")

Over the past decade, renewable energy development has gained rapid momentum across the world. Drivers for this growth include increasing the climate commitments of governments and businesses, increasing awareness and political will, technological advancements, access to finance, and the increasing overall profitability of renewable energy projects. The Indian renewable energy sector has also witnessed tremendous capacity additions over the last few years. Moreover, India has seen the highest growth in renewable energy capacity addition among all global economies over the last seven to eight years, with its overall capacity (including large hydro) increasing 1.97 times, and solar energy in particular increasing nearly 18 times.

As in any infrastructure sector, access to capital has played a significant role in determining the growth of the renewable sector in India. The sector has been attracting increasing investments in the form of both debt and equity. A significant share of these investments come in the form of debt through various channels. Private non-banking financial companies (NBFCs) were the first entrants in the renewables debt market, as conventional financiers such as banks were reluctant to enter the new, evolving market. The large debt size and the long duration of renewable energy projects also acted as deterrents, initially, in gaining access to financial support from both public and private banks. However, as the sector progressed, the financing dynamics transformed significantly. A diverse set of funding sources are now increasingly playing an active role in the sector. These include banks, bond markets (domestic and global), international lenders and development finance institutions, that are contending to become active participants in the growing renewable energy sector due to its widespread socio-economic impact. Private NBFCs have now been overshadowed by large banks, while domestic and international bond markets are also proactively contributing to the sector’s funding landscape.

India has set ambitious targets for the deployment of renewable energy over the next decade. In contrast to the initial dearth of investments in the sector, it is now receiving government and global support. It is further supported by the ease of installation of projects, land availability, new refinancing opportunities and replicability. Access to debt capital for a capital-intensive sector like renewables can potentially be the biggest growth factor at this time.

Domestic and international debt market

Domestic debt financing for renewable energy projects was primarily led by private NBFCs over the first five years of the development of the sector. Private NBFCs were quick to identify the strengths of solar and wind projects, which had lower developmental risks and shorter construction periods. Public sector NBFCs were the second biggest contributors. Financial entities such as the Power Finance Corporation and Rural Electrification Corporation later entered the lending market, providing the required impetus to the growing sector. Soon after, private banks such as IndusInd Bank and Yes Bank also entered the market, with Yes Bank becoming a strategic and financial adviser to Greenko Energies in the acquisition of SunEdison’s solar portfolio in India. The bank also issued India’s first green infrastructure bonds in 2015. Domestic bonds entered the market soon after the demonetisation undertaken by the Government of India in 2016. Other instruments of debt, such as mutual funds, have also become a part of the funding landscape in the sector.

However, the flow of debt was hit by the IL&FS and DHFL crisis, when these two NBFCs delayed and defaulted on their debt repayments to their lenders. This setback was further exacerbated by the unprecedented Covid-19 crisis. Yet, in the last two years, larger banks have rapidly increased lending to renewable energy projects, providing a fresh impetus to the sector. HDFC more than doubled its financing book in financial year 2020-21. As of September 2021, the State Bank of India is leading in terms of the cumulative amount deployed in renewables at roughly Rs 330 billion. It has also altered its credit matrix to allow for more competitive funding of more renewable projects. Large banks have overtaken NBFCs due to their price competitiveness, proving the importance of sustained banking interest in providing competitive debt financing to Indian renewable developers.

The international debt environment has largely adopted a cautious approach to investing in renewable projects. Lending patterns have evolved on the basis of the identified risks, existing political motivation and overall sectoral growth over the past decade. With the emergence of greater political emphasis on the sector and an industrial push, large banks such as Standard Chartered Bank (SCB) and Rabo Bank are now big contributors to the sector. In 2021, for instance, SCB was one of the largest renewable lenders, with nearly a $1 billion in underwriting pinned for the Adani Group. Other lenders are also likely to expand their portfolio towards renewables, given that financiers such as Societe Generale are also increasing their debt contributions to the sector.

