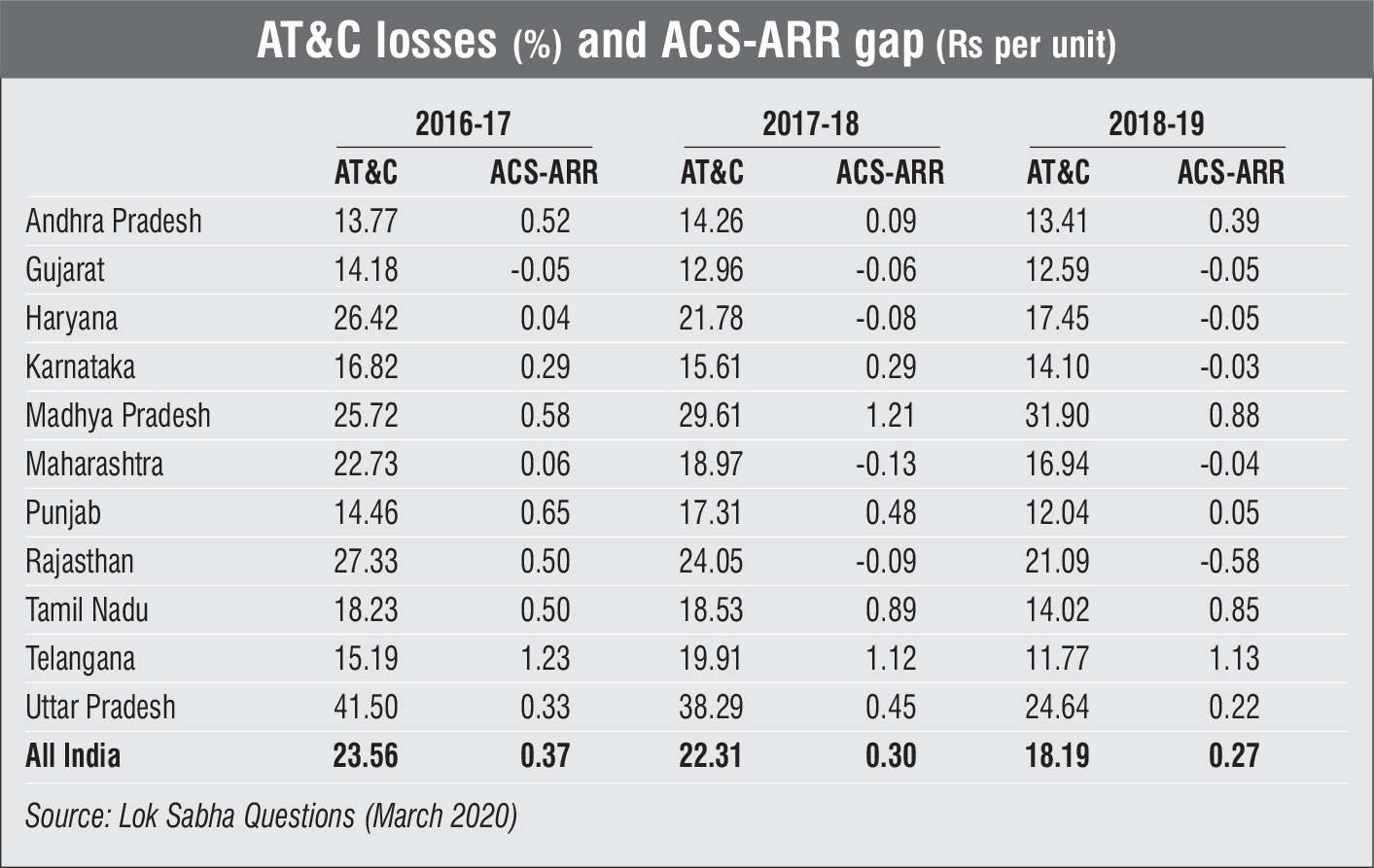

Power distribution has remained the weakest link in India’s power sector for a very long time. While the generation and transmission segments have evolved and become competitive and efficient over the years, distribution still struggles due to heavy technical and commercial losses, which affect the entire power sector value chain. The UjwalDiscom Assurance Yojana (UDAY) was launched by the central government in 2016 as a revival scheme to help loss-making discoms turn around financially. Unfortunately, UDAY has failed to tackle the underlying issues in the sector and most states have been unsuccessful in meeting their targets due to billing issues, shortfall in the collection of revenues, non-reflective tariffs, non-payment of subsidies by states, and non-payment of power dues by state government departments. While leakages in transmission and the non-recovery of billed amounts have decreased over the years, many discoms are still unable to deliver electricity efficiently and have high aggregate technical and commercial (AT&C) losses, much more than the targeted 15 per cent. Moreover, the gap between average revenue realised and average cost of supply (ARR-ACS) remains high, indicating large operating losses.

Impact on renewable energy generators

These continued discom losses have serious implications for the entire power supply chain as payments from discoms to generation companies, including renewable power producers, are getting increasingly delayed. This delay in payments is not a one-time default but has become a recurring problem, with some renewable power producers not having been paid for as long as six months to one year. As of May 2020, discoms’ outstanding dues to conventional and renewable power generators reached Rs 1,163 billion, creating a massive liquidity crunch in the power sector. The list of unpaid developers includes the majority of India’s top solar and wind power producers. Notably, it is the renewable energy-rich states such as Andhra Pradesh, Karnataka, Rajasthan, Tamil Nadu and Telangana that are the worst in terms of payments.

