The global adoption of floating solar systems has gained significant traction, particularly in regions such as Europe, Japan and China. Floating solar was first introduced between 2006 and 2007, experiencing a significant surge from 2012 to 2015, propelled by China’s Top Runner incentive programme. As of 2022, the global floating solar capacity exceeded 5 GW, with China emerging as the leader in the Asia-Pacific region. In 2023, Asia represented over 90 per cent of the world’s demand for floating solar systems.

India entered the floating solar space in 2015, signalling potential growth in this domain. Studies undertaken by TERI and the Center for Study of Science, Technology, Environment and Policy estimate India’s floating solar potential to range from 206 GW to 280 GW, with states like Madhya Pradesh, Maharashtra and Odisha taking the lead in exploration and implementation. The competitive market landscape, coupled with increased stakeholder participation and technological advancements, suggests a narrowing cost disparity between ground-mounted and floating solar plants. With tenders and auctions proliferating, the floating solar market is poised for continuous expansion.

Growth drivers for floating solar

India has set an ambitious target of achieving 500 GW of installed renewable energy capacity by 2030. Currently, renewable energy constitutes approximately 25 per cent of the country’s total installed electricity generation capacity. While ground-mounted solar installations dominate the solar power segment, challenges related to land availability and delays in land acquisition have slowed down the pace of utility-scale solar deployment. In response to these challenges, exploring alternative applications of solar energy, such as agrivoltaics, building integrated solar, canal-top solar, and floating solar, has become imperative.

Floating solar plants present a multitude of advantages when compared to ground-mounted and rooftop solar power installations. One key benefit is their land neutrality, effectively addressing the growing competition for land resources in solar deployment by mitigating associated licensing and land preparation costs. Moreover, these floating solar projects demonstrate a remarkable increase in energy yield, surpassing their land-based counterparts by over 10 per cent. This improvement is attributed to the cooling effect facilitated by the water surface, resulting in a notable drop of approximately 5-10 degrees in module temperatures.

Another advantage lies in the synergy with existing power plants, as many floating solar projects are strategically co-located with hydro/thermal power facilities. This allows for seamless integration with the pre-existing electrical infrastructure, minimising the requirement for additional infrastructure for power evacuation. Furthermore, the installation process is simplified, requiring no further land preparation activities once the waterbed is confirmed for site feasibility. This streamlined approach leads to shorter installation and deployment times for floating solar plants. From an environmental perspective, studies indicate a significant reduction, up to 40 per cent, in the rate of evaporation from floating solar sites.

In addition, these solar panels play a role in diminishing algal activity, contributing to lowered water purification costs. Many floating solar plants are established in flooded coal mines, thereby contributing to the rehabilitation of degraded lands. Collectively, these advantages position floating solar as a compelling alternative in the domain of solar power solutions.

Increasing traction in India

Renewable Watch Research recently conducted a study on the floating solar market in India, tracking over 100 projects. The study highlights growth trends, potential, key projects, technology trends and the project pipeline for the floating solar segment in India. According to the study, Kerala and Telangana collectively account for about 70 per cent of the total commissioned floating solar capacity in India. With over 56 projects aggregating 4 GW in the pipeline, major emerging players in the floating solar segment include NHPC Limited, SGEL, NTPC Limited and SJVN Limited, with NTPC leading the market.