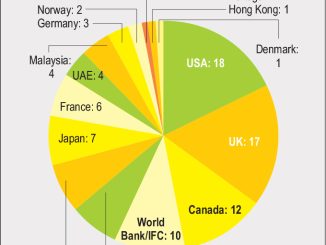

The international bond market, on the other hand, has performed differently. The bond market adopted a proactive approach from earlier on, presenting high-yield offerings to bond buyers. The market not only provides attractive deals for borrowers but also security to lenders using investments and investment ratings. Key international and domestic players have been participating in the international bond market since as early as 2014, with multiple large international bond issuances and refinances. These players include Adani, Hero Futures, Morgan Stanley-backed Continuum, Greenko, ReNew Power, and the International Finance Corporation- and Caisse de dépôt et placement du Québec-backed Azure. The latest players to join the international bond market are development financial institutions such as Asian Development Bank, the Asian Infrastructure Investment Bank and their consortiums. These institutions provide long-term money with negligible interest rate fluctuation risks. While, at present, these instruments are only utilised for commissioned projects, development financial institutions can shift the focus towards refinancing of operational projects using bonds. The international bond market can play a significant role in renewable financing, with greater innovation in financing tools and lending structures.

Challenges and opportunities for the future

Despite tremendous growth in the sector, there exist several challenges that need to be addressed to further streamline financing of renewable energy projects. Due to the risk-averse nature of investors, de-risked operational projects continue to receive the majority of new investments. As a result, greenfield projects are lagging behind in receiving the desired investments from large lenders. Furthermore, a hefty proportion of time-bound renewable energy projects under development receive debt from relatively costlier lenders. This is especially true for non-central government projects, such as state projects and private party offtake projects. Project sizes have also increased tremendously and are likely to continue on this growth trajectory in the coming years, with a rise in hybrid, storage and round-the-clock projects. With the rise in project sizes, debt requirements are also expected to rise. While large projects should ideally receive funding from large, established banks, they are reluctant to invest in these newer technologies and structures.

However, given India’s ambitious targets of achieving net zero emissions by 2070 and establishing 500 GW of non-fossil fuel sources of energy, rapid advancements in technology and falling prices are continuously improving the competitiveness of the renewable energy industry relative to its counterparts. This has been seen in India’s rooftop solar market, which has established itself as highly cost effective. Financial institutions and lenders can, thus, come together to form a consortium to provide effective opportunities for lending. In line with the National Bank for Financing Infrastructure and Development, which was announced in the Budget 2021, a dedicated bank for infrastructure project financing oriented towards renewable energy can also be created. Such a bank may play a central role in aiding and leading policy advocacy, deal structuring, setting the groundwork for sustained growth, providing guarantees, removing financial bottlenecks, etc. Collaborations can generate greater opportunities for innovation, thereby boosting the overall competitiveness of the sector.

An essential element of future debt financing for renewable energy would also be carrying out in-depth research on the evolving renewable energy market to better understand the risk-return dynamics of various debt structures. Multiple models of renewable energy are now operational or under development, including hybrid, storage, green hydrogen and battery energy storage system technologies. It is crucial to analyse the expected risks and returns of these different project combinations to ascertain the most cost-effective financing through debt.

The adoption of global environmental, social and governance (ESG) frameworks and principles has also initiated a new, rising investment boom in the renewable energy sector. ESG commitments are anticipated to bring in greater investments in the sector over the coming years. According to Bloomberg, ESG assets may hit $53 trillion by 2025, a third of global assets under management.

To conclude, rising momentum, constant innovations, and greater global and domestic investor interest together provide a great opportunity for the Indian renewable energy sector to grow over the next decade. India’s renewable energy potential has been evaluated to be over 1 terawatt, led by solar, wind, bioenergy and small hydro.

Additional improvements in terms of battery storage green hydrogen solutions, hybrid models and peak power at utility scale may create the opportunity to meet almost all of India’s energy demand using renewable sources. Therefore, a strategic emphasis on renewable financing and debt model structuring would go a long way in ensuring that India is able to meet its renewable energy potential effectively and efficiently.

This article is an extract from a report titled “Renewable Energy Financing Landscape in India: The Journey So Far and the Need of the Hour”, published by the Institute for Energy Economics and Financial Analysis (IEEFA) in February 2022.