving scaled adoption in the entire EV ecosystem.

A persistent bottleneck for EV adoption has been the limited availability and high cost of financing for electric two- and three-wheelers compared to ICE vehicles. As a key solution, low-cost financing must be mobilised to fully unlock the EV market. To this end, by applying the same loan terms as ICE to EVs, the latter’s EMIs could witness a 5-14 per cent reduction. In addition, implementing schemes such as the Pradhan Mantri MUDRA Yojana, which offers financiers a government-backed credit guarantee on behalf of MSMEs, is needed to help cover defaults incurred on two- and three-wheeler loans. These efforts can help achieve the government’s National Electric Mobility Mission and EV30@30 vision, creating a ripple effect by reducing lenders’ perceived risks and driving EV adoption nationwide. Overall, the widespread adoption of EVs can help the country achieve its goal of netzero emissions by 2070.

By Srijan Naayak