With open access and trading forming a small part of the total renewable energy procurements, signing long-term contracts with discoms is the only option for most developers. Most of these power producers are already struggling owing to transmission and land constraints, low margins due to declining tariffs, and generation curtailment. Thus, any payment delays severely affect their liquidity. Further, these developers have to repay lenders and the non-payment of dues can impact project viability. Hence, the issue of non-payment has become a major pain point for developers as well as investors, often resulting in a lukewarm response to bids. Although the government has taken steps to address this issue through various payment security mechanisms, such initiatives have not generated the desired outcome and the Covid-19 pandemic has further aggravated the situation, with discoms backing out of payments.

Addressing discom inefficiencies

Various government reforms have been enforced time and again to improve the situation of the country’s ailing power discoms. However, their success has been limited and they have been unable to have a lasting impact on the discoms’ financial health. Meanwhile, a bailout package of Rs 900 billion has been announced by the government through which discoms would receive subsidised debt funding from the Power Finance Corporation and the Rural Electrification Corporation. This would allow discoms to cover some of their current overdue payments and effectively infuse liquidity into the sector. Further, the Ministry of Power has proposed amendments to the Electricity Act that pitch for franchising of discoms, cost-reflective electricity tariffs without subsidy, strengthening of the payment security mechanism and the Electricity Contract Enforcement Authority to bring confidence in the sector. However, according to the Institute for Energy Economics and Financial Analysis’ (IEEFA) report “The Curious Case of India’s Discoms: How Renewable Energy Could Reduce Their Financial Distress”, power distribution is the state’s domain and each state discom is on a different path of reform. Thus, state-level solutions are important to address discom issues rather than central-level policies, which can only serve as guiding principles. The IEEFA’s report presents a detailed analysis of discoms in three states, Maharashtra, Rajasthan and Madhya Pradesh, which are at different levels of operational and financial performance. These discoms have varying appetites for reforms, levels of penetration of renewable energy, scope for technology upgrades and so on. These discoms are suffering high AT&C losses and reeling under debts despite them having adopted various reform measures to improve their operational and financial performance.

This report highlights the various opportunities for reforms in these discoms based on their changing performance over the years. Further, the report provides a list of recommendations for the discoms in these states as well as in other regions that can help in reducing the financial and operational inefficiencies across the Indian distribution space. The report recommends the resolution of issues surrounding legacy contracts, the closure of inefficient plants, a reduction in cross-subsidies and a decrease in AT&C losses through digitalisation. A revision of tariffs to make them cost reflective, an increase in competition to promote efficiencies, the creation of a national pool market and the implementation of renewable energy tariffs with indexation are the other important measures suggested in the report.

Discomprivatisation

Discomprivatisation

The increasing competition in the power retail business is considered an important step towards addressing the issue of inefficiency in the distribution space. The Ministry of Power’s Vision 2024 document reiterates this as an important goal. It suggests that by unbundling the discoms into the wires and the supply businesses, and by increasing the participation of private players in various facets of discom operation, their situation can be improved. It was the Electricity Act, 2003 that led to the beginning of private sector participation in the power distribution space through various business models such as private distribution licensee model, private distribution franchisee model and management contract model. In fact, there have been a few successful cases of discomprivatisation in India, including those of discoms in Mumbai, New Delhi, Kolkata, Noida, Ahmedabad, Surat, Gandhinagar and Dahej. However, apart from these isolated cases, the distribution space remains dominated by state-owned discoms. Meanwhile, significant growth has taken place in competitive procurement and privatisation in generation and transmission.

In recent years, discomprivatisation has garnered much attention, and observing this, the government recently announced plans to privatisediscoms in union territories. Further, the Draft Electricity Amendment Act, 2020 has highlighted the importance of competition in the power retail space by introducing the concept of sub-licensing, which is a mix of distribution franchisee and parallel licensee. By combining the two models, sublicensing aims to avoid the duplication of network and metering infrastructure for the same set of consumers, which is a possibility in parallel licensing. At the same time, it promotes private sector participation by franchising. According to ICF’s recent white paper titled “The Need for Private Sector Participation in India’s Electricity Distribution Sector”, the structure of the Indian power market gives significant control to states. States can decide the level of competition, the degree of private sector participation and the model to be adopted based on their desires and needs. Thus, separation of content and carriage assumes great importance for bringing competition in power distribution. The content part would deal with purchasing power from generators, selling power to consumers and billing, and the carriage part would include network operations, planning and development. In this model, independent entities could operate the carriage business business, which enable transparent third-party access to the content business by power consumers. Further, multiple retail supply companies could compete with each other for supplying power to consumers within a single region and improve efficiency of the power distribution segment.

The way forward

India has set a target to achieve 175 GW of renewable power capacity by 2022 and a long-term ambitious goal of 450 GW by 2030. However, the country’s power demand is not increasing at the required pace and has, in fact, declined in 2020 due to the economic slowdown resulting from Covid-19. In order to realise these ambitious renewable energy targets, the distribution segment needs to be equipped both operationally as well as financially. With restrictions on open access and trading of renewable power still limited, long-term power procurement from discoms is the only available option for developers. Thus, discoms need to be prepared and made more efficient for procuring such high quantities of renewables without making developers suffer by not paying their dues on time. Going forward, the emphasis should be not only on the adoption of advanced technologies and robust infrastructure but also on addressing the inherent issues plaguing the distribution segment. Tariff

hikes need to be separated from political agendas and made cost reflective while cross-subsidisation needs to be gradually phased out. Finally, the interference of states in power supply should be decreased by increasing private sector participation so as to provide fair competition in the power retail business and put an end to the monopoly of state discoms.

By Khushboo Goyal