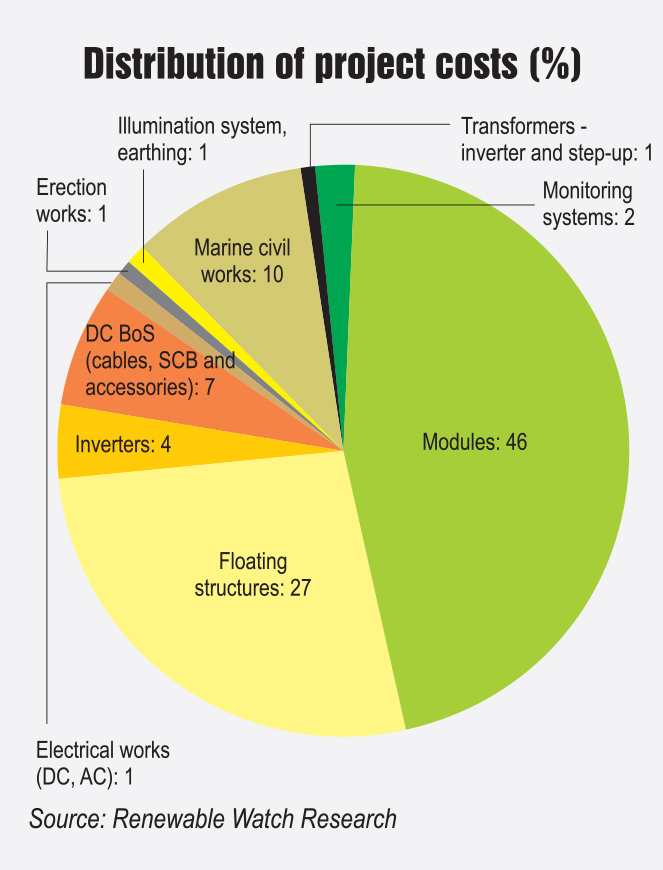

Typical cost components

Modules and floating structures collectively constitute 75 per cent of the total hard costs for a floating solar project. Other major components include marine civil works (if required), balance of system costs, inverters and electrical works. Assuming 9-10 per cent additional soft costs, the total cost for a floating solar project in India is 1.4-1.6 times that of ground-mounted solar projects.

Key challenges

While floating solar projects have promising potential, there are several challenges that demand attention. First, the capital expenditure associated with establishing floating solar plants is notably higher compared to conventional ground-mounted solar plants. However, this initial investment is justified by the enhanced energy yield these systems offer throughout their operational lifespan. Another critical concern is the environmental impact. The long-term effects of floating solar systems on waterbodies and marine life remain inadequately understood. The reduction of algal growth, which may result from the implementation of floating solar, presents a potential drawback, as it may not be universally desirable for all waterbodies.

Operations and maintenance (O&M) for floating solar prove to be challenging due to the unique nature of these systems being situated on water, necessitating specially trained manpower and equipment. Regulatory hurdles add another layer of complexity as permissions need to be obtained from multiple owners of waterbodies across different states. The absence of standardised agreements for water rights further contributes to prolonged deployment times and potential cost escalations. Moreover, there are challenges in the supply chain and manufacturing aspects. For instance, procuring floating structures internationally may incur higher costs and transportation difficulties. Although some domestic and international players have entered the market, the number of specialised manufacturers, particularly in comparison to ground-mounted solar, remains limited. As the industry matures, addressing these challenges becomes imperative for the widespread and efficient adoption of floating solar technology.

The way forward

Given the increasing competition for land resources, the floating solar segment is expected to maintain a steady market share, with a compound annual growth rate of 15-20 per cent for the next five years. Although India has been an early adopter of floating solar technology, the potential remains largely untapped, with penetration being less than 10 per cent of the total potential. The further proliferation of floating solar projects is inevitable and dependent on the timely resolution of several key issues.

Key considerations for the future include:

- Research and development: In-depth research is necessary to design floating solar power plants that can withstand changing wind and water profiles in the country’s climatic context

- Site identification studies: Pre-feasibility assessments covering hydrological data and environmental impact studies should be conducted for floating solar sites to create a project shelf and reduce implementation time.

- Regulatory frameworks and technical standards: Clear policies and regulatory frameworks for the development of floating solar plants are required. The development of specific standards and institutional mechanisms for testing and benchmark certification is crucial to signal the government’s stance on the segment

- Support to technology suppliers: Technology providers, especially start-ups, require support in terms of finance and policy to offer cost-competitive technologies

- Bidding considerations: Future tenders for floating solar projects should prioritise technology and technical considerations over cost to avoid aggressive bidding. Setting a floor tariff initially for such projects may provide comfort to developers.

In conclusion, floating solar is now a well-established technology with demonstrated benefits across the globe. With the increasing number of tenders and tariff-based auctions, the market for floating solar is becoming competitive. The entry of both established and new players, along with technology suppliers exclusive to this domain, instilsconfidence in both developers and financiers. Consequently, the current cost disparity between ground-mounted and floating solar plants is expected to reduce with the proliferation of installations in the segment.